Basis Commodities – Australian Crop Update – Week 42 2022

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

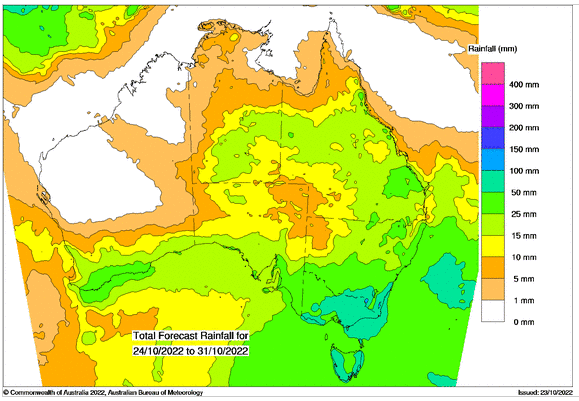

Australian grain markets moved sharply higher in all zones last week on the back of the torrential east coast rains. Central Queensland, which had started harvest, received 150-200mm for the week. Southern Queensland and Northern New South Wales also recorded heavy rain. Totals were lighter further south although the rain was patchy. While there was some isolated heavy rain across parts of Victoria, totals across the Wimmera and Mallee were mostly limited to 5-10mm. It was a similar situation in South Australia. Western Australia was mostly dry and continues to enjoy good harvesting weather.

Accessing grain from storages is an emerging problem. A secondary problem is getting the grain to its destination. This is particularly evident in central Victoria with many roads closed due to floods. In our view, this is likely to become a major feature of this harvest and the subsequent export program and will need to be treated carefully by exporters and consumers alike.

Grain quality is an additional problem. Our analysts AgScienta have released an updated protein profile of the wheat crop slipping with the wet finish. It will be a big ASW year at best and at worst, we’ll see large volumes of downgraded wheat if the rain continues through the harvest window (November-January). Memories of 2010/11 will be still fresh on the traders who survived it.

It’s going to be a long, drawn-out harvest which further exposes the crop to quality downgrading as farmers struggle to get grain off with their own equipment, relying on neighbours for assistance once they’ve finished cutting their own crops.

The rain is a big problem for canola where farmers would typically be windrowing crops ahead of harvest. Windrowing is impossible with the current wet weather leaving paddocks too wet to hold machinery. Initially, we thought this may result in yield losses as they wait for crops to ripen and then direct-head harvest. This approach is difficult and draws out the ripening process leading to yield losses as they wait to optimise the already ripe pods against pods that aren’t ready. However, crop coatings can be applied to ripening canola which holds the pods together limiting yield losses associated with direct heading. Access to planes to apply this will be the next issues.

It should be noted that harvest is already running two to three weeks later than normal due to the cold and wet weather on the east coast. This means most crops are still green and benefiting from rain. Ripening of feed wheat crops will be dependent on the weather between now and harvest. We’re not quite into that window yet, but it’s looking ominous with more rain on the way next week. Similar patterns of southerly fronts combined with a trough that draws moisture from the north is expected to result in more extreme rainfall across the east coast in the latter half of next week.

The weather situation is better in South Australia and Western Australia where receivals have started to roll in.

On the cash side, traders were releasing stocks allocated against export positions that work into domestic markets with the spike in prices. Aussie feed barley is triggering export demand at current values. Canola strengthened with the spike in ICE which is likely to be driven by export selling to China.

WA and SA bids were also sharply higher in the past week. Exporters have become more sensitive to supplies for nearby shipments as the east coast outlook becomes more uncertain.

From our perspective, another massive crop year puts the customer’s focus squarely on grain quality and logistics. Grain stocks will continue to swell across wheat, barley, and canola. We will have stock build across all balance sheets, the question is where the demand comes from for a big ASW crop. We understand China has already been active in securing ASW which is likely to be used as a low-quality milling wheat/feed wheat. Southeast Asian feed wheat buyers have also been active to ensure access to harvest slot logistics. Consequently, we believe Southeast Asian wheat importers are reasonably well covered for the first quarter but demand from the Middle East and East Africa is slow due to the pricing dilemma provided by Russian wheat, at least 60 dollars below APW on a FOB Basis. Difficult economic conditions and a high US dollar simply exacerbate the situation.

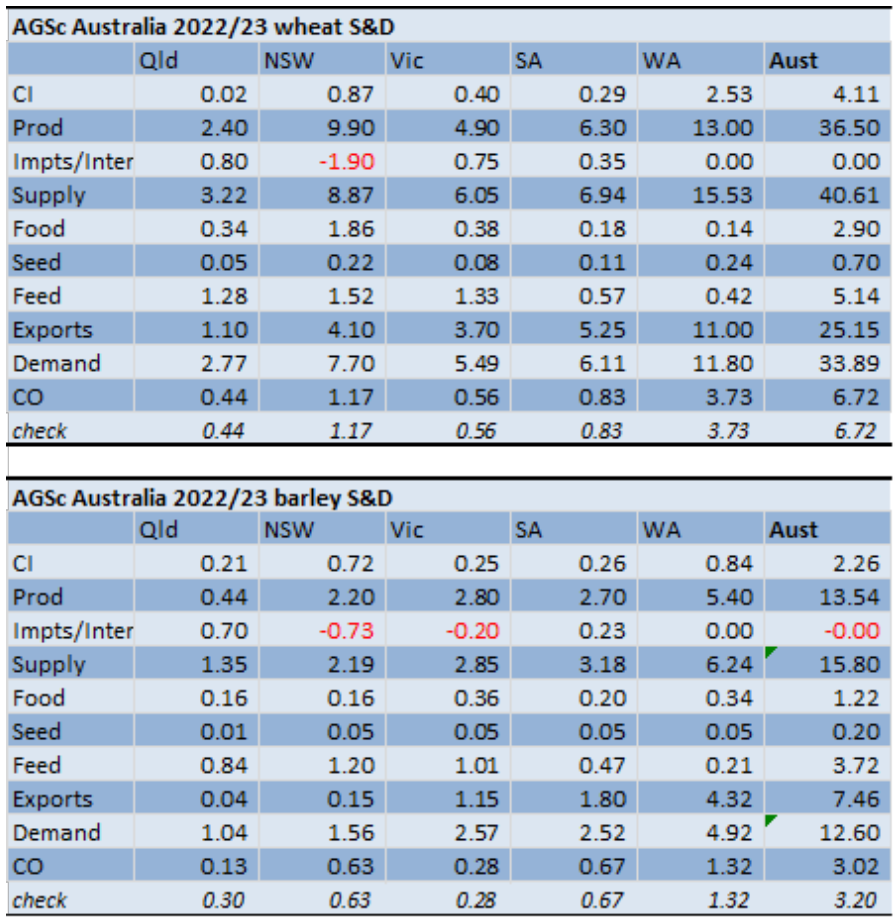

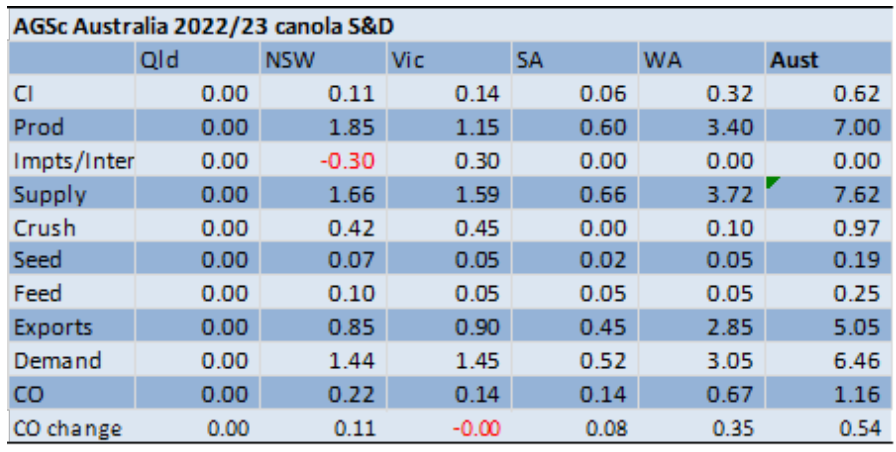

Updated Balance Sheets and Projected Crop Profile

We have lifted national wheat production to 36.5MMT, barley to 13.5MMT and canola to 7.0MMT. There are some production losses in NSW and Victoria where crops are saturated, have been sitting in water for some time and will be abandoned. But overall, more crops are benefiting from the rain still. We are calling the NSW yields down 20-30% on last year. Victorian grain production will be hurt in parts, although the worst hit areas by the floods are not the state’s biggest production areas. Overall, the impacts will be relatively small, and these are offset by big yields in the Mallee and Wimmera. South Australia will be a record large crop and Western Australia is similar to last year and possibly better.

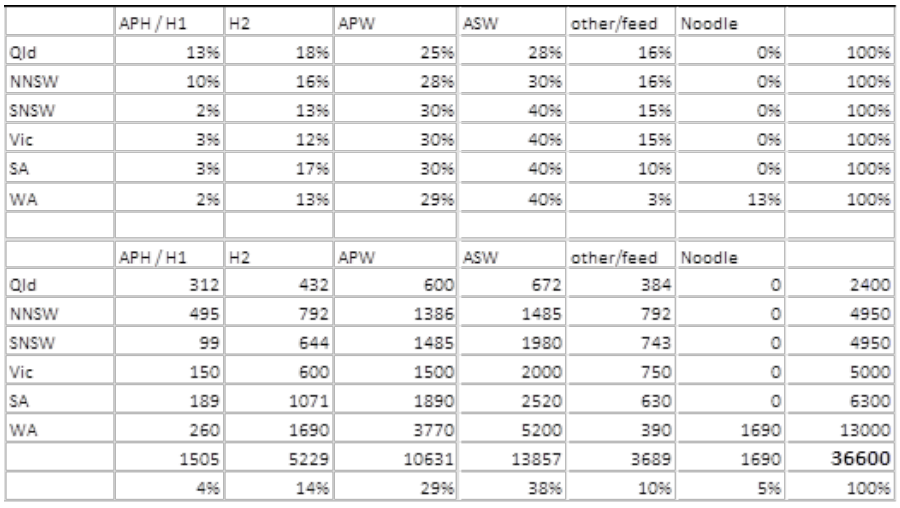

Below is our current projection of crop quality. As some of our customers would already know, access to high protein wheat for exports is going to be a challenge with domestic users moving quickly to secure the protein they need from a depleted crop.

Export Stem

There was 776KMT of grain added to the stem over the past week with canola the largest contributor. There was 342KMT of canola, 324KMT of wheat and 110KMT of Barley added to the stem with nearly half of this coming from Western Australia. It comes as no surprise the weekly east coast stem additions were limited as the ongoing unsettled weather stalls early harvest and doubts when the new crop supplies will be available for export.

Ocean Freight

The Ocean Freight market continues to search for direction. Levels in the Atlantic are firming. The issue is what is going on in the Pacific where there is little to provide direction. Indices would seem to support a weaker market and the sentiment is negative, and yet the market remains stable. Week to week rates are down with less enquiry causing numbers to ebb away. After last week’s push on bunkers, they have started tracking down again.

Oaten Hay

The Australian hay season is expected to produce around 12 million tonnes for the 2022/23 season. The rain in the eastern states is likely to limit the amount of export quality hay from that region. South and Western Australian states however have had favourable conditions and expect to represent the exportable surplus of approx 1.1MMT for the season.

The biggest challenge to exports of fodder products remains ocean freight. Container rates into the Middle East remain firm and while there has been some nearby indices support for softer prices into 2023, the limited export surplus caused by the wet weather in the eastern states is supporting prices.

Australian Dollar

The AUD is one of the most liquid currencies in the world and given the prevalent risk aversion in the air, the AUD is proving yet again to be the weapon of choice to express risk aversion and is consequently in a bearish trend. Inflation is expected to peak at the end of the year in Australia. The RBA is now trying to balance the impact of interest rates over GDP rather than just catching inflation. The market is expecting a further 25bps increase in November in Australia and opposing to other developed countries, a growth in their GDP. That makes the Aussie attractive versus other currencies.

The post Basis Commodities – Australian Crop Update – Week 42 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.