Australian Crop Update – Week 12, 2025

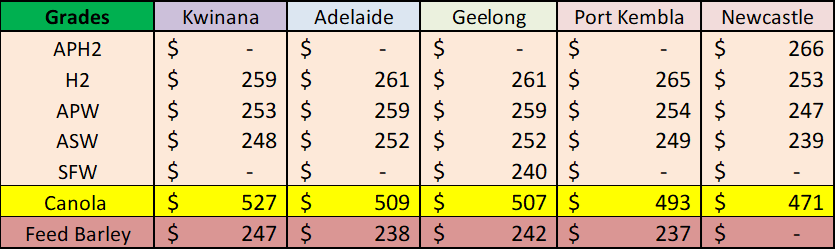

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Trump’s tariff agenda has added another layer of complexity to international grain markets in recent weeks. However, the local prices drivers remain little changed as this overseas volatility provides noise as to where we go from here.

There are two opposing features that are currently driving domestic grain markets. Grain markets in southeastern Australian are being driven by the dry weather and limited pasture supplies which are keeping the delivered feed grain markets firm. This is starting to spill into the track feed grain values. These dry weather worries are creeping north where it was reported that farmers were now holding lupins as stockfeed as they are concerned for the seasons weather prospects. The weather worries will continue to build the longer the east coast goes without significant rain as we approach the planting season.

On the other hand, sluggish wheat export sales are dampening the appetite of traders to chase wheat supplies. It’s an interesting discussion how these two factors get resolved in the market. In the south, its likely to be the timing on rains that trigger pasture growth ahead of the cooler months. Sluggish demand from key Asian wheat importers is unlikely to change without a major production scare in Russia given the balance sheet and certainly that they have little incentive to move away from just-in-time purchasing patterns which is akin to a Dutch auction between the major origins. Ultimately Asian buyers are happy for the Australian farmer to carry wheat for the time being and the farmer is not in a hurry to sell.

What is interesting is the small protein spread that we are seeing in Australia. Higher protein wheat grades slipped $2-3 per metric tonne (/MT) while ASW bids edged higher on the strength of the domestic feed markets.

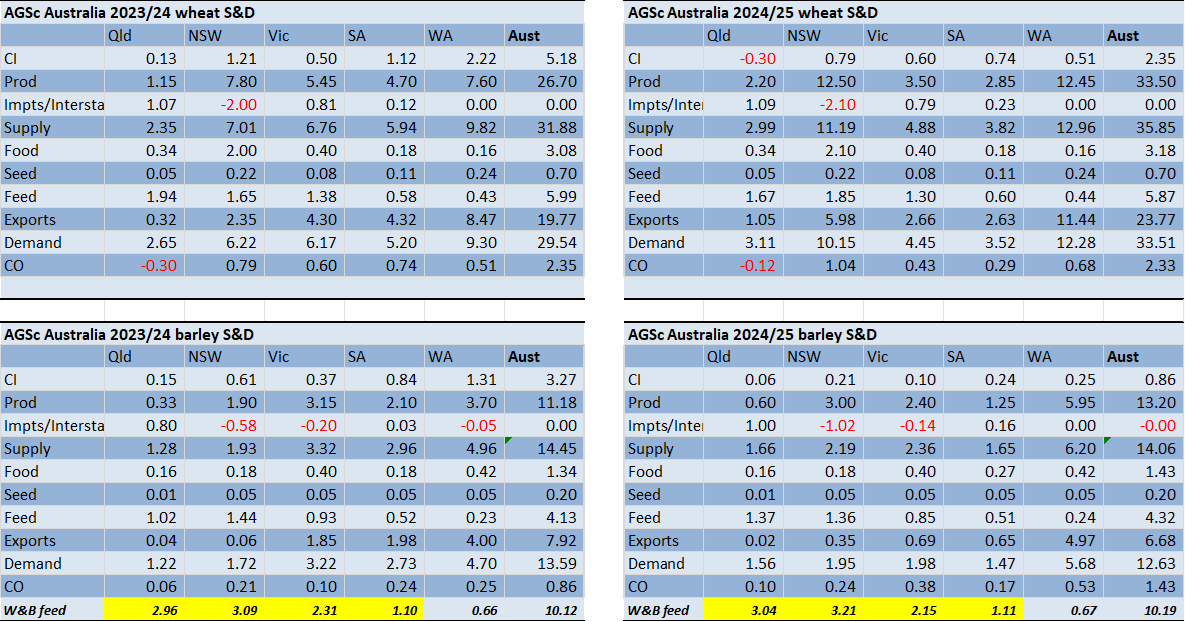

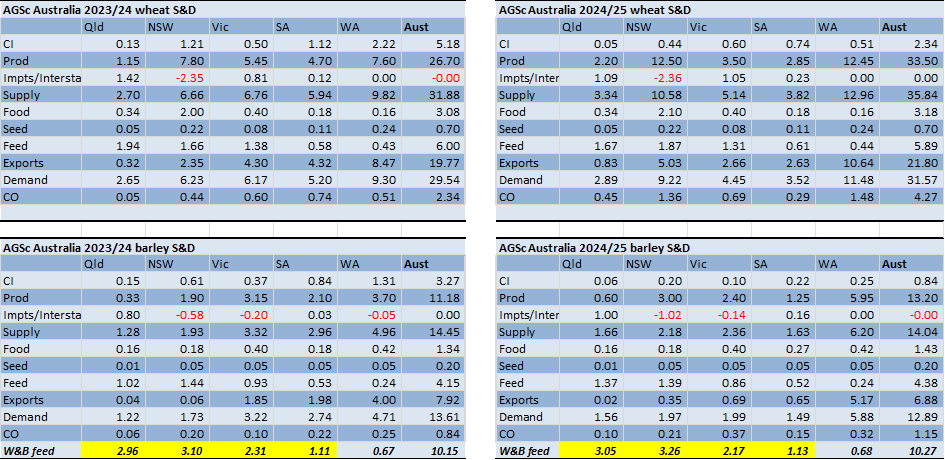

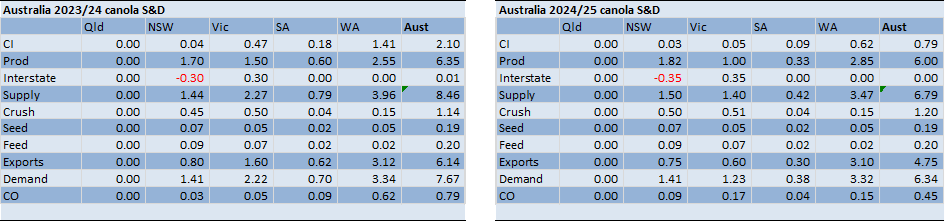

Australian Supply and Demand update:

Our Analysts have raised our forecast of Australia’s 2024/25 barley crop to account for the strong export pace. Heavy supplies of barley in QLD and Northern NSW also justify higher yield assumptions for the northern production areas of the east coast. National barley production has been raised to 13.2 million metric tonne (MMT). National wheat and canola production are little changed but the exports have been updated for the ABS actuals for October/November/December and stem forecast projections for the January/February/March quarter. We have kept national wheat exports close to 24MMT but the sluggish start to the program means more of the export task will be pushed into the July/August/September quarter when Australia competes with 2025/26 Black Sea supplies. The latest updates lift Australian wheat production to 33.5MMT, barley production to 13.2MMT, canola 6.0MMT and sorghum at 2.475MMT.

Source: AgScientia www.agscientia.com.au/

Export Stem & Ocean Freight Market Update:

IThe Panamax market sprung to life off the back of stronger Transatlantic and ECSA demand last week. The Pacific was stable compared to the gains in the Atlantic but as owners with ships in Asia are now looking to ballast towards the east coast of South America, it has a had a flow on effect with offer rates being revised upwards. With Nopac and Australia still active, some Charterers were caught out by this sudden shift. The Supramax/Ultramax market continued its strong run in the Pacific but remains a mix affair in the Atlantic. The Handysize sector remains the quiet achiever over the past few weeks in both Basins. The Pacific is still well supported with long backhaul steels paying a premium which is causing tonnage lists to tighten. As a result, the outbound values from Australia/NZ have grown, not necessarily by an increase in demand but by a lack of suitable tonnage available for charterers to fix.

There was 873 thousand metric tonne (KMT) of wheat put onto the stem in the past week making it the second biggest week of nominations for the year. This included New South Wales (NSW) with 297KMT followed by Western Australia (WA) with 285KMT, Victoria (VIC) 175KMT and South Australia (SA) with 116KMT. Other grains were reasonably lean with 124KMT of barley and 107KMT of canola.

Despite this good export stem performance, we adjusted our export forecasts through the week. The stem and export reports show that wheat shipments are lagging the pace needed to achieve the previously forecast 23.8 million metric tonne (MMT) export forecast. Specifically, NSW, Queensland (QLD) and WA. We have reduced NSW wheat exports by 1MMT to 5.0MMT. Interstate flows have also been adjusted. WA wheat exports have been cut to 10.6MMT which lifts the ending stocks to 1.5MMT. Australian wheat exports are now forecast at 21.8MMT, but this could still prove optimistic if the exports in NSW, QLD and WA don’t improve in Q3 and Q4 of our October to September marketing year. National wheat ending stocks are forecast at 4.3MMT which is 2MMT more than last year. Australian barley exports have been edged higher to 6.9MMT. WA exports are now 5.2MMT. Ending stocks will be tight in all states.

Australian Weather:

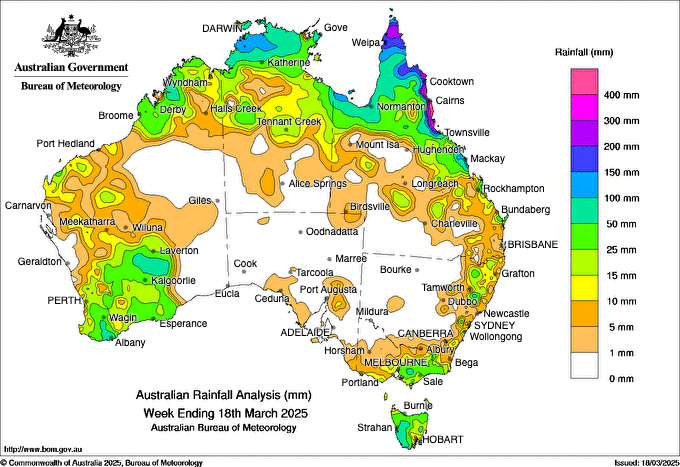

Weather concerns are increasing following a dry summer in southeastern Australia and a hot summer in the north. The most pressing concern is the dry weather across SA and VIC. Most of SA’s cropping area soil moisture is in the bottom 1%. These dry weather concerns have now also extended into Southern NSW. Northern farmers are also looking for rain and were disappointed that the storms following Alfred didn’t offer any significant rain for the cropping areas apart from Central QLD and some patchy storms in Southern QLD.

On the other hand, the Australian Bureau of Meteorology extended outlook from April to July is holding to the normal rainfall patterns for eastern and central Australia. Although their recent track record hasn’t been that good in terms of forecast. WA picked up good rain last week which has only added to reasonably healthy moisture profiles in the west. The rainfall totals were better than initially forecast with the cropping regions receiving 20-45mm across the week providing a good start to the 2025/26 Season.

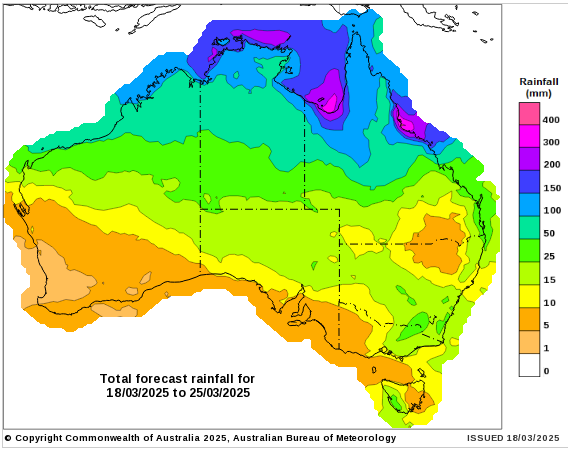

8 day forecast to 25 March 2025

http://www.bom.gov.au/

Weekly rainfall to 18 March 2025

http://www.bom.gov.au/

The Bureau of Meteorology released its long-range forecast for March to June last week. Rainfall is likely to be in the typical range for the season for most of Australia, with below average rainfall likely for much of northern, eastern and central QLD and above average for parts of north-western Australia. Warmer than average days are very likely across most of Australia, with an increased chance of unusually high daytime temperatures across much of the country.

AUD/USD Currency Update:

The Australian dollar was higher to end last week when valued against the Greenback closing at 0.6302. The Australian dollar (AUD) received support from rising commodity prices, including gold, steel, and iron ore on Friday. However, The AUD/USD pair could face pressure from a strengthening US dollar (USD) amid growing fears of a global economic slowdown. We continue to think more bouts of AUD volatility should be anticipated over coming weeks.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.