Australian Crop Update – Week 16, 2025

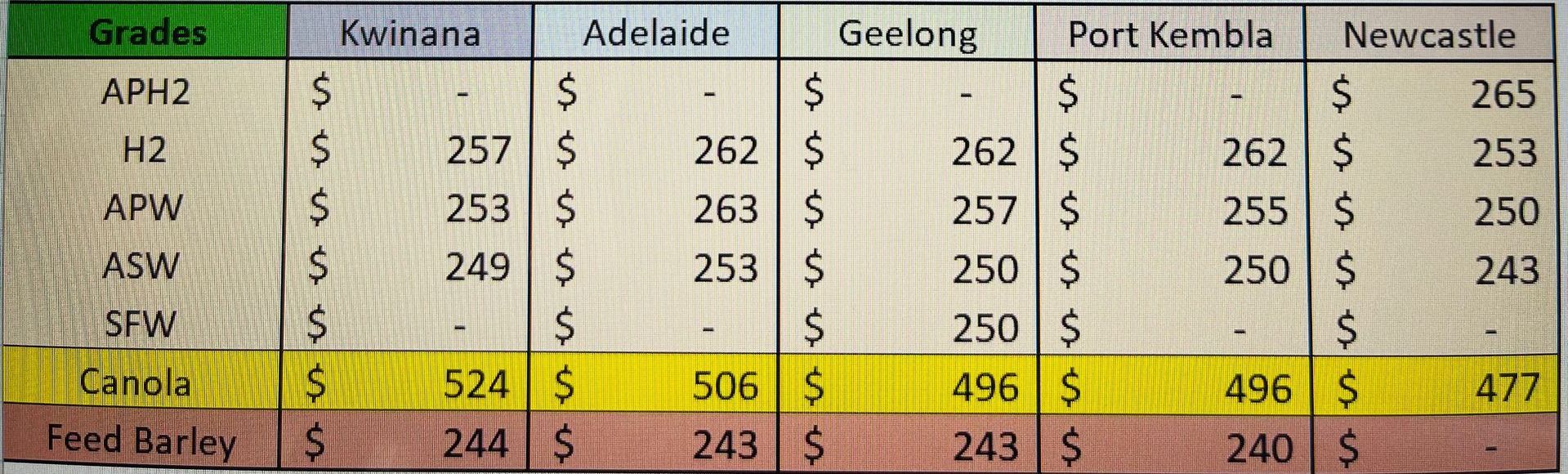

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

A significant amount of grain was bought and sold in the past week making it the largest trading week in more than a year as traders swooped up the cheaper farmer offers which became workable with a lower AUD weakened by Trump’s China Tariff increases. The 5% plus movement in the AUD through the week – both up and down also offered selling opportunities for farmers and exporters. Although it seems demand remained muted as a lot of consumers continued to sit on the sidelines – concerned about further volatility and improving global weather that may widen the emerging inverse to northern hemisphere new crop values further.

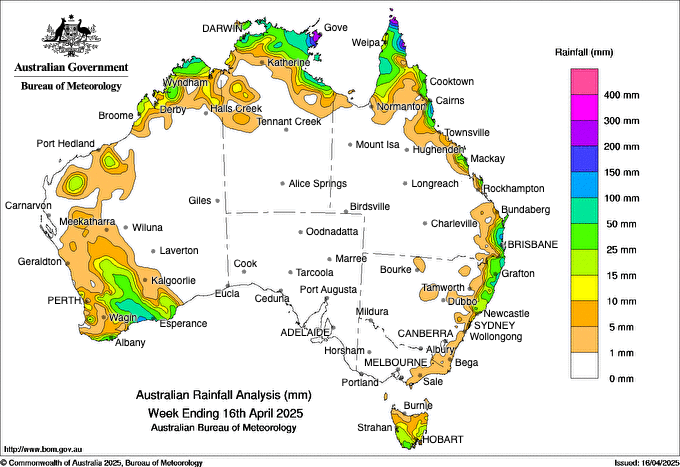

That said dry weather worries through South Australia (SA), Victoria (VIC) and Southern New South Wales (NSW) are building and is beginning to influence farmer decision making. Some farmers are holding off planting and we are also hearing southern farmers are holding back on forward fertiliser purchases they would normally be making at this time of the year due the dry outlook. Queensland (QLD) and Northern NSW on the other hand have received a good early break and Western Australia (WA) is also in fair condition. Soil moisture levels were near to above median in NSW, QLD, and WA, while below median in SA and VIC. The first week of April showed significantly above median levels in QLD, above median in NSW and WA, and a remaining soil moisture deficit in SA and VIC (below 80% of the median).

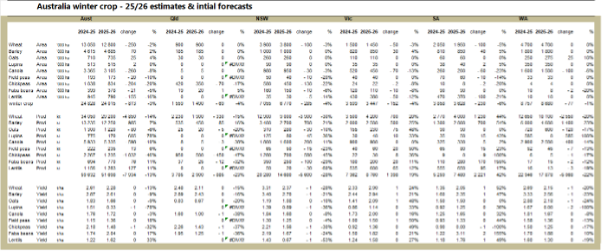

Elsewhere, our analysts released their initial 2025/26 winter crop plantings, yields and production estimates last week. Overall wheat plantings should remain steady, but we expect farmers will trim total plantings in South East Australia. This shouldn’t apply to areas that have enjoyed a favourable start to the season, such as Northern NSW and much of WA. Barley plantings in the big states of WA and NSW are expected to be large and steady.

Export Stem & Ocean Freight Market Update:

There was 800 thousand metric tonne (KMT) of wheat vessel nominations added to the shipping stem in the past week, 141KMT of sorghum, 121KMT of barley and 58KMT of canola. It was the largest week for total stem additions in eight weeks. WA accounted for around 540KMT of the weekly wheat additions followed by NSW with 166KMT and the Vic with 94KMT. All the weekly barley additions were in WA, and this is unlikely to change with the continued dry weather in South East Australia.

The dry bulk shipping market has also been grappling with geopolitical volatility, creating uncertainty as both shipowners and charterers continue to feel the associated repercussions. Freight rates have been up and down like a yo-yo, keeping everyone on their toes and making the decision-making process difficult for anything longer than 20-30 days forward. Not surprisingly the spot rates took a hit across all sectors last week with market players erring on the side of caution rather than being prepared to make a bold play either way. However interestingly, remaining relatively firm are owner’s period rates (though there has been little evidence of fixing) which indicates many are still looking for more evidence that the fundamentals have changed before they are willing to consider reduced levels. For now, it’s very much a wait and see game with cautiousness still the status quo on both side of the market.

Australian Weather:

Southern WA is expected to see more rain later this week as the tropical system close to the Kimberly region and unstable airmass influences weather patterns. This is expected to result in more for the Esperance area on Thursday and Friday. This may result in some light showers for SA and VIC on the weekend but limited to light showers. Eastern Australian cropping is expected to remain dry on the nearby models until the end of April. NSW and North East VIC will see coastal rain associated with the low in the Tasman Sea.

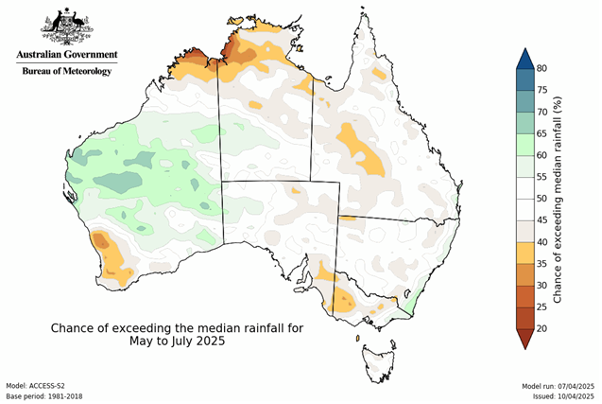

March 2025 recorded slightly higher-than-forecast precipitation across all states (135% vs. 120% of the median forecast). The latest April 2025 forecast shows significant above-median rainfall in NSW, QLD, and WA (>150% of the median), but lower estimates in SA and VIC (~50% of the median). The May to September 2025 outlook remains above median across all states (~120%), with notably high rainfall in NSW and QLD, and near to slightly above median levels in VIC, SA, and WA.

8 day forecast to 23 April 2025

http://www.bom.gov.au/

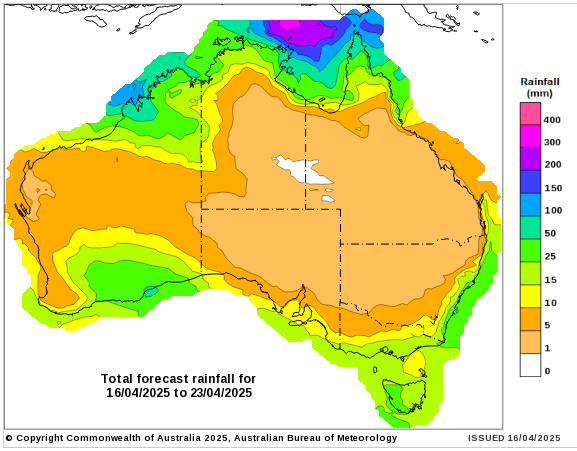

Weekly rainfall to 10 April 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The upbeat tone across the markets and a weaker USD helped the Australian dollar to a strong close to last week. The bullish tone for the AUD emerges as the US dollar (USD) continues to weaken across the board, dragged by lower-than-expected economic data and growing investor concern over inflation and trade policy. While momentum is cautiously improving, we don’t think volatility is going away any time soon.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.