Australian Crop Update – Week 15, 2025

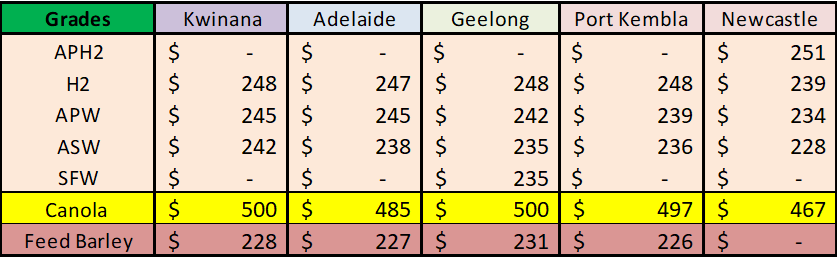

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Last week was quite volatile for global inputs as investors assessed the rapidly changing dynamics with Trump’s tariff agenda. US wheat futures finished the week steady while corn was firmer and French rapeseed lower. The Australian dollar ended the week sharply lower, although most of this was in Friday night’s selloff which won’t be reflected into local markets until Monday. The A$ fell 4% or 2.5 cents for the week to just over 60 cents to the USD.

The Australian domestic markets were quieter in the past week with only modest values changes. Northern grain selling has slowed following last week’s flurry following the soaking rains in Queensland (QLD) and Northern New South Wales (NSW). New crop wheat values drifted lower last week with the rain. In the cash markets, the trade buying interest is for the lower wheat grades, which is leading to a compression in the grade spreads. Southern markets are well supported by the ongoing dry weather across South East Australia. Barley is well supported in the south as well as other feed grains. Wheat bids in Western Australia (WA) were firmer for the week on exporter short covering. APW and ASW bids were up USD5-8 for the week. Barley was down USD3 per metric tonne (/MT).

Dry weather is set to shrink Australia’s 2025/26 wheat output by 16%, according to a poll conducted by Reuters. Australia is likely to produce 28.6 million metric tonne (MMT) of wheat in 2025/26, an average of five analysts and traders polled by Reuters shows, down 16.1% from 34.1MMT in 2024/25. However, there is a considerable spread between the forecast which ranges between 27MMT to 30.752MMT. Australia is being confronted with contrasting production outlooks for the 2025/26 winter crop. NSW and QLD are off to an ideal start with early soaking rains. The WA Great Southern is also enjoyed favourable rains in the past couple of weeks.

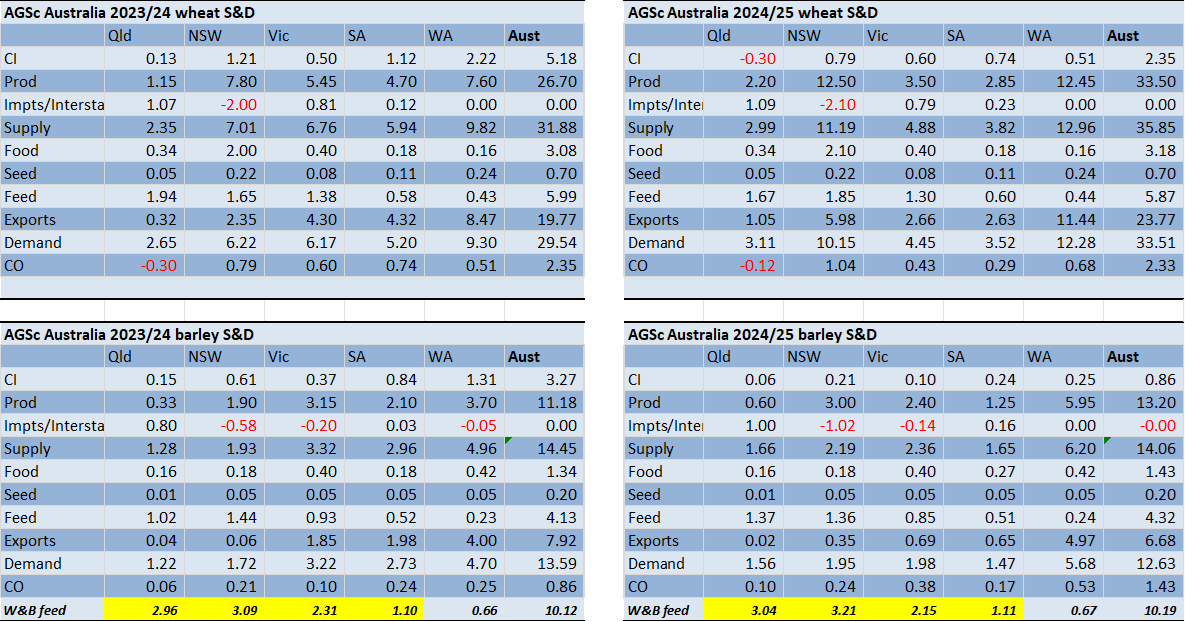

Australian Supply and Demand update:

Our Analysts have raised our forecast of Australia’s 2024/25 barley crop to account for the strong export pace. Heavy supplies of barley in QLD and Northern NSW also justify higher yield assumptions for the northern production areas of the east coast. National barley production has been raised to 13.2 million metric tonne (MMT). National wheat and canola production are little changed but the exports have been updated for the ABS actuals for October/November/December and stem forecast projections for the January/February/March quarter. We have kept national wheat exports close to 24MMT but the sluggish start to the program means more of the export task will be pushed into the July/August/September quarter when Australia competes with 2025/26 Black Sea supplies. The latest updates lift Australian wheat production to 33.5MMT, barley production to 13.2MMT, canola 6.0MMT and sorghum at 2.475MMT.

Source: AgScientia www.agscientia.com.au/

Australian Export Update:

Australia exported nearly 2.1MMT of wheat in February, close to 1.0MMT of barley and 0.526MMT of canola. Although wheat exports improved from the 1.85MMT in January, our current national 2024/25 export forecast of 21.8MMT requires a continuation of the 2.1MMT plus monthly exports from March to September if the forecast is to be achieved.

Wheat exports to China improved in February to 74.7 thousand metric tonne (KMT) but total shipments remain sharply below last year. The Philippines was the largest destination in February with 472KMT. This was a monthly record to the Philippines and slightly higher than the previous high of 459KMt in Jul 2023. Indonesia was the next largest with 338KMT, which is the largest monthly total to them so far for 2024/25. Thailand was the next largest with 352KMT, which was the most since Jun 2023. Australian wheat exporters are working to maximise sales into feed destinations with China’s lacklustre appetite for imports. There was also 52.5KMT of wheat shipped to Algeria in February.

Barley exports remain strong with 979KMT of shipments in February. WA dominated the February barley exports with 657KMT with South Australia (SA), Victoria (VIC) and NSW chipping in with cargoes. China accounted for 604KMT of Australia’s February barley exports, slightly back on the 703KMT in January. Other notables were 113KMT to Saudi (328KMt now for DJF) and 71.5KMT to Iran.

Canola exports remain strong with a further 526KMT shipped in February. This included 357KMT from WA and 159KMT from VIC.

Export Stem & Ocean Freight Market Update:

t’s been another modest week for shipping stem additions. There was 345KMT of wheat added to the stem in the past week. There was also 121KMT of canola, 113KMT of barley and 72KMt of sorghum (Newcastle NAT). Stem movements are reinforcing some underlying themes that have been evident in the local market for a while. These include - wheat export sales are difficult to make and this is leading to a slow export pace in the state’s where supplies are most plentiful. Sales are getting done, but probably not at the pace needed for the current 21.8MMT export forecast.

Another slow week marked by a lack of urgency and declining activity levels across all segments, and regional holidays combined with uncertainty on policymaking further dampened the likelihood of a short term recovery. The introduction of sweeping tariffs shifted the sentiment to a negative tone as the shipping market tries to come to terms with what real effect they will have going forward. The Pacific was quiet in all usual loading regions as rates slid from Monday to Friday. The exception to this was early in the week, there was a surprising steady flow of handy size backhaul steels in the Feast which helped support initially however this was short lived and faded as the week progressed. The North Atlantic was depressed all week but the south was supported and held steady off the back of ECSA activity. The paper market continues its downward trajectory, with the outlook for 2025 shifting back to a more negative tone. It’s hard to discern where a shift in momentum will come from right now however, as seen earlier this year, conditions can change rapidly.

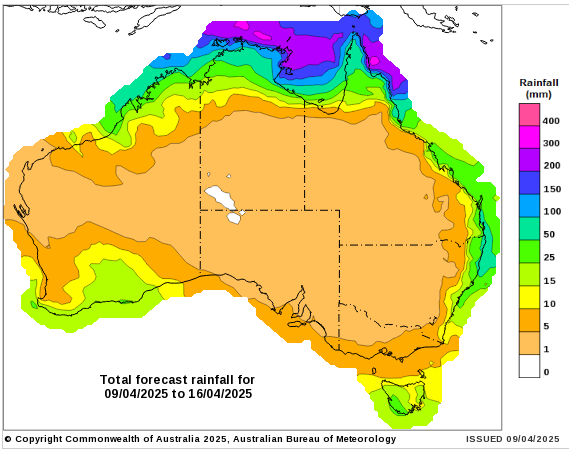

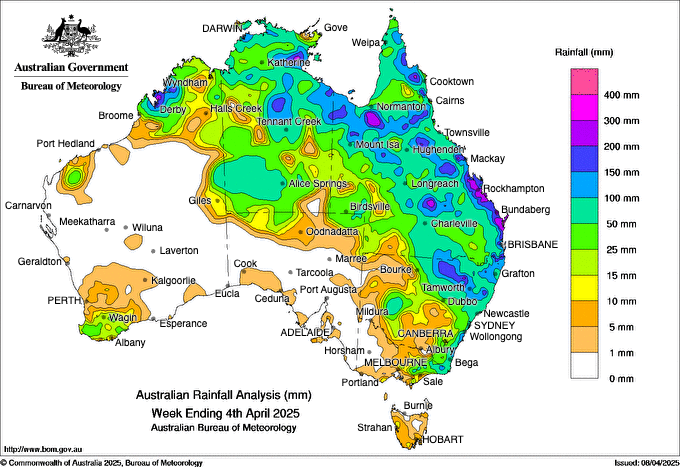

Australian Weather:

As famer in South East Australia anxiously wait for the traditional Autumn break, the latest Bureau of Meteorology (BOM) outlook indicates the drier pattern may persist. In its latest climate outlook statement for April to July, the BOM said rainfall is expected to be within the typical range for April to June for most of Australia. However, parts of southern Australia have a slightly increased chance of below average rainfall for the three months.

8 day forecast to 6 April 2025

http://www.bom.gov.au/

Weekly rainfall to 4 April 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar is heavily weaker to close last week trading at 0.6008 surpassing the low recorded in 2020 at the start of the Covid-19 pandemic. The drop follows an intensifying trade standoff between America and China, which saw Beijing slap an additional 34 per cent tariff on all US imports on Friday in retaliation for similar US levies. Markets now expect the RBA to potentially deliver back-to-back rate cuts in the next few meetings, with some banks even forecasting a 50 bps move in May.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.