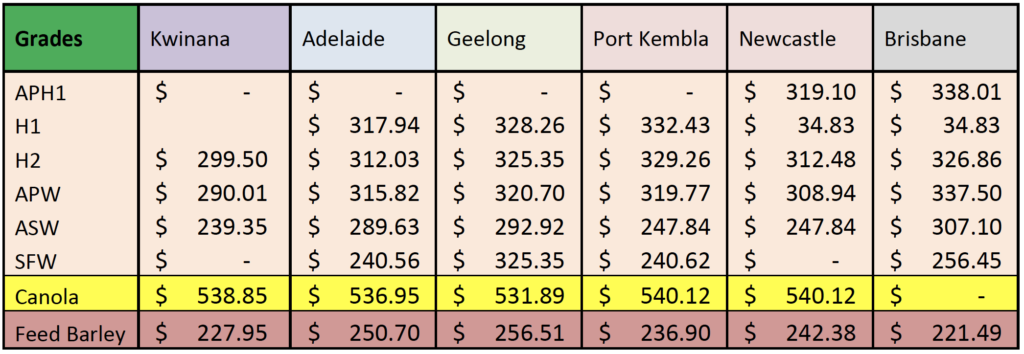

Basis Commodities – Australian Crop Update – Week 41 2022

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

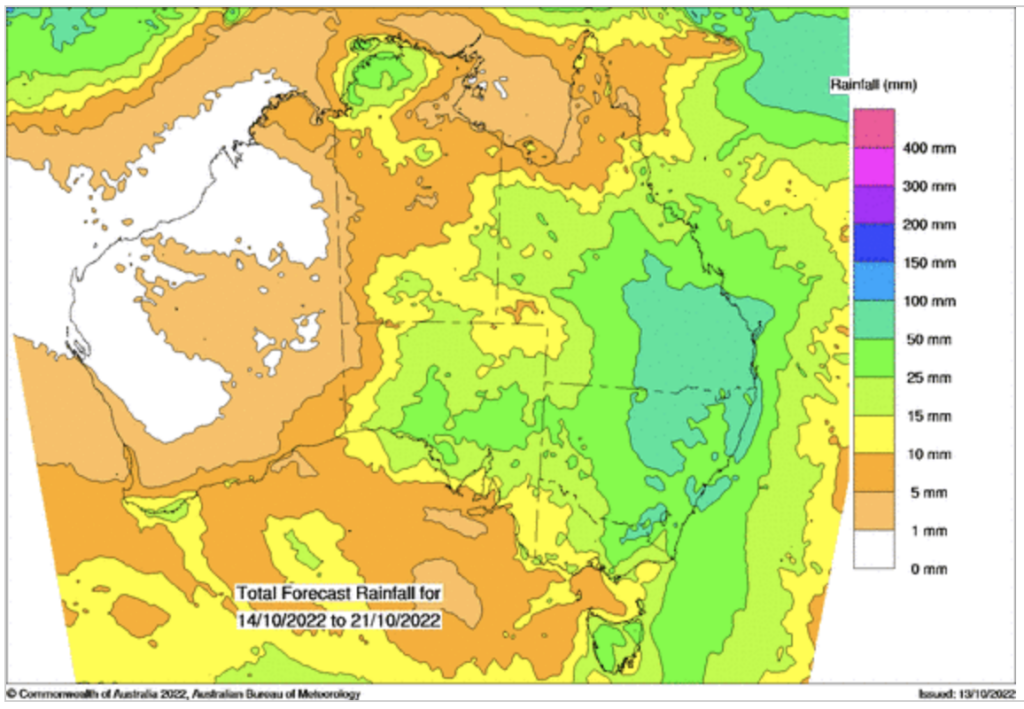

The Bureau of Meteorology released its latest long-range forecast for Australia, and eastern and Northern Australia seem set for a wet summer and autumn. Victoria received heavy falls early this week and more is on the forecast for Victoria, New South Wales, and Queensland over the coming days. Western Australia continues to escape the rain as harvesting picks up pace and South Australia continue to pick up yield.

Southern Queensland is unlikely to start harvesting for another 3-4 weeks (a month late) and most of NSW is saturated. This will impact pre harvest activities as well as harvest itself. Farmers are already behind in windrowing canola because it’s too wet. Recent rain only makes this worse. Harvest activities are going to be impacted as well as paddocks won’t take the weight of harvesting equipment, field bids and trucks. It’s going to be long harvest on the east coast with NSW being the epicentre of the problems for a second consecutive season.

Global grain markets are beginning to pay more attention to the excessively wet weather across eastern Australia with rain threatening to spoil the quality of another big east coast harvest and possibly lead to the spectre of significant crop abandonment.

Analysis of the NDVI’s for the various states in early October reveals the state by state story:

- Central Queensland is better than last year but not as good as 2016.

- Southern Queensland is better than last year but not as good as 2016.

- In New South Wales a late start and wet weather have held back vegetative conditions vs Qld and Vic which haven’t been as wet, or late. Crops are suffering.

- In Victoria, the Mallee is better than 2016 which was their best ever. Wimmera is better than last year by a little, but not as good as 2016.

- Most of South Australia is in good shape and is adding yield after a late start to the planting season and mild weather.

- In Western Australia, the Geraldton and Kwinana zone better than last year, while the upper Great Southern is about the same.

New crop bids were firmer this week as domestic consumers took quality cover as the ongoing rain threatens the quality of upcoming east coast wheat harvest. ASX wheat, which is for APW, has rallied by close to $50/MT over the past three weeks. Old crop barley bids were sharply higher on old crop squeezes which is normal for this time of the year, but they will probably last longer than normal given the lateness of harvest and the wet outlook. Old crop barley bids are up to $375/MT Melbourne. The grower remains a reluctant seller given the weather risks they’re facing as well as quality concerns, higher input costs and the volatility caused by wider geopolitical concerns.

Ocean Freight

The freight market in Asia seems to be well supported. Although, it is difficult to determine that we are on a longer-term upwards trend particularly when you see the cliff face in the FFA paper market for 2023, which drops in the region of 13k pd for Q1 2023 and the clear discrepancy between the physical and paper markets. Bunkers have firmed in the last week with the oil price rise. Backhauls from the Pacific to the Atlantic remain a dilemma/point of contention with different owners attaching very different values to it.

Australia Export Pace and Logistics

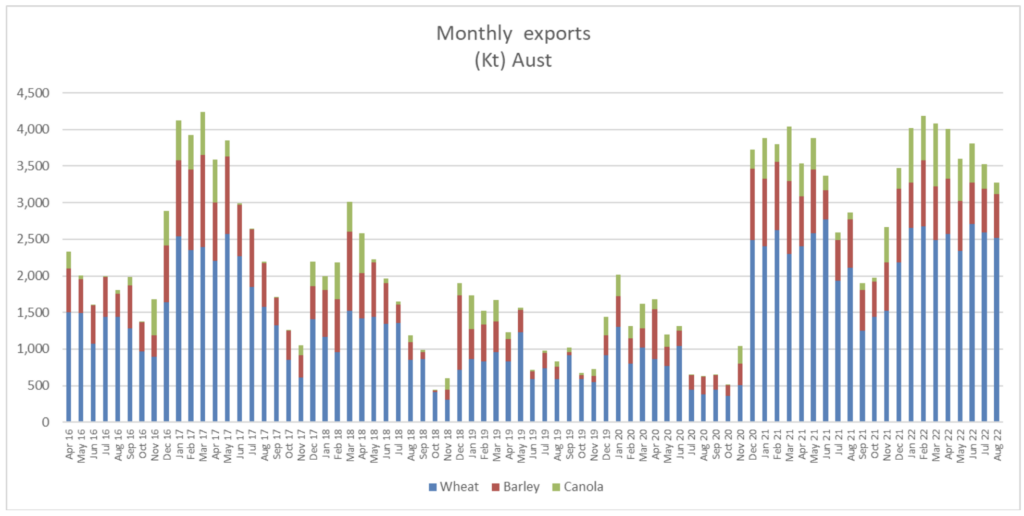

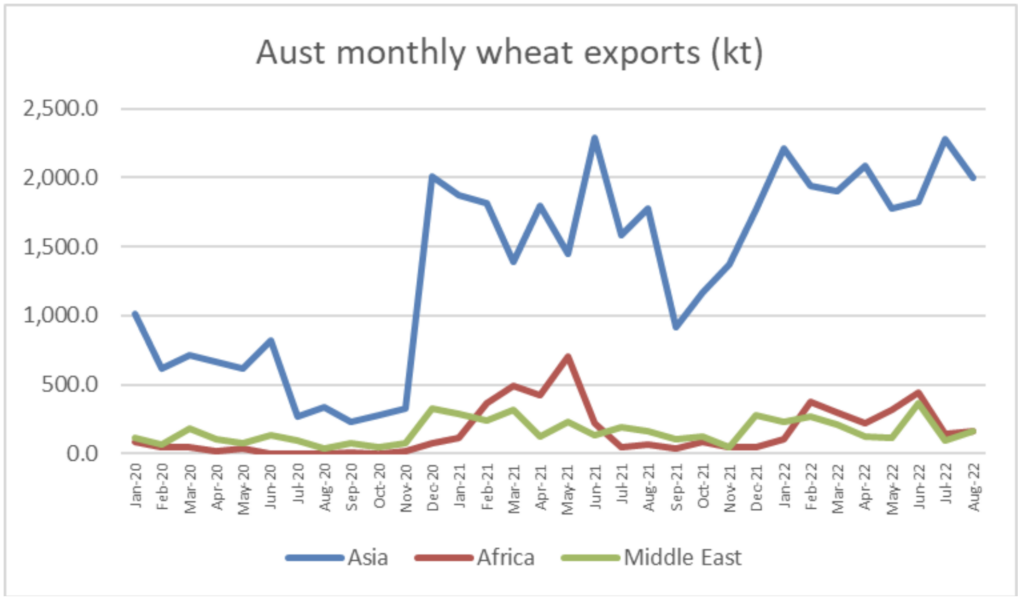

Australia exported 2.52MMT of wheat in August, modestly below the 2.6MMT in July and the 2.71MMT in June. This lifts the Oct/Aug exports to 25.7MMT. Western Australia has already shipped 9.4MMT of wheat so far for the 2021/22 marketing year, and New South Wales 6.0 MMT. Indonesia was the largest destination for August with 444KMT followed by Philippines with 420KMT, then Vietnam with 322KMT followed by China with 308KMT. Australia has shipped 5.8MMT to China in the Oct/Aug period.

Barley exports for August were 602KMT up from 591KMT in July. WA accounted for 426KMT of the August exports. Saudi took 323KMT with Japan the next largest at 61.4KMT.

Sorghum exports for August were 253KMT with 242KMT of this heading to China. There was 184KMT of sorghum shipped from Brisbane in August.

Canola exports in August fell to 152.5KMT down from 336KMT in July and 540KMT in June. Nearly all came from Victoria.

Ships scheduled to load in NSW slipped back by around a week. More heavy rain is forecast across East Coast in the next week which will add to the delays. It is shaping up to be another tough season for grain logistics with big crops keeping pipelines running at or near capacity and this will need to be borne in mind by consumers when planning their purchases. As far as we can tell, China is well progressed with its new crop purchasing – mainly low protein ASW – along with Southeast Asian consumers and as a consequence there is very limited stem available before February/March.

Australian Dollar

Risk aversion has dominated the currency markets this week with the AUD losing ground to a stronger USD. This mood looks set to continue with the AUD likely to test lower at some point in the fourth quarter, although the Reserve Bank is making noises about a balanced approach to interest rates – it’s not just about inflation, it seems the GDP growth gets a look in at times.

USDA Report Summary

Wheat:

USDA cut the U.S. crop as flagged in their Sept 1 stocks report. USDA lowered U.S. wheat exports by 1.4MMT to 21.1MMT. Argentina’s crop was lowered by 1.5MMT to 17.5MMT with exports down 1MMT to 12MMT. Australia’s crop is unchanged at 33MMT. Russia is also unchanged at 91MMT while the global trade is modestly lower. EU crop was raised 2.7MMT to 134.8MMT and exports were increased by 1.5MMT to 35MMT.

Corn:

The USDA forecast U.S. corn production at 13.895 billion bushels, based on an average yield of 171.9 bushels per acre. Analysts, on average, expected a 13.885-million-bushel crop with an average yield of 171.8 bushels per acre. USDA lowered U.S. exports. USDA lowered China’s 2021/22 imports by 1MMT to 22MMT and left 2022/23 unchanged at 18MMT. USDA raised Ukraine 2021/22 and 2022/23 each by 2.5MMT. EU 2021/22 wheat imports were raised by 2MMT to 20MMT and 2022/23 imports up by 1MMT to 20MMT. EU corn production trimmed.

Barley:

Raised EU crop by 1MMT to 51.1MMT. EU exports unchanged. Ukraine crop unchanged but exports up by 0.6MMT to 2.4MMT. USDA cut Australia’s 2021/22 exports by 0.8MMT to 8.2MMT. 2022/23 Australia’s crop unchanged at 12.2MMT and exports unchanged at 6.7MMT. Australia’s 2022/23 ending stocks raised by 0.8MMT on the back of smaller 2021/22 exports. Global imports largely unchanged with Saudi imports unchanged at 4.7MMT and China at 9.5MMT. USDA raised Saudi’s 2021/22 imports by 0.3MMT to 4.5MMT.

Canola:

Rapeseed production for the EU has increased 1.0MMT to 19.2MMT on higher production for France, Germany, and Poland. Partly offsetting this is a 0.5MMT reduction to 19.5MMT for Canada’s canola crop on a lower yield. China’s canola imports are lowered 0.5MMT to 2.3MMT reflecting lower Canadian supplies.

The post Basis Commodities – Australian Crop Update – Week 41 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.