Basis Commodities – Australian Crop Update – Week 40 2022

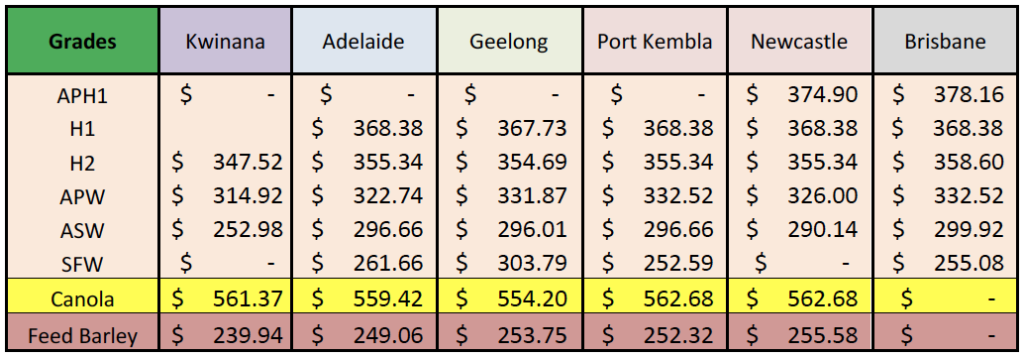

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

As we tick into the 22/23 crop year, the above table is our view of “replacement FOB numbers” for the main wheat grades, barley, and canola across the main port zones. It is important to bear in mind that these prices are composed of the track bid/offer spread for the grade/zone plus our view of accumulation and fobbing costs. This is NOT an offer or indication to sell at these levels, but we believe it is useful for our clients to gauge a rough idea of protein spreads between wheat grades. It also helps inform buyers with respect to elevation margins on each commodity and therefore the likelihood, or not, of FOB sellers putting wheat, barley or canola on the stem which is an increasingly important feature of the Australian cash markets in a big crop year.

As with the crop year just gone, we need to bear in mind that with another big wheat, barley, canola, oats, fava beans, chickpeas and lentils crop on the way, the commodity being sold at the FOB point is access to export logistics. Therefore, as with any market, the highest bidder or commodity with the largest elevation margin will be prioritised, and this may run counter to our fundamental analysis of a commodity’s worth at the FOB point.

Market Update

It was an interesting week for the local grain markets. This was not so much in market activity, which was mostly steady in the trade. However, there were some notable changes in the zonal pricing structures as buyers become more nervous about the ongoing rain on the east coast and the impact this will have on grain quality. ASW continues to be priced at big discounts to APW in all zones working back into Asian feed wheat values. New crop barley bids are being priced as the cheapest feed grain in the world on a farmer replacement basis, but this is not being seen at the FOB point as wheat outcompetes barley in the battle of elevation margins.

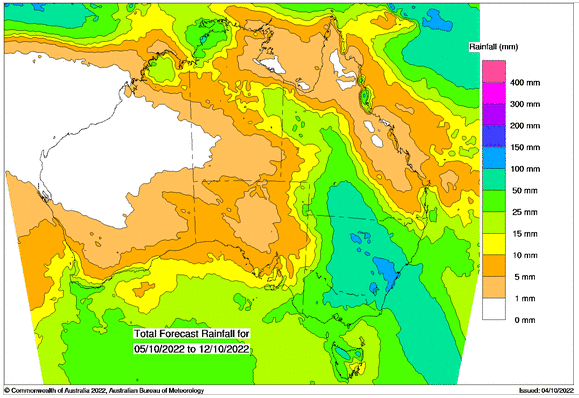

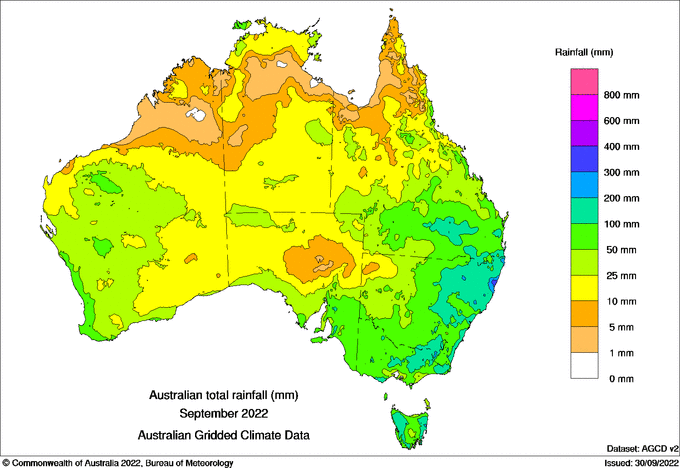

Wetter than normal September weather has locked in another massive Australian winter crop harvest. Below is the monthly rainfall map which shows just how wet it has been. NSW has been the epicentre of the rain where most of the state’s cropping areas have seen double the normal September rainfall with parts of northern NSW seeing up to four times the monthly average. The excessive rain has also extended north into Qld and south into Vic. More concerning is the outlook. All of NSW and Southern Qld are expected to see another 25-50mm in the coming days, which will only add to the current problems and looming quality concerns.

The extended outlook is also a worry. The Bureau of Meteorology said October to December rainfall is likely to be above median for the eastern half of Australia, but below median for the west coast and the northern and central Western Australia. Mostly dry weather is giving exporters some confidence that activity will ramp up in WA in the coming weeks. The same can’t be said about the east coast. The cool, wet season is expected to put the harvest dates back by around two weeks behind average. However, this could be put back even further if the rain doesn’t let up. Wheat harvest is just starting in Central Queensland. Southern Queensland won’t start until late October, possibly later, which will have a knock-on effect on new crop shipping programs which will be delayed.

Quality is clearly a big flag for the upcoming harvest and will need to be watched closely.

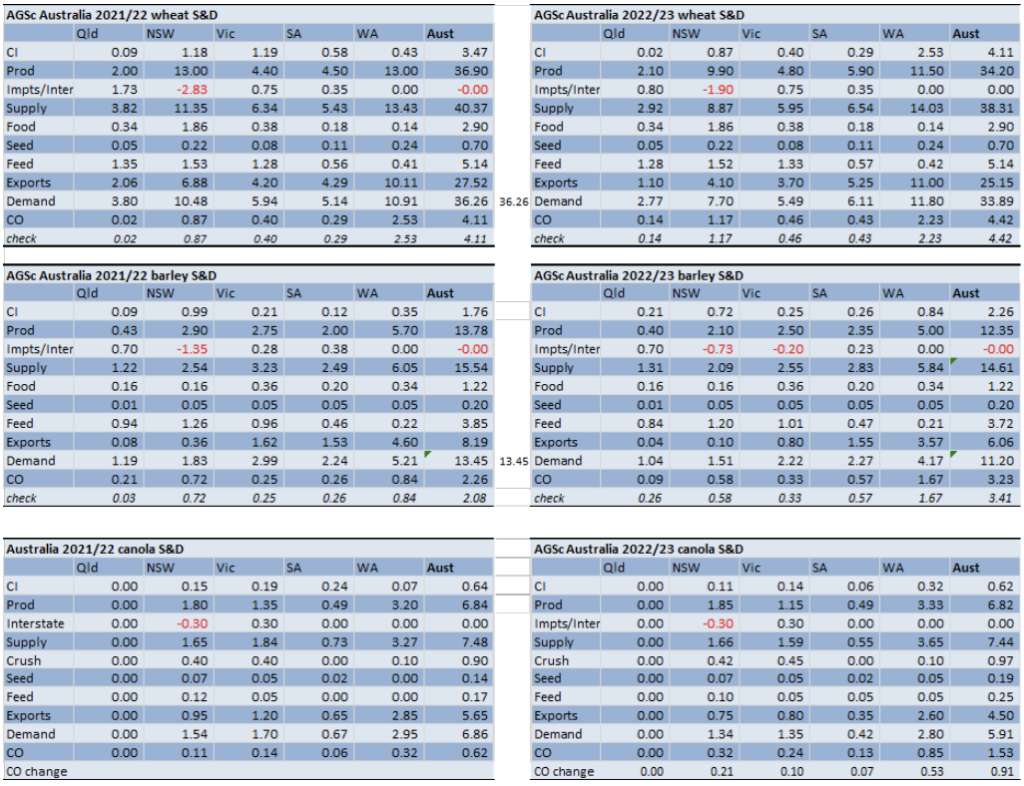

AgScientia Australian Balance Sheet update

It’s shaping up to be the second largest winter crop behind last year. Our analysts have just raised their forecast for Australia’s 2022/23 wheat harvest to 34.2MMT. Barley production is pegged at 12.35MMT and canola production at 6.8MMT. Wheat production is up on our August update on the back of a significant yield increase in South Australia and smaller increases in Victoria and Western Australia. This isn’t the case in New South Wales where crops continue to struggle with the late planting dates and excessively wet conditions in most areas.

The only change to domestic consumption is a 5% increase in dairy grain feeding in most states on the back of good returns.

Australia’s 2022/23 wheat exports are forecast at 25.1MMT, down from the 27.5MMT forecast for 2021/22. Barley exports are forecast at 6.1MMT but can go higher if demand permits. Canola exports for 2022/23 are forecast at 4.5MMT down from last year’s 5.6MMT.

Australia’s wheat stocks are forecast to edge higher to 4.4MMT from 4.1MMT in 2021/22. Western Australia’s carry-over remains large at 2.2MMT which is a function of the export capacity constraints. New South Wales carry-over stocks edge higher to 1.2MMT but it’s not a burdensome number for the state with its large domestic demand base. Australia’s barley stocks swell to 3.2MMT which is 1MMT up on 2021/22. Australia’s canola stocks also climb to 1.5MMT, which is up 0.9MMT on 2021/22.

Seasonal conditions are clearly very similar to last year and this is what’s allowing for the well above average yield assumptions. There is a concern we will also see another year of below-average proteins. This is a concern for the domestic food market, but it also restricts the export markets where the surplus can be shipped to.

Shipping Stem and Ocean Freight

It was a quiet week for shipping stem additions with a lot of participants away as they take advantage of the public holidays in various states and across Asia. There was 277KMT of wheat added to the stem in the past week as well as 135KMT of barley and 35KMT of sorghum.

The Ocean freight market continues to move sideways although sentiment suggests further market weakness is just around the corner, although that may be more a factor of the Golden week holidays this week. The Atlantic and Pacific markets are basically trading at parity now, but it looks like the Atlantic will soon become a premium – returning us to a more traditional market profile where back-hauls have their purpose which is good news for our friends in the Red Sea and the Mediterranean.

Australian Dollar

Markets remain extremely volatile with thin liquidity and a declining macro picture making it difficult to have a clear view of the longer-term trend for the AUD. Having touched intraday lows at US$0.6363 last week, the AUD seemed set on plumbing new lows against the USD and may still do so. However, the UK government’s U-turn on fiscal policy helped ease tensions and allowed the AUD to recover near 2% climbing back above US$0.65 to mark intraday highs at US$0.6520.

Our attentions turn now to RBA policy update. Momentum for another 0.50 basis point hike has built through the last 30 days as persistent signs of inflation and a robust labour market support a sustained and aggressive tightening of financial conditions. Key will be how the RBA signals or justifies any future slowdown in the pace of future hikes.

The post Basis Commodities – Australian Crop Update – Week 40 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.