Australian Crop Update – Week 9, 2025

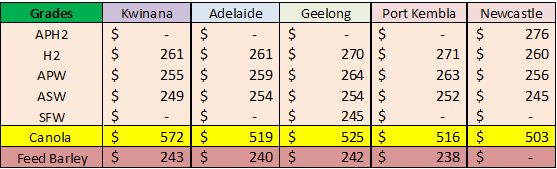

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

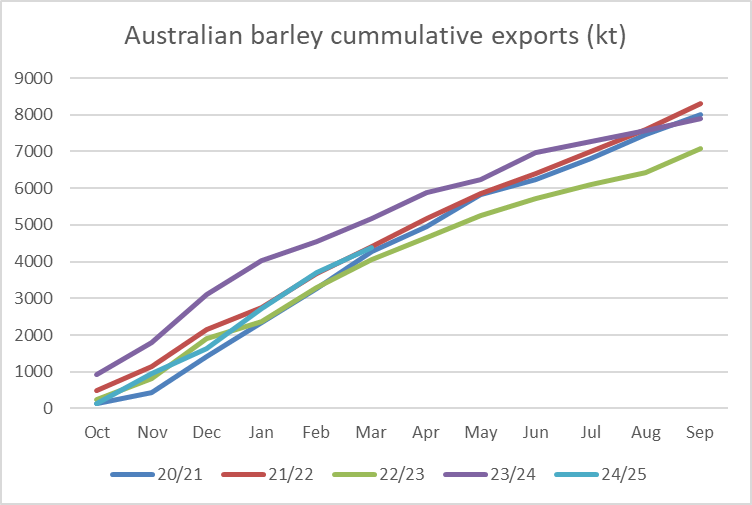

Hot on the heels of our previous delayed report the Australian domestic wheat and barley bids have strengthened across eastern Australia in line with gains in global markets over the past week. Gains were sharpest in Queensland (QLD) and Northern New South Wales (NSW) where they are playing catchup to other values in southeast Australia. Reserved farmer selling is also offering support, where farmers are selling but not enough to keep the improving export pace satisfied.

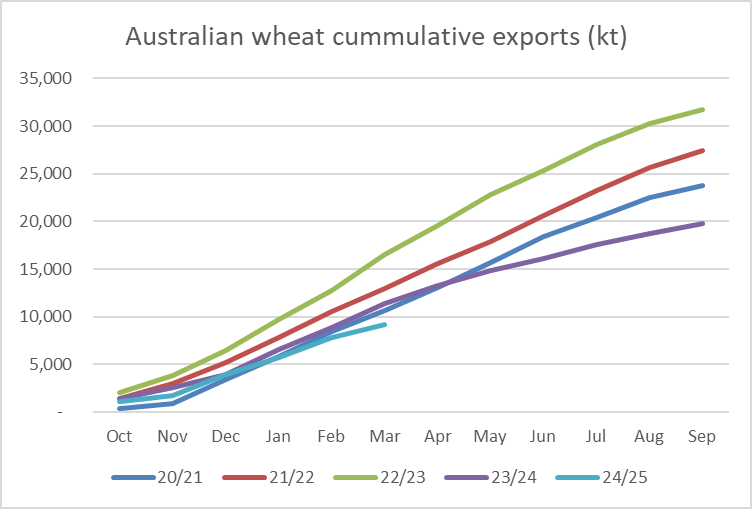

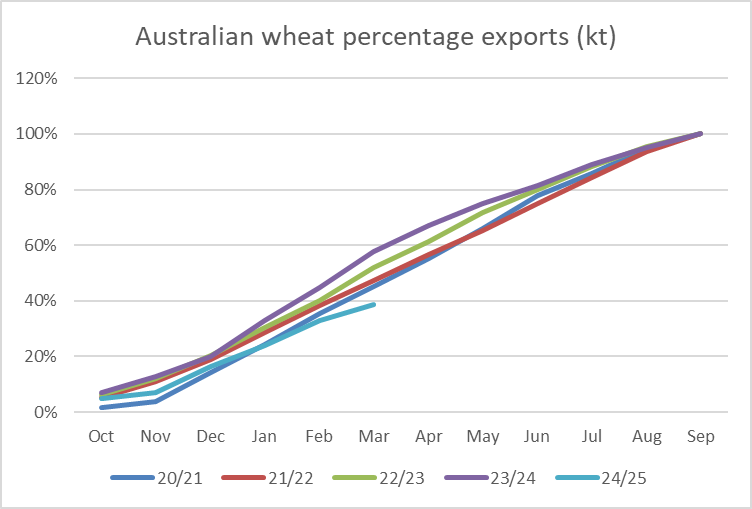

Exporters have been getting their share of export sales on in recent weeks given that Australian wheat has been increasingly competitive. This was evident in the Australian Bureau of Statistics exports where monthly shipments into the Middle East countries were the largest in more than a decade in December. Shrinking Black Sea supplies is playing its part in this as well as the Russian export restrictions than came into force in mid-February.

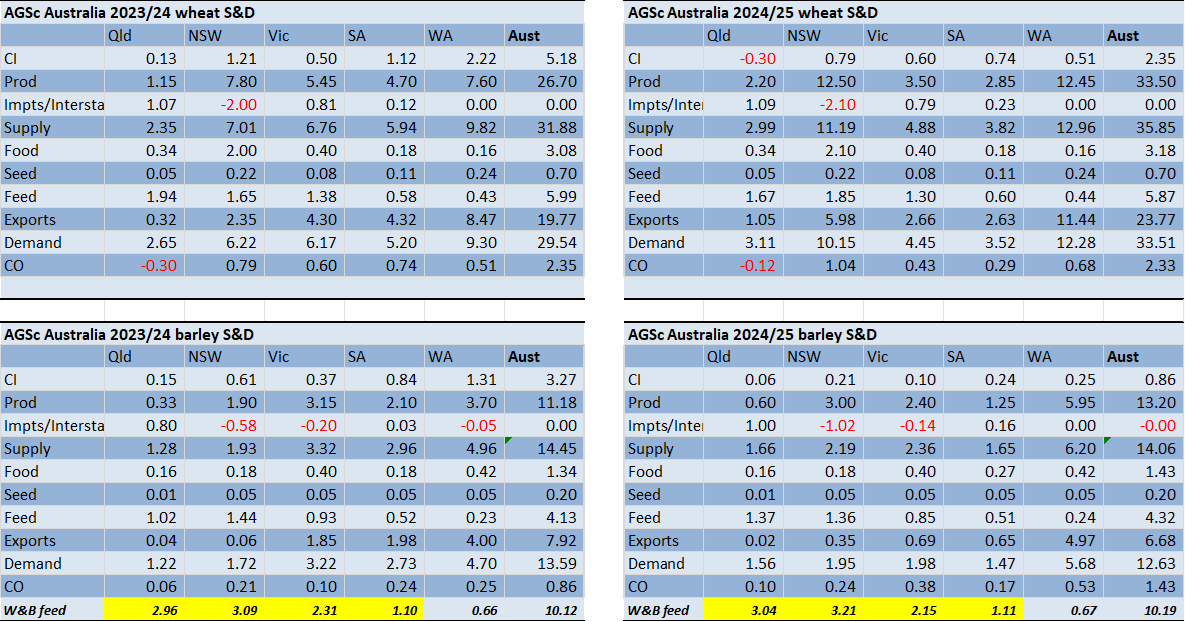

Australian Supply and Demand update:

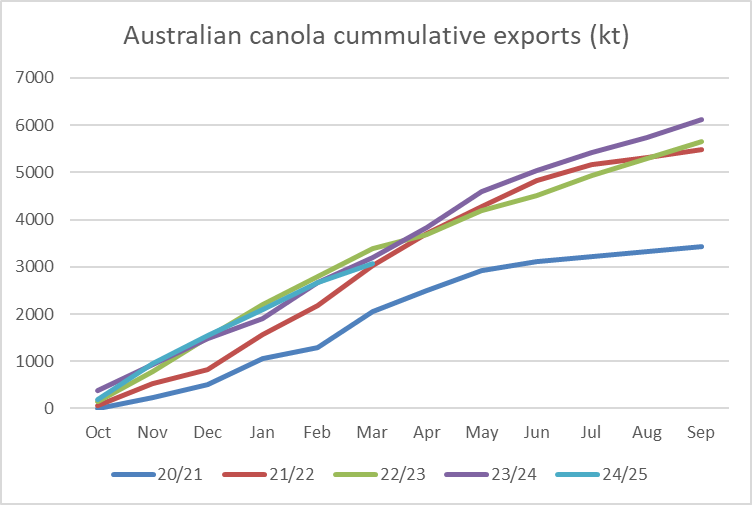

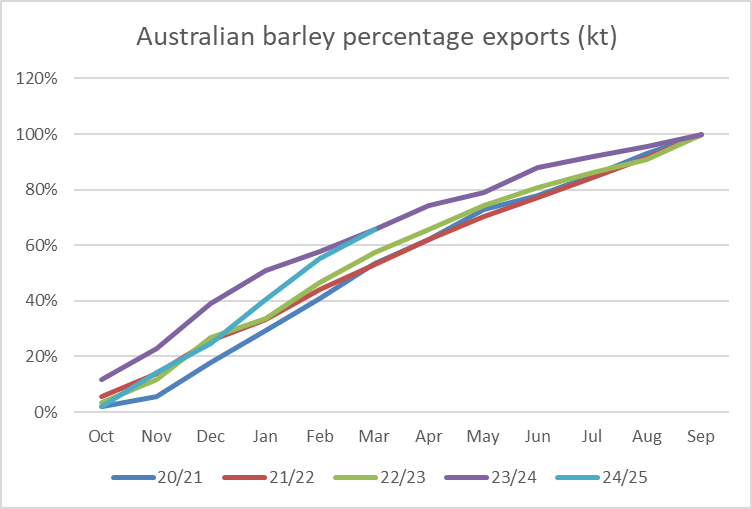

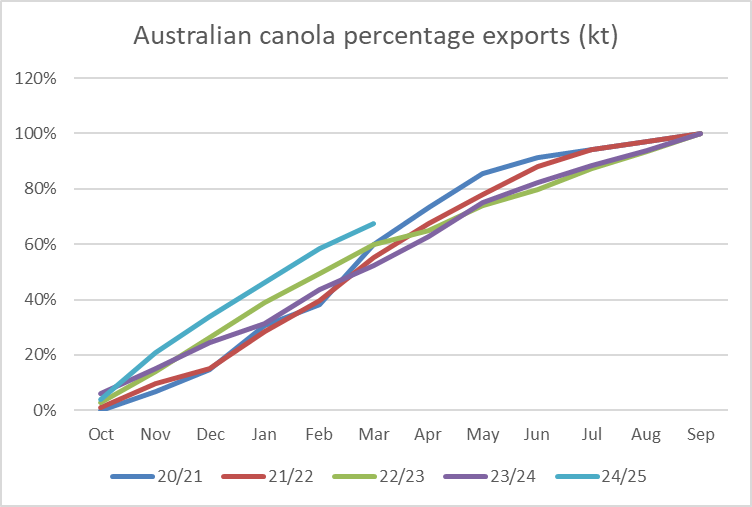

Our Analysts have raised our forecast of Australia’s 2024/25 barley crop to account for the strong export pace. Heavy supplies of barley in QLD and Northern NSW also justify higher yield assumptions for the northern production areas of the east coast. National barley production has been raised to 13.2 million metric tonne (MMT). National wheat and canola production are little changed but the exports have been updated for the ABS actuals for October/November/December and stem forecast projections for the January/February/March quarter. We have kept national wheat exports close to 24MMT but the sluggish start to the program means more of the export task will be pushed into the July/August/September quarter when Australia competes with 2025/26 Black Sea supplies. The latest updates lift Australian wheat production to 33.5MMT, barley production to 13.2MMT, canola 6.0MMT and sorghum at 2.475MMT.

Source: AgScientia www.agscientia.com.au/

Export Stem & Ocean Freight Market Update:

Shipping stem additions were significantly smaller in the past week following the previous week’s 1.7MMT. There was 380 thousand metric tonne (KMT) of wheat, 125KMT of canola and 65KMT of barley put on the stem in the past week.

After a quiet start to the week for Panamax, rates started to gain ground by Wednesday to finish the week on a stronger note. The Pacific sparked to life off the back of some grain demand ex Aussie and Nopac. For Supramax/Ultramax it was another positive week in the Pacific, mainly driven by sustained demand in the Fareast and Nopac markets (mostly steels and grains) which has pushed rates along. Interestingly, Australia is lagging due to minimal fresh demand for this sector. The Handysize market has followed a similar trend in Asia, with the Fareast being the best performer over the week. Overall, there has been a wide range of reported fixing rates for all types which indicates the market is still working to find its equilibrium.

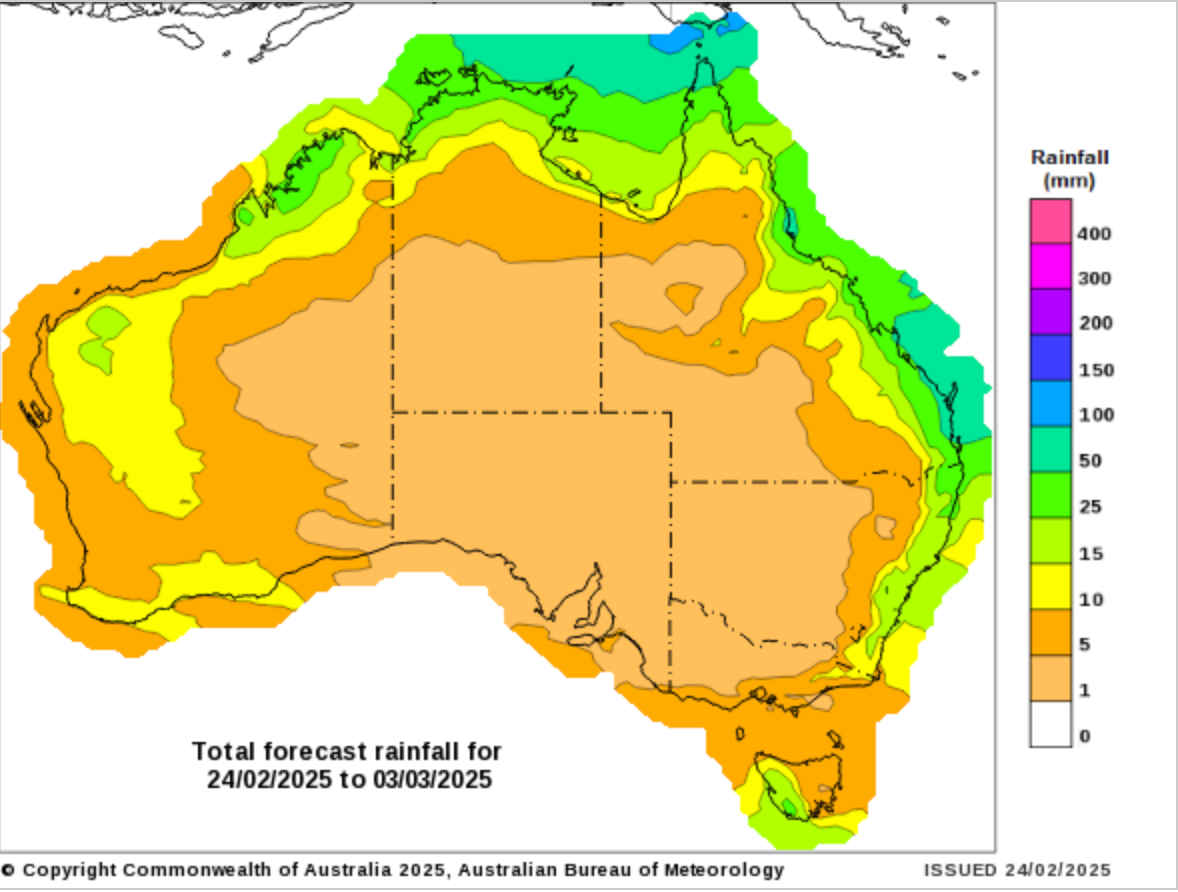

Australian Weather:

Southern QLD and NSW received some patchy rain last week. Broadly, QLD and NSW farmers are sitting on good soil moisture reserves ahead of autumn planting dates which has farmers comfortably positioned. Victorian (VIC) and South Australian (SA) farmers are keen to see soaking rains where grain farmers have seen little to no rain since early December. Subsoil moisture reserves are well down on this time last year and soaking rains are needed before winter crop plantings in April and May. Nearby forecasts remain dry. Extended Bureau of Meteorology models point to improved rain in late February returning to normal rainfall patters for March-May.

8 day forecast to 3 March 2025

http://www.bom.gov.au/

Weekly rainfall to 24th February 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar remained static to end last week when valued against the Greenback closing at 0.6350. Having given up fresh 2025 highs above US$0.64 the AUD slid to session lows only marginally above US$0.6350. Uncertainty surrounding the new Trump administration's economic policies and a sell off across US equities sparked a sharp uptick in risk aversion driving markets to haven assets and away from the AUD.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.