Australian Crop Update – Week 8, 2025

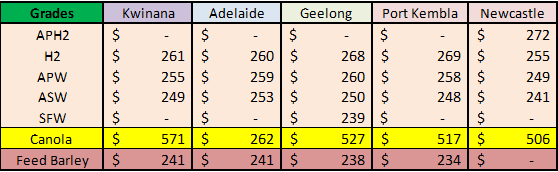

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Australian domestic wheat and barley markets were stronger across most port zones, with the exception of Western Australia (WA), in the past week as buyers lifted bids to chase elusive farmer selling. The AUD was 1.3% higher for the week as the US lost some of its gloss following the Trump election victory.

Australian 2024/25 Production Update:

Forecasters have raised production estimates of Australia’s 2024/25 barley crop to account for the strong export pace. Heavy supplies of barley in Queensland (QLD) and Northern New South Wales (NSW) also justify higher yield assumptions for the northern production areas of the east coast. National barley production has been raised to 13.2 million metric tonne (MMT).

National wheat and canola production are little changed. National wheat exports are estimated for the season to be close to 24MMT but the sluggish start to the program means more of the export task will be pushed into the July/Aug/Sept quarter when Australia competes with 2025/26 Black Sea supplies.

The latest updates lift Australian wheat production to 33.5MMT, barley production to 13.2MMT, canola is 6.0MMT and sorghum production at 2.475MMT.

Export Stem & Ocean Freight Market Update:

It was a big week for the shipping stem last week with a combined 1.7MMT of wheat, barley, canola and sorghum added. Wheat made up 850 thousand metric tonne (KMT) of the total, comprising 655KMT in WA and 175KMT in NSW. There was also approximately 400KMT each of barley and canola put onto the stem as well as 60KMT of sorghum in Brisbane.

It was a mixed week for shipping where we witnessed Capesize and Panamax lose ground while the Supramaxes and Handysizes continued to gain. The Atlantic came under pressure on the larger sectors as demand became scarce. As a result, charterers began to drive down their bid levels and left owners little choice but to accept or risk becoming spot/prompt in a falling market. The Pacific bucked the trend with a steady demand stream appearing ex Nopac and Aussie to help hold rates stable for now. The Supramaxes experienced another positive week with most loading zones being achieved in Atlantic and Pacific which helped owners to revise their offer levels upwards by another 1-2kpd. In the Pacific, we are also seeing an increased amount of FarEast back haul voyages appearing in the market. Charterers willing to pay healthy rates for long duration business could help position tonnage out of the Pacific and tighten the supply/demand equation in the east.

The Handysize have been steadily increasing since the Lunar New Year holidays and there is a renewed sense of optimism in the market. The Handy Pacific indexes have all increased circa 2000 points over the past two weeks and owners are pushing rates to the next levels with charterers having to now chase to secure tonnage. Period activity on all sizes remains healthy which has led to owners increasing offer levels up 1-2kpd depending on the duration and what optionality charterers need.

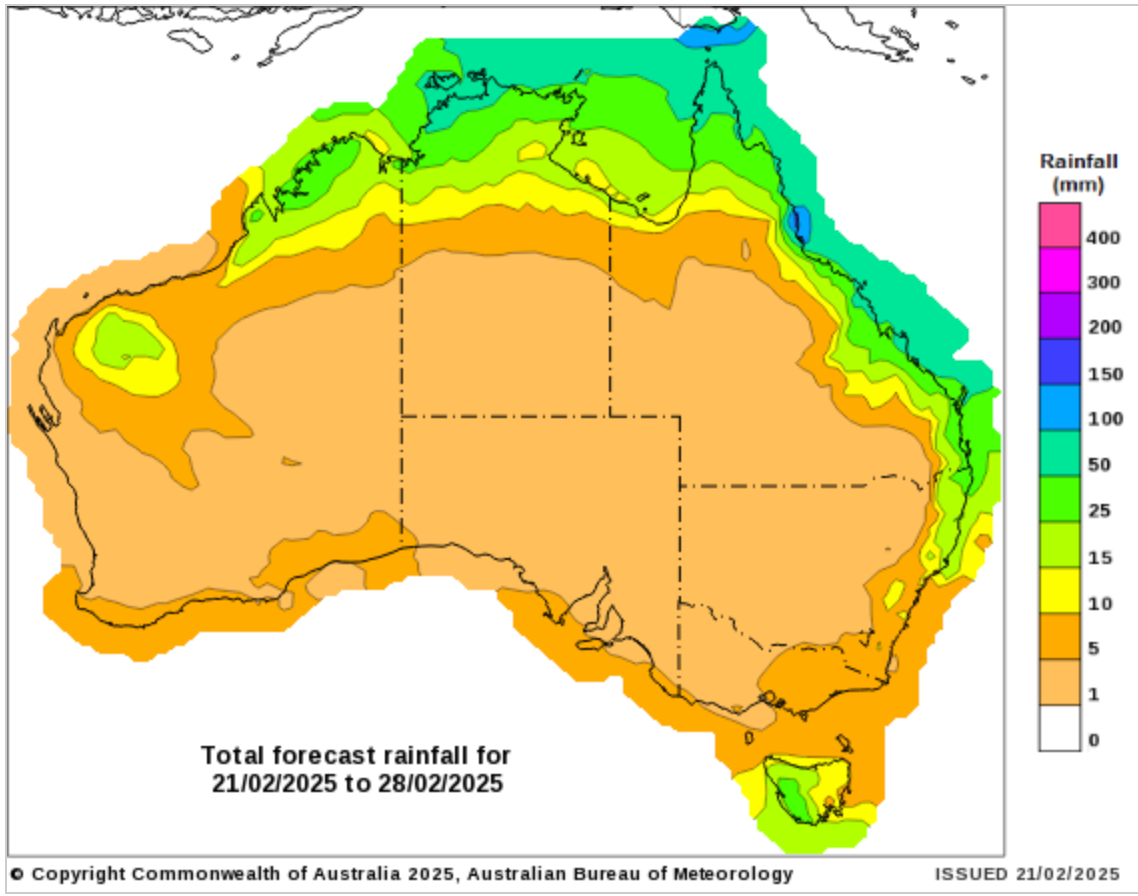

Australian Weather:

It was a good rainfall week for QLD and Northern NSW but dry elsewhere. Last week’s rain means these areas are well positioned for soil moisture ahead of Autumn/Winter crop plantings. Southern cropping areas remain dry and will be looking for Mar/Apr rain. WA is dry but that’s not unusual for this time of the year

8 day forecast to 28 February 2025

http://www.bom.gov.au/

Weekly rainfall to 20th February 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar was higher over last week when valued against the Greenback closing at 0.6354. The Australian dollar advanced Friday amid softer US retail sales data and dwindling tariff fears. While Trump's regime of reciprocity remains in sharp focus the threat of imminent tariffs has faded as officials’ analysis the US’s trade relationships with the intent of issuing country-by-country tariff programs. Having pushed through US$0.6350 the AUD touched its highest level since mid-December marking US$0.6368. This week we saw the expected 25 basis point interest rate cut, although the Federal Reserve remains cautious about flagging further cuts ahead of an impending general election campaign.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.