Australian Crop Update – Week 7, 2025

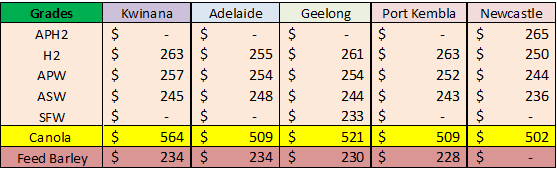

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Australian cash markets were firmer last week aided by the strength in US futures. The market felt like export shorts started to show a greater appetite to increase coverage as the AUD strengthened to help them. However, calculated FOB replacement wheat values were US$3-6 higher for the week.

Farmer selling remains slow. Overall, Western Australia (WA) is probably more than 50% sold on wheat, more on barley and mostly sold on canola. The size of the WA crop has surprised farmers which have left them more undersold than they thought. We get the impression that New South Wales (NSW) farmers would be volume sellers of wheat at values of +$5-10 above where the bids are.

The Australian Bureau of Statistics released its December grain export data which showed a sharp kick in wheat shipments and a huge month for chickpea shipments.

December wheat exports were 2.156 million metric tonne (MMT), up from 577 thousand metric tonne (KMT) in November. Exports to Asia were 1.46MMT and 593KMT to the Middle East which was the largest monthly exports in more than a decade. Let’s hope for more of the same!!

Barley December exports were 679KMT, down from 834KMT in November. China was the main market with 386KMT. There was 150KMT of barley shipped to Saudi Arabia as well.

On pulses, chickpea exports were huge at 781KMT. India took 75% of the December chickpeas. Lentils exports were also strong at 240KMT. Pulse exports exceed both barley and canola in December which is an interesting development. The chickpea figure has lifted exported for the first quarter of the shipping year to 1.3MMT, with the currently tariff-free Indian market accounting for close to 1MMT of that. The surge reflects Indian demand ahead of the expected reinstatement of the tariff in April, and the availability of a large, good-quality Australian chickpea crop which growers were happy to sell for cash at harvest.

On lentils, the December total exported was a more than five-fold increase on the November. This is again reflecting new-crop availability, and buoyant demand for a relatively low-volume Victorian (VIC) and South Australian (SA) crop, the result of a low-rainfall growing season. Australia’s main customers for December-shipped lentils were India on 114,365 metric tonne (MT), Bangladesh on 81,854MT, and the United Arab Emirates on 25,727MT.

Export Stem & Ocean Freight Market Update:

Exporters added 560KMT of wheat to the stem in the past week which lifts the additions in the past four weeks to 1.7MMT. It is apparent that export sales of wheat are still difficult to make whereby shippers are working hard to get sales on. It also flags that 2024/25 wheat exports may not reach the forecast 24MMT which will push up the carryover stocks in NSW and WA – something to be considered. It also means that traders have limited willingness to chase farmer supplies with a resulting stand off. Barley shipments and forward stem are already two thirds for the forecast 5.5MMT 2024/25 shipments which is 7 pts ahead of last year. Canola shipments are equally advanced. There was also 215KMT of barley added to the stem in the past week and 280KMT of canola.

There was a slow start to ocean freight last week post Lunar New Year holidays. There was a positive swing on the indexes and FFAs for the first time in weeks. Owners were less eager to chase Charterers. Instead, many were happy to sit and wait as the rates started to increase from late Wednesday through to Friday afternoon as increased cargo demand started appearing now that many market participants are back behind the desk. Owners have been resistant to take last done levels, and we have witnessed standard pacific rounds rates gaining 1-2kpd by the end the week. It will be interesting to see whether this positive sentiment continues – we are not so sure.

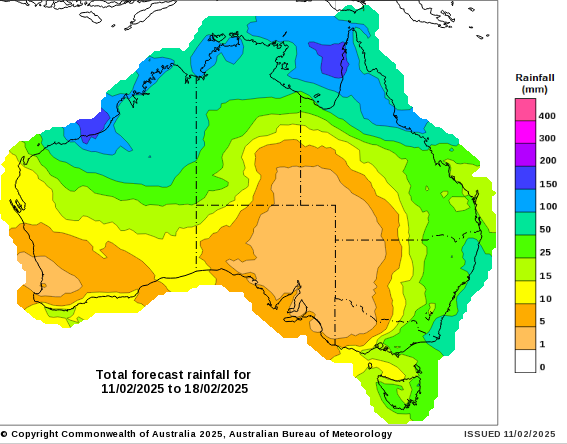

Australian Weather:

Subsoil moisture in the northern cropping areas is generally good ahead of autumn plantings while southern cropping areas are dry (not abnormal for this time of the year).

BOM’s extended weather outlooks offers a wetter than normal autumn for northern and southern Australia. The long-range forecast for February to April shows above average rainfall is likely for northern Australia and much of the south, with an increased chance of unusually high rainfall for much of these regions. For parts of southern WA and scattered parts of south-east Australia, rainfall is likely to be in the typical range for February to April. Warmer than average days are likely across much of southern and eastern Australia. Since late December, conditions across the tropical Pacific have been more La Niña-like, with both oceanic and atmospheric indicators beginning to align. However, until a sustained atmospheric and oceanic response is observed, the BOM’s ENSO status remains neutral.

8 day forecast to 18 February 2025

http://www.bom.gov.au/

Weekly rainfall to 11th February 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar was sharply higher over last week when valued against the Greenback closing at 0.6250. After plunging below US$0.61 on Monday the AUD proved remarkably resilient in closing the week higher yet remains ever so vulnerable to tariff headlines.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.