Australian Crop Update – Week 5, 2025

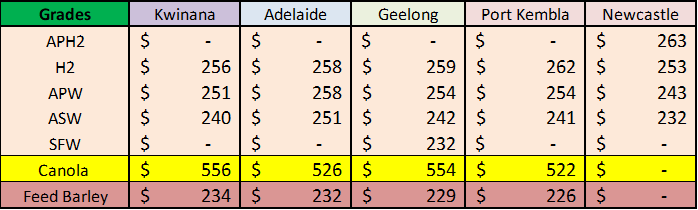

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Increased farmer selling and reports that Chinese buyers were trying to washout Australian wheat purchases and sell them back into Southeast Asian markets were behind the weakness in the early part of last week, but wheat and barley cash bids were generally firmer into the weekend.

Sorghum harvest has started in Southern Queensland (QLD) and Northern New South Wales (NSW) around Moree. Northern NSW is forecast to see some storms late next week which could slow progress. Early yields in Southern QLD and Northern NSW have been favourable.

Australian Pulses Update:

Exports of Australian chickpeas, faba beans, and lentils are well advanced, as buoyant export demand and good quality enables a string of cargoes to set sail for South Asian and Middle East markets. Shipping figures and stems indicate more than 1 million metric tonnes (MMT) of the 1.9MMT chickpea crop, as forecast by ABARES, will have been exported from October to January, the first third of the marketing year. Around 300,000 tonne (MT) of current-crop lentils will have been shipped by the end of this month out of a total crop seen by ABARES at 1.1MMT crop. Faba beans is expected to see approximately 700,000MT exported by the end of March.

Export Stem & Ocean Freight Market Update:

There was 656 thousand metric tonne (KMT) of wheat put onto the stem in the past week which is the most in 18 weeks. Half of the wheat additions were in Western Australia (WA) but there was also 142KMT in NSW and 100KMT in South Australia.

There was also 172KMT of barley put onto the stem in the past week, split between SA and WA.

There was a further 73KMT of canola put on the stem as well.

Overall, wheat shipments are historically lagging while the barley and canola export pace is strong.

The Lunar New Year holiday is now in full swing with many Asian countries on leave this week. As the rates steadily declined over the past few weeks, it has caused market sentiment to be the lowest since the start of COVID – with freight rates to match. All sectors have been affected with many owners having to fix low freight or TC rates on the spot basis in order to find coverage with the hope that the market will improve once the Long Holidays are over. While this week we are not expecting any wholesale changes in the market, there is a general sense that rates are dragging along the floor and looking forward, there is still optimism that the market will bounce once the spot/prompt tonnage is cleared (which will take a couple of weeks). Helping this sentiment, there still appears to be a healthy amount of cargo enquiry currently in market, albeit at reduced levels. On a macro level, news of a ceasefire in Gaza was welcomed. If the truce is held, we will wait to see when the Red Sea is safe to transit again without the threat of a Houthi attack which would dramatically reduce the tonne/miles on many trades.

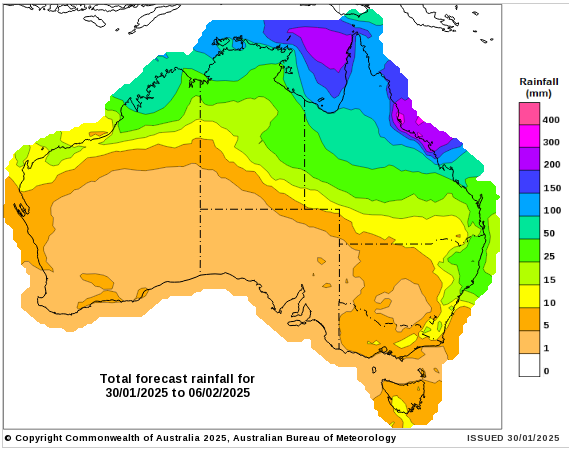

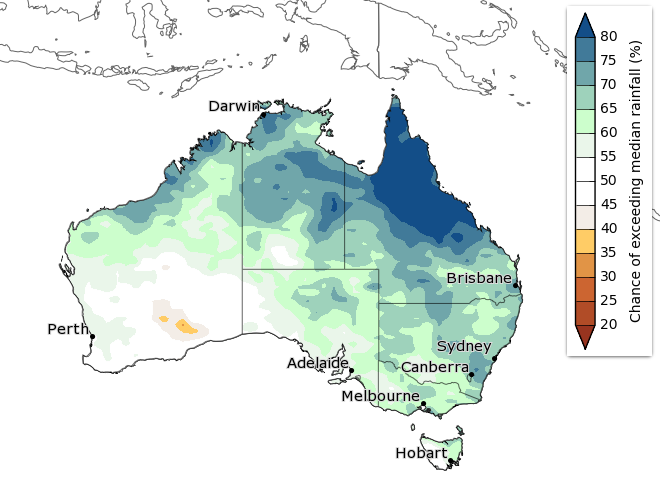

Australian Weather:

The 3-month long-range BOM forecast from Feb-Apr is indicating above median rainfall for most QLD, NSW, Victoria (VIC) and SA. This is welcome news for growers if it means a ‘normal’ break, particularly for VIC and SA. The forecast for the next week shows only coast rainfall with little pressure on the sorghum harvest for disruptions.

8 day forecast to 2nd February 2025

http://www.bom.gov.au/

Weekly rainfall to 29th January 2025

http://www.bom.gov.au/

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar was up 2% to finish last week when valued against the Greenback closing at 0.6300. The market traded with nervous optimism through the first week of Trump's second presidency as a more benign than expected policy agenda emerged. Heading into this week, the focus was on inflation rates. Q4 2024 CPI printed below consensus forecasts (as it has tended to do over the past two years), and importantly it also undershot the RBA’s projections. Headline inflation rose just 0.2% in Q4 with the annual rate running at 2.4%pa. As such, most banks now feel the RBA will announce a 25bp interest rate cut when it meets on 18 February. A 25bp move is now ~96% factored in. While the first step has been brought forward the outlook for the RBA’s cycle hasn’t materially changed. Interest rate markets are pricing in just over three cuts in 2025.

Most analysts believe further near-term downside should be limited. At the same time however, with US trade tariff risks still lurking and the USD firm, any near-term AUD rebounds are also likely to be capped. As per our 2025 outlook we see the AUD oscillating in the low- to mid-$0.60s over coming months as domestic and offshore cross-currents play out.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.