Australian Crop Update – Week 4, 2025

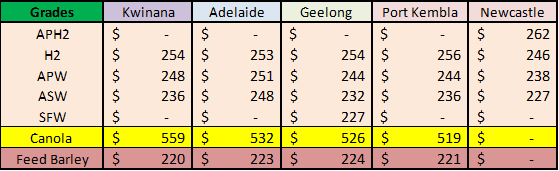

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Domestic wheat prices were firmer last week, barley was mostly steady, canola bids were lower with the declines in ICE and Matif. Global inputs were mixed. The AUD was up 1% for the week, now back at 62 cents. Overall, wheat basis remains soft with traders not willing to reward CBOT rallies while they are struggling with export competitiveness into Asia while the export pace is lagging. Feed grain markets across south east Australia edged higher in most key regions. However, the trade focus is now on the 2024/25 crop which is expected to result in another large sorghum harvest which will require another year of large exports, which will primarily go to China. Australia’s 2024/25 sorghum production is expected to top last year’s ABARES 2.2 million metric tonne (MMT).

Australia exported 579,589 metric tonnes (MT) of wheat in November 2024, according to the latest data from the Australian Bureau of Statistics. The figure is down 49 percent from the 1,126,926MT shipped in November 2023. Big pulse programs out of ports from Mackay in Queensland (QLD) to Newcastle in New South Wales (NSW), coupled with a drought-reduced crop out of South Australia (SA), contributed to the drop.

In containerised exports, Thailand on 32,691MT, followed by Malaysia on 24,161MT, and Vietnam on 23,886MT, were the biggest markets for shipments in November 2024.

In the bulk market, a total of 418,994MT was shipped for the month, with the Philippines on 96,198MT, followed by Indonesia on 83,481MT, and Japan on 58,349MT were the major destinations.

This week’s stem results reaffirm earlier observations of the advanced barley shipping pace compared to the lacklustre wheat program. Australia’s 2024/25 barley exports are 57% complete against our s&d forecast which is similar to last year in terms of the percentage complete of the forecast export program. Whereas the current Feb wheat exports are 18 percent behind last years. Hence, the only urgency in wheat buying is from some of the domestic delivered markets in south east Australia.

Exporters will be happy to let the farmer hold wheat supplies until export competitiveness improves.

On the demand side trader reports were circulating in Europe that Chinese buyers have cancelled an unspecified volume of Australian wheat purchases. It supports the overall narrative of disappointing Chinese grain imports this year. One to be watched.

Export Stem & Ocean Freight Market Update:

There was 292 thousand metric tonne (KMT) of wheat, 175KMT of barley and no canola put onto the shipping stem in the past week. There was also 185KMT of chick peas put on the stem, which was mostly QBT in Brisbane, catching up with some December loadings as well as forecast loading for Jan and Feb.

The dry bulk market continues to experience a challenging start to the year. Although expected, the extent of the downturn has caught many by surprise with rates plummeting lower than anyone predicted. There is a clear over supply of tonnage putting pressure across all sectors. This week we have seen an increase in smax/umax vessels fixing handysize business. Operators continue to be cautious in this difficult environment with a clear lack of confidence in the immediate future. With Chinese New Year (CNY) approaching, many are looking for the traditional rebound that follows these holidays. As in previous years, there is a sense of anticipation that post CNY there will be some much-needed stability and recovery in activity. However, until then there is very much a wait and see approach from most owners.

On a different subject, reports are emerging from Houthi sources that they may call a halt to rocket attacks now the peace agreement in Gaza seems to be holding. It may take a little while for owners and container lines to jump back in but sentiment, at least, does seem to be this will happen sooner rather than later. This should shorten delivery times with a resultant reduction in freight and container rates.

On the other side of the world, while water levels have recovered at the end of 2024 as El Nino subsided and La Nina emerged, the Panama Canal now faces heightened geopolitical tensions. Trump stated that he would not rule out military measures to regain control of the canal, citing concerns over Chinese influence on this strategic waterway. These developments further strain one of the main arteries of global trade.

Australian Weather:

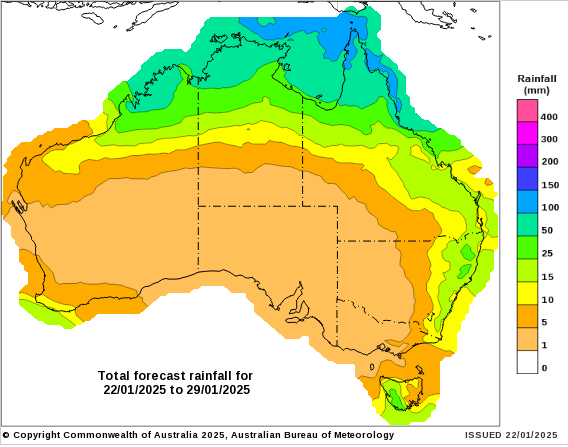

Scattered thunderstorms continued across the east coast over the weekend and through the week amounting to reasonable totals. There was 5-40mm across the Darling Downs and 10-30mm in Central QLD. Northern NSW recorded some storm activity 5-30mm. Central West NSW picked up heavier storms of 30-70mm which will build soil moisture for autumn winter crop plantings. The storms resulted in structural damage in parts of Southern NSW and the Central West. There were wind gusts of more than 100kmh with the Central West, Riverina, and Southern Slopes areas amongst the worst affected. Trees were toppled with damaged to buildings in areas from Griffith, Wagga and the Central West. The storms are benefiting sorghum crops although delaying early harvest in QLD.

8 day forecast to 29th January 2025

http://www.bom.gov.au/

Weekly rainfall to 21st January 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar was slightly firmer to finish last week when valued against the Greenback closing at 0.6190. The expectation is that the USD will ease and AUD/USD to strengthen this week as AUD looks oversold. However, the known unknown risk of US tariffs, specifically on China is a factor. Trumps tariff intentions are a big swing factor, and we are already seeing him put some of his pledges into action with a flurry of executive.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.