Basis Commodities – Australian Crop Update – Week 9, 2023

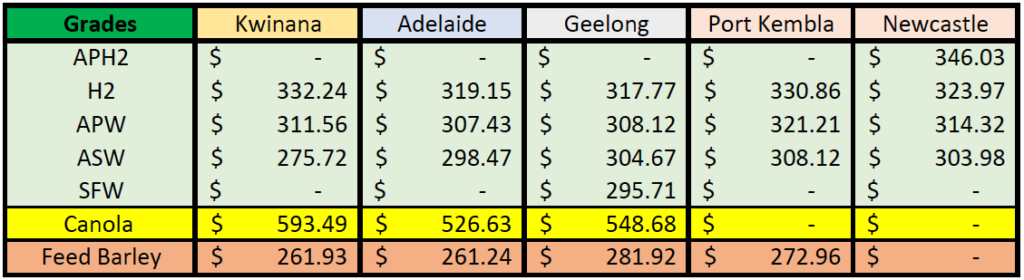

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Market Review

Domestic markets in Australia were generally firmer in the past week as buyers and traders do their best to purchase available farmer offers to cover off nearby export positions. It was another strong week for shipping stem additions within the port zones. Stem data shows that Australian exporters are finding ample international demand for all wheat, barley and canola. Grain exports are running at capacity in most zones.

Australia’s 2022/23 export pace moved into overdrive in December 2022 and shipping stem data indicates the brisk pace will continue through the first quarter of 2023. Australia’s combined monthly wheat, barley and canola exports in December was more than 4.6MMT. This comfortably exceeded the previous monthly major grains exports of 4.2MMT set in February 2022. Improved operations of the existing major grain export terminals as well as the addition of new participants have both contributed to the record large monthly grain exports.

ABARES will updates its Australian crop forecasts in early March, and this will be reflective of the bigger crop on the back of the larger than expected grain receivals in Western Australia and South Australia. We expect they will end up lifting the wheat crop to 38MMT plus and barley to 13.5MMT plus.

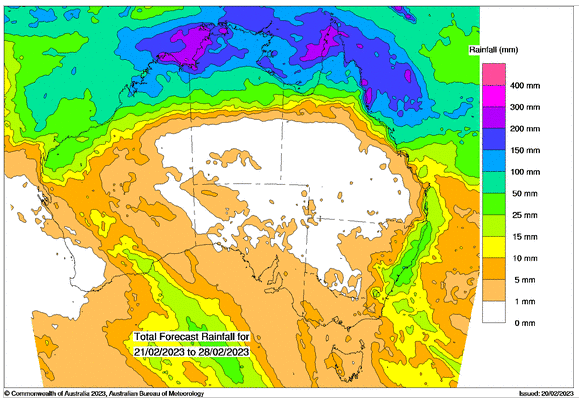

Australian Weather

The Australian Bureau of Meteorology said in its latest Climate Drivers Update, La Niña continues in the tropical Pacific Ocean. While oceanic indicators, including sea surface temperatures (SSTs), have weakened to ENSO-neutral values, the atmosphere has been slower to respond and remains La Niña-like. Most of the major models show an increased risk of an El Niño developing in late 2023.

Major models are pointing to drier weather in the coming months. The European 46-day has weather patterns over Australia becoming drier in the coming months as the La Niña influences decay and influences move closer to El Niño. El Niño is predicted to commence in May.

Source: http://www.bom.gov.au/

Source: http://www.bom.gov.au/

Ocean Freight

We are seeing positive rates (albeit in small increments) being reported on Supramax and handy indices but can’t see why those particular sizes have improved versus Panamax which has remained subdued. There doesn’t seem to be any significant movement in fundamentals and the general “feel” of the market is still quiet. The Indo-coal shipments have picked up and there is plenty of China controlled tonnage being pushed around the market. The implication is the domestic China freight markets remain unhealthy which should pull the rug from under the market optimists. March and April FFA levels being reported by brokers are at significant premiums to spot physical….BSI 10tc is $7,641 spot physical versus xs $11k for March and nearly $12.5kpd for April. Something significant has to happen soon for these levels to justify themselves. PMX physical spot levels have been steady to slightly negative. Nothing new has happened over the last week and consequently, the index drifted off.

AUD – Australian Dollar

The Australian dollar finished the week on a lower note at .6827 against the Greenback after hitting a high of 0.6998 on Wednesday last week. The AUD/USD pair remains under heavy selling pressure driven by the China / Australia relationship remaining tenuous due to historical grievances and a lack of cooperation between the two governments. It is expected that the USD can track higher this week given the recent bout of positive US economic surprises. Eventually, US economic outperformance will fade as it shows more strain from the interest rate rises.

The post Basis Commodities – Australian Crop Update – Week 9, 2023 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.