Basis Commodities – Australian Crop Update – Week 46 2022

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Mostly dry and warmer weather in the coming days is conducive to harvest activity this week. Queensland and Northern NSW will see warm weather before storms arrive on the weekend. Southern areas across eastern Australia are also set for warmer temperatures on Thursday and Friday as well as a generally dry forecast through to the start of December. The delayed start to harvest on the east coast is expected to see a more drawn out harvest in Victoria, and cool and unsettled weather continues to limit harvest progress this week in South Australia. Western Australia’s growing areas received some rains which slowed their rate of harvest progress.

Early wheat quality isn’t offering any major surprises. Proteins are below average with the high yields. High protein grades are scarce and there is plenty of downgraded wheat coming to the market in Queensland and Northern New South Wales. The proportion of the downgraded wheat is expected to climb when the NSW harvest eventually picks up, but there does seem to be a pleasing amount of milling wheat out there. There is some AH 11.5 protein coming off, but very little APH.

Logistics continue to be a challenge as many roads in the North West of NSW remain blocked due to floods. Last week GrainCorp’s total NSW grain deliveries finished at 0.39MMT which is about 2MMT less than the same time last year.

CBH received 1.4MMT of grain taking total deliveries to 3.9MMT, compared to a total of 4.7MMT this time last year. Growers are still reporting yields higher than expected in Western Australia and protein in the Northern part of the state is also higher than expected at this stage. Wheat proteins have been lower as harvest moves south. The Geraldton zone has received nearly 1.5MMT of grain deliveries which will be about a third of what is expected. Overall, WA harvest is nearing 20% complete.

Grain deliveries in SA picked up last week. Viterra reported around 340,000 tonnes of grain delivered into its storage network in the week ending November 13, taking the season total to around 370,000 tonnes. Just under three-quarters of the grain deliveries were on the Eyre Peninsula, where hot, dry weather is allowing farmers to make good progress.

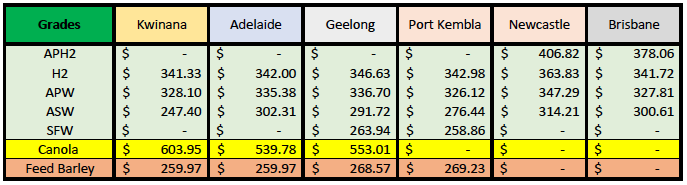

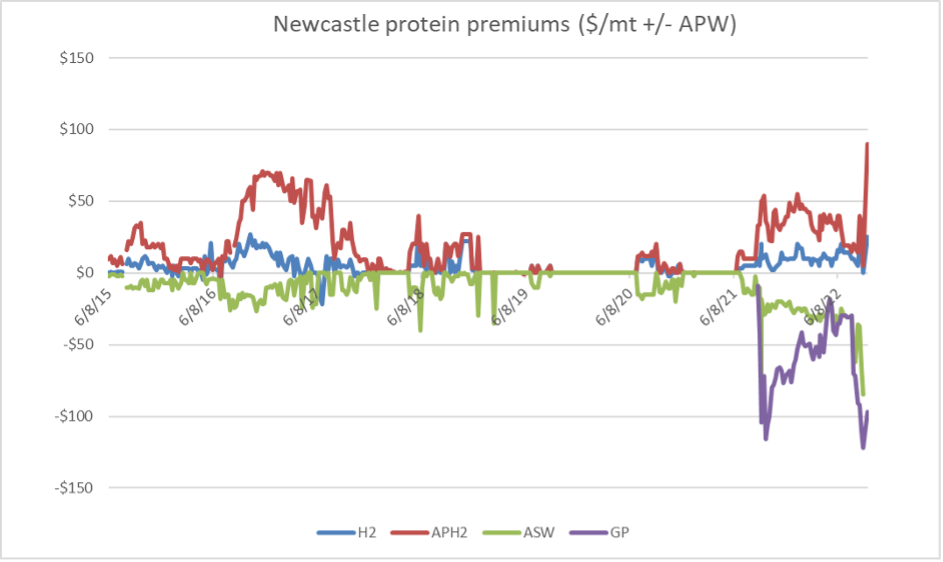

Domestics cash markets were broadly pulled lower by harvest progress, strength in the dollar and weakness in global markets with the extension of the Ukraine safe corridor deal. This is very variable by region and most of the work is being done on the quality spreads with lower quality wheat moving lower and protein wheat – APW and AH2 and higher – maintaining value. Indeed, if you look at this graph below from our analysts you can see graphically how the protein spreads are widening at the track level in AUD – albeit in the Newcastle zone.

Canola bids were sharply lower across all zones with the sharp declines in overseas markets. Barley bids were down $10/MT but the trades through Clear Grain Exchange suggest the feed barley bids are even softer than the $340/MT quoted for Kwinana. On the futures side, ASX wheat futures were down $15/MT to $450/MT and are now off about $40/MT in the past couple of weeks.

On the demand side of the equation, there is growing speculation among the trade that China will lift bans on Australian barley and canola imports after a meeting between leaders on the sidelines of the G20 meeting. Indeed, Chinese buyers continue to be active in the wheat space and are reported to be buying milling wheat into Q2 of 2023 from Australia. Nothing has been confirmed, but it looks like traders are sensing change and Chinese demand may have already emerged.

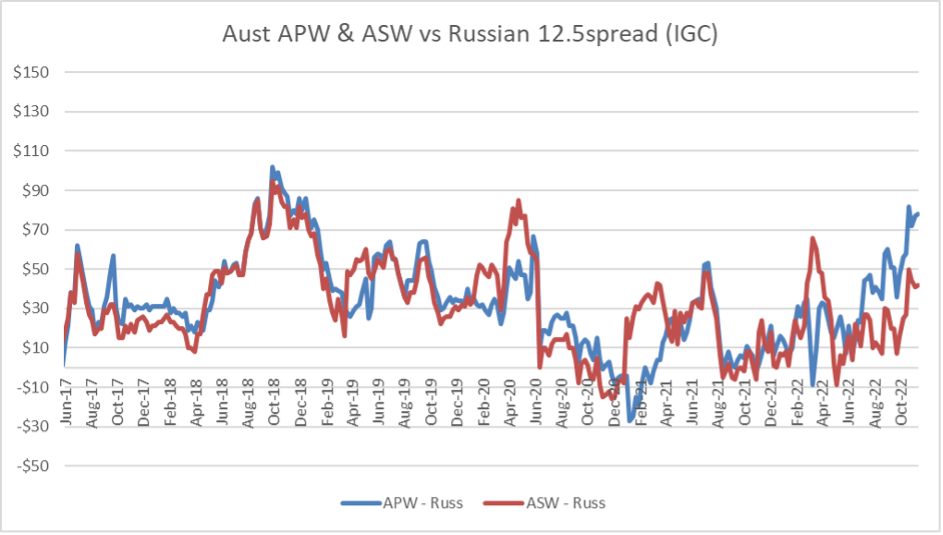

In the Middle East and East Africa, demand remains muted. APW and ASW, as this graph shows, are still pricing healthy premiums over Russian 11.5 and 12.5 wheat into those markets which is making finding demand difficult.

Ocean Freight & Export Stem

Southeast Asian demand seems to have bottomed out – especially for Handysize vessels – but the Far East remains over-supplied and the amount of China cargo is limited. As we mentioned last week, until we see more cargoes into China from charterers, the signals for the Ocean freight market will remain negative. Bunkers continue to slowly slide away which assists with voyage numbers.

Export Stem additions continue to climb with the onset of the 2022/23 harvest, although it’s not without its problems. There was close to 1.2MMT of grain added to the stem in the past week up from about 1.0MMT in the previous week. Two-thirds of the weekly stem additions were WA/SA with exporters still very unsure about the ability to export from the east coast, particularly NSW which is the worst affected state by weather and floods.

Australian Dollar

In a quiet week for the markets given the US Thanksgiving holiday later this week, the Aussie was trading a bit under 66½¢ to the USD earlier this morning.

The post Basis Commodities – Australian Crop Update – Week 46 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.