Basis Commodities – Australian Crop Update – Week 33 2022

Market Update

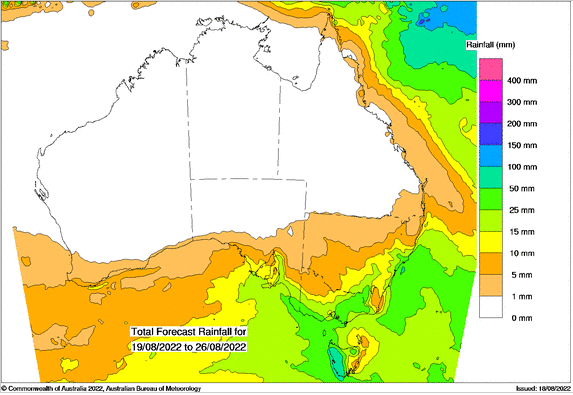

The BOM (Australian Bureau of Meteorology) ENSO Outlook has been raised to La Niña ALERT. Historically, when La Niña ALERT criteria have been met, La Niña has subsequently developed around 70% of the time. La Niña events increase the chances of above-average rainfall for northern and eastern Australia during spring and summer. In addition, the Indian Ocean Dipole (IOD) index has been very close to or within negative IOD thresholds since early June, with the latest weekly value one of the strongest observed so far during this event. All surveyed climate models indicate that negative IOD conditions are likely to continue into late spring. A negative IOD event is typically associated with above average winter–spring rainfall for much of Australia, so in short, the fear is we are in for a similar year of wet conditions in the run into 22/23 Harvest with all the challenges that brings.

Indeed, too much rain is the concern for most of NSW. That said, last week’s rain across the state was heaviest in the north where crops will benefit from the rain and lighter across the central west where they have been struggling with the excess moisture. The northwest received 20-30mm in the past week while falls across the central west were mostly limited to 5-10mm. The north and the south of the crop are positioned for above average yields but production in the central west will be constrained by the excess moisture.

Australia’s other cropping regions are well positioned heading into spring with regular rainfall helping to lock in another massive winter crop. To that end GIWA (WA growers) updated its crop estimates on Friday and said the state’s total grain harvest has the potential to climb above 20MMT for a second consecutive season following the recent rain. They put the WA total grain harvest at 19.6MMT vs 24.0MMT. They pegged the 2022 wheat crop at 10.3MMT (12.9MMT LY), barley at 5.1MMT (6.37MMT LY) and canola at 3.16MMT (3.13MMT LY).

In discussion with FOB sellers, it feels like old crop export sales are largely in the execution phase with logistics and scheduled maintenance shutdowns severely limiting FOB liquidity. Similarly, concerns about new crop protein and weather risk are also limiting new crop appetite after the initial rush to fill Chinese new crop demand.

Barley was softer in both the old and the new crop. The issue for barley is one of demand. Aussie barley will be priced to find export demand in the new crop, but will this demand be enough to shift the crop without China and as Saudi’s imports shrink? Exporters will be cautious about building length, and this is evident in the grower bids for new crop.

Australia exported 2.798MMT of wheat in June, up from 2.366MMT in May. WA shipped 920KMT, the most since Feb while NSW shipped 736KMT. China was the largest destination taking a massive 711KMT followed by Indonesia with 318KMT, then Vietnam with 225KMT and then the Philippines with 200KMT. Australia has exported 20.8MMT of wheat so far for Oct/Jun. Barley exports for June were 563KMT down from 681KMT in May and 758KMT in April. Saudi took 293KMT, Japan 158KMT and then Vietnam with 68KMT. Australia’s Oct/Jun barley exports are 6.4MMT. Sorghum exports were 273KMT which is about the same as May. China took 196KMT and then Japan with 69KMT. Canola exports were 481KMT. Australia has shipped 4.72MMT of canola in the Oct/Jun.

There was 323KMT of wheat added to the stem in the past week. There was no wheat added in WA in the past week. Vic accounted for 123KMT of the weekly wheat additions followed by 80KMT in NSW, then 65KMT in Qld and 55KMT in SA. Sorghum was the next largest grain with 135KMT which was split between NSW & Qld.

Ocean Freight

It feels like last week the market over-corrected to the downside - if that is a thing. Certainly, the feeling this week is more positive but it feels notional and until owners and charterers come off the fence, the market maintains a status quo of sorts albeit at lower levels.

Australian S & D Update (Agscienta)

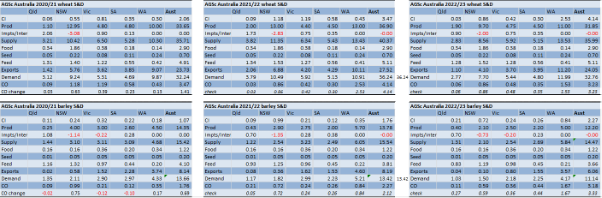

Our Analysts Agscienta released changes to our forecasts for Australia’s wheat, barley, and canola balance sheets this week. There were multiple changes.

Firstly the 2020/21 wheat, barley and canola production estimates have been adjusted following the release of the ABS 2020/21 survey data a few weeks back. Changes to the 2021/22 balance sheets are limited to export progress. I am using national 2021/22 wheat exports at 27.5MMT, barley export at 8.2MMT and canola exports of 5.5MMT. The barley exports are below USDA’s 9.0MMT which looked optimistic from the start. This leaves wheat carry over stocks at 4.1MMT, barley at 2.3MMT and canola at 0.6MMT. The most notable feature of the carryover stocks is that wheat and barley stocks in WA are building on the back of last year’s massive crop. WA has 2.5MMT of the 4.1MMT national wheat stocks and 0.8MMT of the 2.3MMT national barley ending stocks at Oct 1. This isn’t because of a tardy WA export pace which has been up and about 1.6MMT/month, but more a function of the size of the crop.

We have raised 22/23 national wheat production to 32.0MMT from 30MMT previously. A low 30’s crop is justified, and it could climb to a 34 and possibly 35MMT. A national crop of 32MMT equates to a national wheat yield of close to 2.5 t/ha. Extended weather models point to a cool mild finish. WA crop conditions are extremely good and will continue to improve heading into September following recent widespread rain. SA’s Eyre Peninsula is the best since 2016. Other parts of SA are improving following a late start with recent rains. Vic is the best in more than a decade. NSW is mixed. The south is very good, Central areas are late and too wet but are starting to improve.

We are pegging the national barley crop at 12.2MMT. This is down from the past couple of years but still large by historical standards. Domestic feeding and malt will be maximised, but it still leaves a large export surplus of about 7MMT to keeping ending stocks close to unchanged. This will be a challenge without China/slowing Saudi imports and stiff export competition from cheaper corn, but the bearishness of the barley situation needs to be offset against slot availability as different commodities vie for place on the stem.

We have lifted the 2022/23 canola crop to 6.1MMT. This is down from 6.8MMT in 2021/22 but still a massive crop. We are using exports of 4.5MMT which is the same as the USDA and this leaves a stock build of 300KMT to 0.8MMT. We are using a crush of 0.9MMT. Some have raised the national crush to about 1.0MMT. Either way, stocks are building.

The post Basis Commodities – Australian Crop Update – Week 33 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.