Basis Commodities – Australian Crop Update – Week 24 2022

Market Update

Cash bids remain variable across the various export zones, but it was evident that traders are stepping up efforts to shake out remaining old crop longs. Traders reported improved liquidity throughout the week. Barley bids were generally softer across the east coast which is likely to reflect that farmers are selling more barley than wheat ahead of the end of financial year.

ABARES released its first detailed 2022/23 crop estimates earlier in the week. Their forecasts indicated soaring grain prices and mostly favourable planting conditions are expected to result in a third consecutive bumper winter crop. In its initial estimates for the 2022/23 season, ABARES said Australia is forecast to produce 30.2MMT of wheat. Barley production is forecast at 10.9MMT with canola projected at 5.6MMT. Other forecasters are saying the wheat crop will be larger. However, as mentioned last week, early cautionary flags have emerged in multiple states which highlight the 30MMT national wheat crop is far from guaranteed. South Australian farmers have welcomed recent soaking rains but a late start means above-average yields will depend on good winter rains and a soft spring. It is still excessively wet in Southern Queensland and Central West New South Wales and this is hampering winter crop planting in these areas. The areas most affected in New South Wales account for 60% of the state’s wheat area (Northern, North West and Central West). A lot of this is already planted, but a significant proportion isn’t. Some of these areas are only partially planted. Dry weather is a building concern in Western Australia.

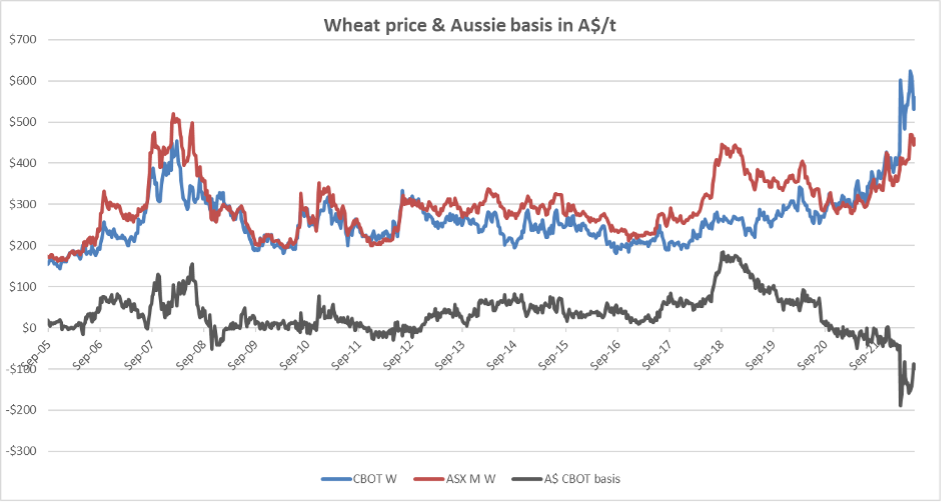

The mix of high grain prices and historically cheap Australian basis leaves a volatile and dangerous mix for domestic markets in the coming months. Global markets are set to remain strong, even if a deal is reached to allow grain exports from Ukraine. New crop basis is historically cheap at A$-90/MT. We have included a long-term basis chart with ASX, CBOT and basis all in A$ terms.

USDA Report Summary

The USDA’s June WASDE report failed to offer many fresh inputs. In the United States, the USDA trimmed HRW wheat production, but this was offset by a larger SRW crop. They didn’t change the HRS forecasts. Some private forecasters have lowered forecast US wheat plantings by more than 1.0 million acres on the back of the late plantings. This equated to upwards of 1MMT of lost production based on average yields. It’s also likely that some of the intended spring wheat acres in the Canadian Prairies (Manitoba) may not be seeded because of wet weather delays. This will leave the North American high protein balance sheet extremely tight for the 2022/23 season with no room for further weather problems. Russian wheat production was increased by 1MMT to 81MMT and exports were raised by 1MMT to 40MMT. Other private forecasters are calling the Russian crop 5-6MMT higher. India’s wheat crop was lowered by 2.5MMT to 106MMT and exports were cut by 2MMT to 6.5MMT. World wheat trade was trimmed by 0.3MMT to 204.6MMT. We expect this will prove too high when the extent of demand rationing can be better assessed in the coming months as importers pare back purchases at the current high prices. The bottom line of the above changes is the world is still heavily reliant on exports from the EU and Russia. Russian exports of 40MMT will depend on commercial shipping companies gaining guaranteed safe access to the Black Sea shipping routes. This is not guaranteed. Ukraine’s wheat production was unchanged at 21.5MMT with exports of 10MMT. Global weather risks remain. Dry weather is restricting wheat plantings in Argentina which has private forecasters lowering production estimates.

The USDA’s June WASDE didn’t offer many fresh inputs for corn. USDA cut the US 2021/22 corn exports by 50 million bushels on the sluggish shipping pace which lifted the carryover stocks. New crop US plantings and production were unchanged. Plantings could fall by 1 million acres with the slow progress in North Dakota and Minnesota, but USDA is waiting for the June seeding report for further inputs. The US 2022/23 balance sheet will be driven by final planted area, yields and strong domestic biofuel margins. The US 2022/23 ending stocks were lifted to 1.4 billion bushels on the large 2021/22 carry in stocks. Globally, USDA raised Ukraine corn production, but can it be exported? There is limited downside to corn with the strong domestic premiums and threatening weather as well as questions around yield assumptions.

USDA lowered its forecast for world 2022/23 barley production by 1.7MMT on smaller crops in the EU, Australia, and Ukraine. Saudi’s 2021/22 imports were cut and the 2022/23 were pulled back by 0.5MMT to 5.0MMT. China imports were unchanged at 10MMT. As with wheat, soaring prices are likely to erode global demand for barley. This is already evident in Saudi Arabia.

The June WASDE report was bullish soybeans, with the USDA raising old crop exports and lowering 2021/22 ending stocks to just 205 million bushels. Old crop stocks are tight, domestic processing margins are high, export demand is robust, and the US weather threatening. Markets will remain extremely sensitive to the slightest of weather concerns in all the US summer crops, but particularly soybeans. Global soybean supplies are relatively tighter than corn because of the changes in the Brazilian supplies. Demand rationing is the next step as there are no global buffer stocks for soybeans.

Currency

The Aussie Dollar rallied sharply overnight with the US Federal Reserve raising interest rates by an aggressive 0.75%. The drivers were a stronger message on interest rates from the RBA and some stronger‑than‑expected economic date from China. The Aussie is suffering more than most because China’s economy remains at risk of further COVID lockdowns.

The post Basis Commodities – Australian Crop Update – Week 24 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.