Basis Commodities – Australian Crop Update – Week 20 2022

Market Update

The last week saw rain across much of the country. Western and South Australian farmers will welcome the rain as planting continues but many farmers in the east will be hoping for a gap in the rain as it is now so wet, planting is being held up. That said, east coast plantings are already advanced. Most of the canola is already in the ground. Some areas may end up getting replanted to wheat or barley as it’s been too wet.

Looking forward, the Bureau of Meteorology said June to August rainfall is very likely to be above median for much of mainland Australia. The chance of exceeding the median is greater than 80% across most of northern Australia, southern Queensland, New South Wales, north-western Victoria, and the north-eastern half of South Australia. Large parts of eastern Australia have a 40% to 60% chance of being in the wettest 20% of past June to August periods. This is around two to three times the normal likelihood of a very wet season. There is an elevated chance of below-median winter rainfall for parts of Western Australia’s Southwest.

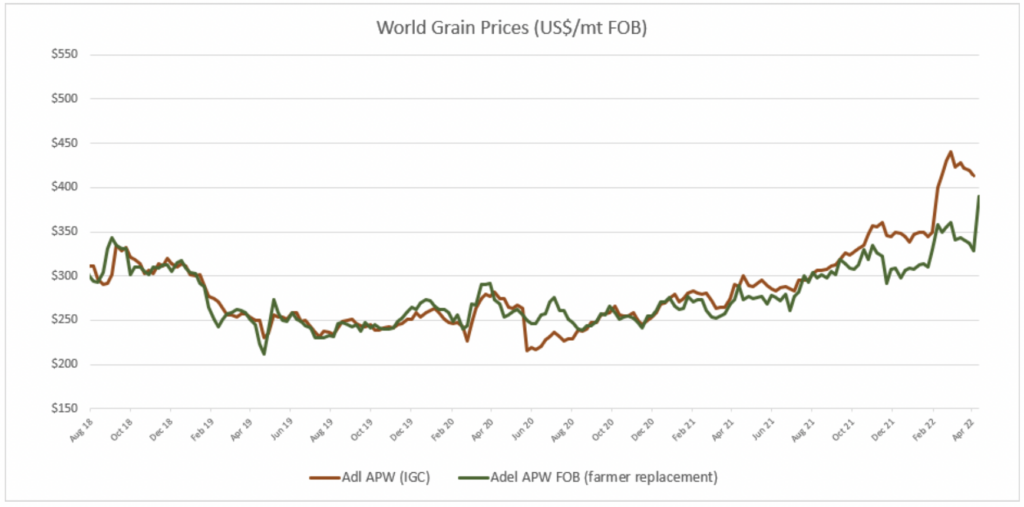

The cash markets were sharply higher this week on the bullish global news and some domestic market shorts being squeezed. Grains are very difficult to buy. At this stage, it feels like Australia will continue to find both export and domestic demand and therefore we feel it is likely values will remain firm into new crop. Wheat is just one of a number of commodities that will be pushing for space on the export elevators this year so our expectation is there will be little or no inverse to new crop this year at the FOB point. Indeed, new crop (2022/23) bids were steady to higher in all zones.

High prices have many domestic demand sectors assessing if they can ration back grain demand. This is only possible for a few; others will be assessing how they can pass the prices back on. We expect that feedlot numbers will decline as there is plenty of natural fodder. Overall, the capacity to pare back domestic grain usage is limited as most of the industries are domestically focused.

On the International demand side, many consumers are seemingly trying to reconcile local commercial realities with current values and certainly, the issue of demand destruction has at some point got to impact FOB values. Although, there seems little evidence of it to date.

As time progresses and the Russia/Ukraine war continues, the impact of limited Black Sea exports only becomes more acute as French and Hard Red Winter crops struggle with dry weather. Weather remains too wet across the US Northern Plains which is likely to result in less spring wheat and corn plantings for North Dakota and Minnesota.

Add to this India’s seismic decision to ban bulk exports on Friday night – albeit with caveats – and it feels like we are witnessing the emergence of a wheat balance sheet issue, the likes of which many of us have never witnessed.

Interestingly, the USDA touched on this issue in its latest report. Globally, world wheat production is forecast to fall by 4.5MMT to 774.8MMT. World wheat stocks are set to fall by 12.7MMT to 267MMT which is the smallest since 2016/17, although global trade has grown by 20MMT since then. Pardon the pun, but that is food for thought…

Ocean Freight

A month of holidays across the globe starting from Easter and finishing with Golden week in Japan and May Holidays has certainly been disruptive, but fundamentally we remain in the same spot we were two months ago. The freight market is jittery and seeking clear direction and it’s hard to pick out the true drivers from the myriad of factors that are potentially in play. Not the least of these is that China remains beset by COVID which is causing congestion. This should be tightening tonnage supply in the Pacific, but it has been matched by an absence of orders to really tilt the tonnage balance in the owner’s favour.

The Atlantic has generally firmed – rates ex US Gulf/East Coast South America have seen most improvement and we would say the Atlantic has now re-gained its freight pre-eminence over the Pacific…but it has not caused a traditional “back-haul” rate structure to re-emerge which helps importers in the Middle East and East Africa. Fuel prices remain stubbornly high, and it doesn’t appear there will be any relief in the near future as oil prices remain supported by supply issues that seemingly outweigh the drag being seen in reduced demand.

USDA Commentary

The USDA US Hard Red Winter Wheat production was cut by nearly 6MMT and world wheat production was lowered some 3.6MMT to 774.8MMT whilst consumption was forecast at 787.5MMT. Russian exports were posted at 39MMT and Ukraine at 10MMT, and whilst the world needs these volumes, it seems difficult to see how either can achieve these numbers. Indian production was posted at 108.5MMT (the Government last was 105MMT and the trade is around 95MMT) but most importantly exports for 2021/22 were pegged at 8.2MMT which today would be around 6MMT and for 2022/23 were set at 8.5MMT which basis the export ban, will be close to zero.

The market was surprised USDA cut its estimate for U.S. corn yields to 177 bushels per acre, down 4 bushels from February. Spot corn ended modestly higher with stronger gains in the new crop December.

Soybean futures closed higher on expectations for limited U.S. supplies. USDA said U.S. farmers will harvest a record large soybean crop for the second year in a row this year, but supplies will remain tight due to soaring demand.

World barley production for 2022/23 is forecast at 149MMT up from 145MMT in 2021/22. There are some big changes in the annual changes at the country level. Canada’s crop is up by 3.55MMT to 10.5MMT following last year’s drought.

Australian Dollar

The Australian dollar fell to new year-to-date lows as markets maintained a firm risk-off mood. Fears the global economy is poised to tip into recession, as the sustained conflict in Ukraine heaps pressure on Europe’s energy crisis, China’s COVID-zero policy hampers supply chain productivity and central banks begin aggressively hiking interest rates, all weigh on investors, prompting an evaporation of positive sentiment. The AUD plunged below supports at 0.6915/20 to mark fresh intraday lows at 0.6830. Equity markets plunged, while copper, iron and other key metal exports all tested new lows. Often seen as a barometer for global growth, copper prices plunged nearly 3% while iron ore futures were down over 4%. Fresh fears Beijing will soon be plunged into lockdown sparked concern supply chain disruptions will only worsen in the months ahead.

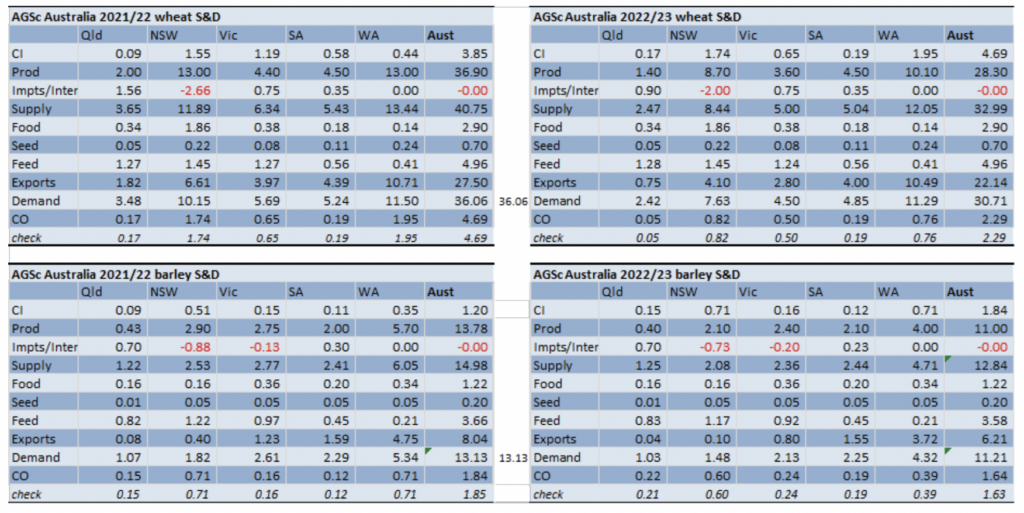

Agsicenta latest Australian Balance Sheets

The post Basis Commodities – Australian Crop Update – Week 20 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.