Basis Commodities – Australian Crop Update – Week 15, 2023

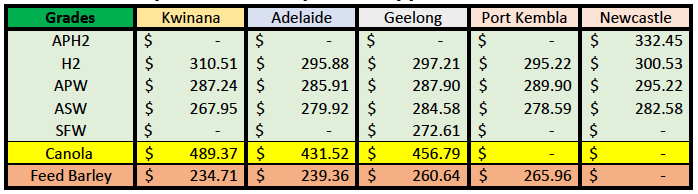

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains & Oil Seed Market

Australian markets were softer last week for wheat, barley and canola with further declines in global values. The size of the price declines varied by port zone on the nearby coverage. This is primarily against export positions with the domestic buyers mostly covered against nearby requirements. Barley bids were steady for the week, but the offers have disappeared on reports that China’s ban on Australian imports may be coming to an end. It’s clear that Beijing and Canberra have been discussing details about a possible end to the barley export ban and the decision earlier this week to halt WTO actions and allow the Chinese government to review the situation on Australian Barley imports was seen as a face-saving exercise in light of WTO likely to rule in Australia’s favour. Relations between China and Australia have thawed considerably over the past six months.

The Australian Bureau of Statistics confirmed another impressive export month for February. This included a further 3.0MMT of wheat exports. Barley exports were strong at 1.04MMT and the strong canola shipments continue with a further 600KMT for Feb. Pulse crop exports were also strong. Combined wheat, barley and canola exports were 4.6MMt, slightly up on the 4.4MMT in Jan and Dec. Western Australia’s combined wheat, barley and canola exports exceeded 2.0MMT and weren’t far below the December record.

Wheat exports from all states were strong with China being the largest destination with 646 KMT. This lifts their Oct/Feb tally to 3.25MMT. Vietnam was the next largest with 374KMT then Thailand with 326KMT, South Korea with 255KMT, Indo with 231KMT and then the Philippines with 194KMT. The breakdown of the wheat export destinations highlights that Australia’s wheat export sales have become more difficult after the recent sharp declines in US corn values given that a lot of the wheat exports have been heading into feed grain destinations in Southeast Asia.

Saudi was the largest barley destination with 277KMT, lifting the Oct/Feb total to 1.2MMT. Japan was next with 150KMT and then Thailand with 130KMT.

Looking forward, Australian wheat plantings are set for a strong start as better-than-expected rains in central and southern areas have further improved soil moisture in the wheat growing areas with more on the way as this 14 day forecast shows.

On the other hand the Australian Bureau of Meteorology says from July, all but one of the models indicate El Niño thresholds will be met or exceeded, with all models noting it will be established by August.The ENSO is currently neutral with most international climate models suggesting neutral ENSO conditions are most likely to persist through autumn. It should be said ENSO outlooks extending beyond autumn should be viewed with some caution as they typically have lower forecast accuracy than forecasts made during other times of the year. When ENSO is neutral, the Pacific Ocean typically exerts little influence on Australian climate patterns. El Niño typically suppresses rainfall in eastern Australia during the winter and spring months. The Indian Ocean Diapole (IOD) is neutral. Most models suggest that a positive IOD event may develop in the coming months. A positive IOD can supress winter and spring rainfall over much of Australia, potentially exacerbating the drying effect of El Niño. Long-range forecasts of IOD made in autumn have lower accuracy than those made at other times of the year.

Ocean Freight Market & Export Stem

With holidays world-wide last week, the freight market headed lower as cargo activity dried up. Many players were away from the market, so liquidity tightened and rates fell away for the nearby positions. Owners across all sizes with tonnage open ppt-10days forward all took a bath as they realised enquiry was likely to dry up over the holiday period. Coal into China was notably quiet and there wasn’t much else to take its place. Supramax – Ultramax took the brunt of the fall with rates in Southeast Asia dropping away quickly to low teens and Charterers bidding sub $10kpd by the end of the week. It would not be a surprise to see rates already under $10k for Supramax types in the Pacific as we emerge from Easter. Handysize and Panamax held steady but sub-index types are under pressure – not a good sign. Several of the operators were expecting this dip to be short-lived, with activity picking up again after 1-2 weeks and FFA levels would indicate some support for that hypothesis but really the only thing predictable about the current market is its unpredictability. Owners are still holding firm on period numbers so a large discrepancy exists again between trips and legs for operators to try and bridge.

It was a quieter week for the Australian shipping stem following the sizable wheat additions in the previous week. A further 450KMT of wheat and 115KMT of barley was added to the stem in the week leading up to the Easter long weekend with no further canola.

Pulses Market Update

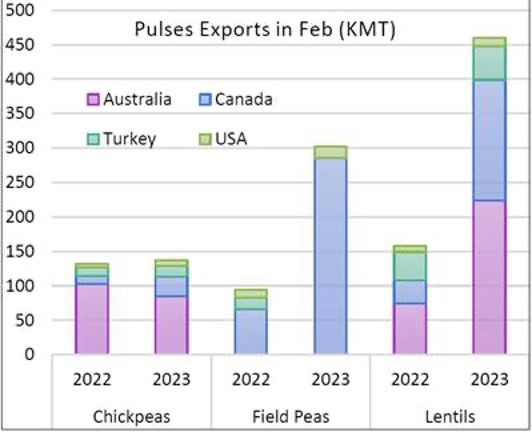

Availability of pulses remains higher than last year. As per the custom data available, lentil exports out of the four top exporters (AU, CA, TR, US) were 460KMT, compared to 158KMT last year. While India, the top importer, remained absent from Canadian shipments, Australia sent 122,504MT of lentils. For field peas, Canada exported 285KMT vs only 66KMT last year. Chickpea availability has also improved from the same time last year.

Ukraine to Plant Less Peas? As per the Ministry of Agriculture data, Ukrainian farmers have completed pea planting on 73,100 ha, compared to 82,500 ha at the same time last year. Pea acreage is falling behind and the ideal window is closing soon. The weather is conducive for the growth with sporadic rains and ample soil moisture.

Australian Weather

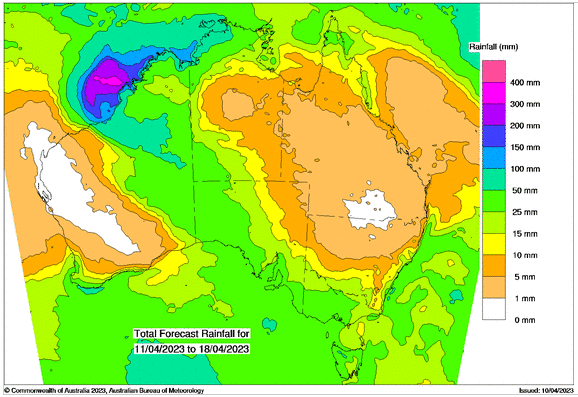

More rain fell across Australia’s cropping areas last week with Western Australia benefiting the most. Victorian cropping areas also saw decent falls throughout the week as did New South Wales. Queensland saw some patchy rain, but we expect this was isolated as some stations saw little to no rain. There were some heavy storms across the inner and eastern parts of Southern Queensland. In general, Australian farmers are happy with the start to the 2023 cropping season following the rains over the past few weeks. However, all eyes are on the medium-term weather outlooks and the prospects of an El Nino developing in the coming months as mentioned earlier.

Source: http://www.bom.gov.au/

Source: http://www.bom.gov.au/

AUD – Australian Dollar

The Australian dollar slipped back below US$0.6650 over the Easter break, weighed down by a slew of US data sets. US treasury yields rose on Friday, buoyed by another strong US non-farm payroll print. Payrolls climbed more than 230,000 in March, in line with market expectations lifting yields and dragging the USD higher. Having tested a break above US$0.67, the AUD slumped back below this handle, compounding losses through trade on Monday to mark weekend lows below US$0.6620. With another Fed rate hike all but priced in, we expect the AUD to remain under pressure through the near term. While supported on moves below US$0.66, upside moves will likely meet resistance above US$0.6750 and approach US$0.68.

USDA Report

The USDA’s April WASDE report offered few surprises which was US corn and wheat closing lower while soybeans strengthened. USDA kept its US 2022/23 corn and soybean ending stocks unchanged and modestly increased US wheat ending stocks. Analysts generally expected the USDA to trim corn and soybean stocks slightly after the March quarterly stocks report showed smaller than expected supplies. USDA left the US 2022/23 corn ending stocks at 1,342 mill bu and soybean ending stocks at 210 mill bu. US wheat ending stocks were increased by 30 mill bu to 598 mill bu, still down 100 mill bu (2.7MMT) on last year. Globally, USDA made further sizable cuts to Argentina’s summer crops. Although this came as no surprise. The most notable was a change in the global export mix. USDA lowered its forecast of 2022/23 world wheat exports by 1.2MMT to 212.7MMT. However Russian wheat exports were raised by 1.5MMT to 45.0MMT, Ukraine exports were increased by 1MMT to 14.5MMT and EU exports were cut by 2MMT to 35MMT. The safe corridor is working effectively for now and global buyers want cheaper Black Sea wheat supplies however a vocal minority in Eastern Europe is tired of the cheap flow entering from Ukraine angering their respective farm communities. Australia’s wheat exports were unchanged at 28.5MMT, up 1MMT on last year. World barley trade was trimmed by 0.3MMT to 30MMT, down 2.4MMT from 2021/22. Saudi Arabia’s imports were reduced by 0.4MMT to 4.3MMT.

The post Basis Commodities – Australian Crop Update – Week 15, 2023 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.