Basis Commodities – Australian Crop Update – Week 10, 2023

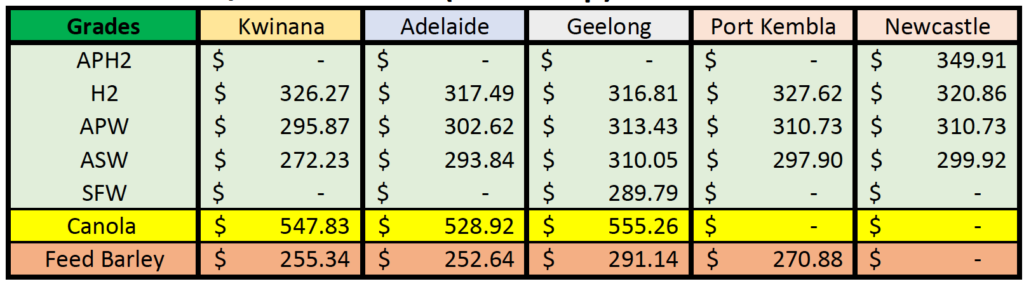

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Market Review

Big crops get bigger, and this has certainly been the case with Australia’s 2022/23 winter crop. The crop production forecasts across the board are higher following the harvest receival data showing Australia’s 2022/23 national wheat crop at 38.55MMT, the barley crop at 13.75MMT and canola at 7.8MMT. It’s a record large winter crop harvest, comfortably exceeding last year’s harvest. This was achieved with the massive crops in WA and SA, as well as big crops in Vic and Qld. These offset the smaller harvest in NSW where the excessive wet resulted in a lot of crops not being harvested along with eroding yields.

The Australian markets moving forward will be a function of exports, shorts and the prospects of a drier season in 2023/24. Australian grain prices have ignored most of the selloff seen in the US and French markets over the past week or so. Traders and exporters have absorbed most of the price decline.

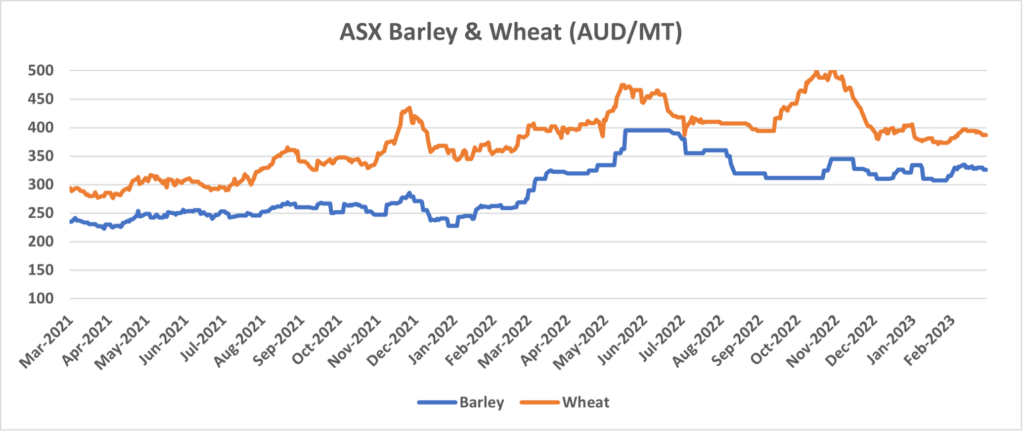

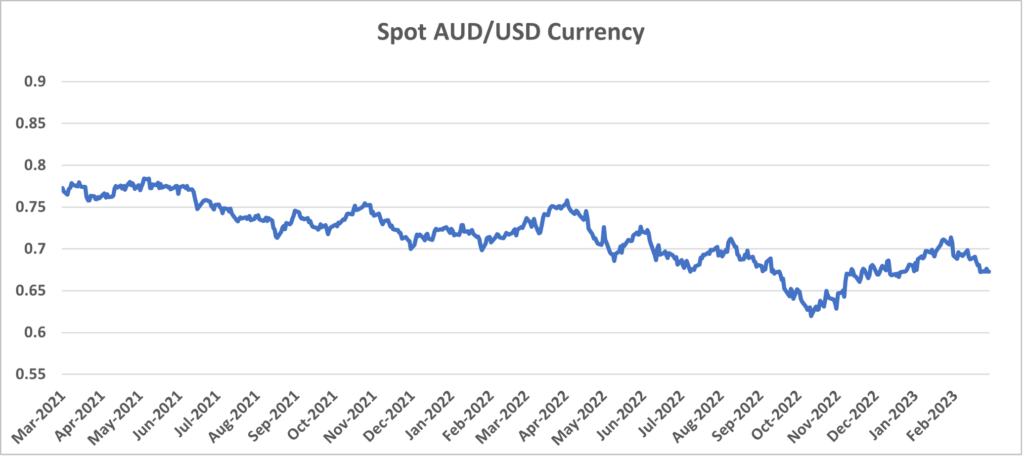

Australian exporters have enjoyed very healthy export margins over the past 12 months and are giving back some of this margin against the Mar/Apr/May’23 sales to pare back shorts. This is evident on the ASX/A$ chart below which has rallied more than $30/MT over the past couple of weeks. Farmers are cashed up following the third consecutive record winter grain harvest. We estimate that farmers are 5-7% behind last year on wheat sales. This may not seem a lot, but when you look at it against a 38.5MMT wheat crop it’s about 2.7MMT which equates to a month of exports. Farmers are also wary of the possibility of a drier season ahead and have been more cautious on the selling programs.

Australia is well into the 2022/23 export season. The overall export pace is higher than 2021/22 at the same time, but there are some variations. Part of this was due to the carryover stocks from 2021/22 which allowed a quick start for the 2022/23 export program. Australia’s combined wheat, barley and canola exports for the Oct/Nov/Dec’22 was 10.15MMT which is more than 2MMT higher than the same period a year earlier. Half of this increase was canola which was 1.8MMT in Oct/NovDec’22 up from 0.82MMT a year earlier. The Oct/Nov/Dec wheat exports were up 1.3MMT on a year earlier, but the barley shipments were about 250KMT less. The shipping stem offers a good idea of what the Jan/Feb/Mar’23 shipping pace will be. It is forecast that the total wheat, barley and canola shipments for the Jan/Feb/Mar’23 will be similar to last year’s 12.3MMT.

Pulse Market Review

The Australian Pulse market moved sideways last week as little new international interest was reported. The weather outlook suggests a decline in rainfall in the autumn months and it is expected that planting intentions will be determined within the next few weeks as farmers look to grow the most appropriate crop for the upcoming season. In Australia, Pulses are recognised for the role they can play in improving subsequent cereal yields, by breaking the cycle of cereal root diseases while maintaining soil fertility. Pulse crops are able to ‘fix’ nitrogen when growing and although most of this is stored in the grain and therefore removed when the crop is harvested, the plants have not taken this nitrogen from the soil and so the need for nitrogen fertilisers is reduced. This combination of higher soil nitrogen and reduced root diseases is cumulative and can result in a dramatic increase in subsequent cereal yields.

Ocean Freight

Positivity is still the name of the game, but it feels like the market is in a period of consolidation and digestion of the rapid advances of the last couple of weeks. Whether this is a plateau before rising again is a moot point – it doesn’t feel like there is a huge change on the supply and demand equation beyond a shortage of ships in Southeast Asia across all sizes. We still note that Chinese controlled tonnage is being pushed in the market which we feel indicates the underlying situation in China is not healthy. Furthermore, this suggests that when the current Indonesian coal export push peters out, as it is very likely to do when the effects of the Indian monsoon arrive in May, then we will see the freight market ease off. We maintain that China is the biggest influence on the freight market so when it looks subdued, then that will hold the key to where the market is ultimately going.

Over the last week, vessel rates continued on their upward trajectory until Thursday and then we saw it activity diminish, a situation which persists into early this week. Bunkers also reversed and headed upwards again which underlined the market positivity for the voyage cargoes. It remains difficult for operators because period numbers, already a solid premium to spot, have been pushed again and so have maintained their spread versus spot.

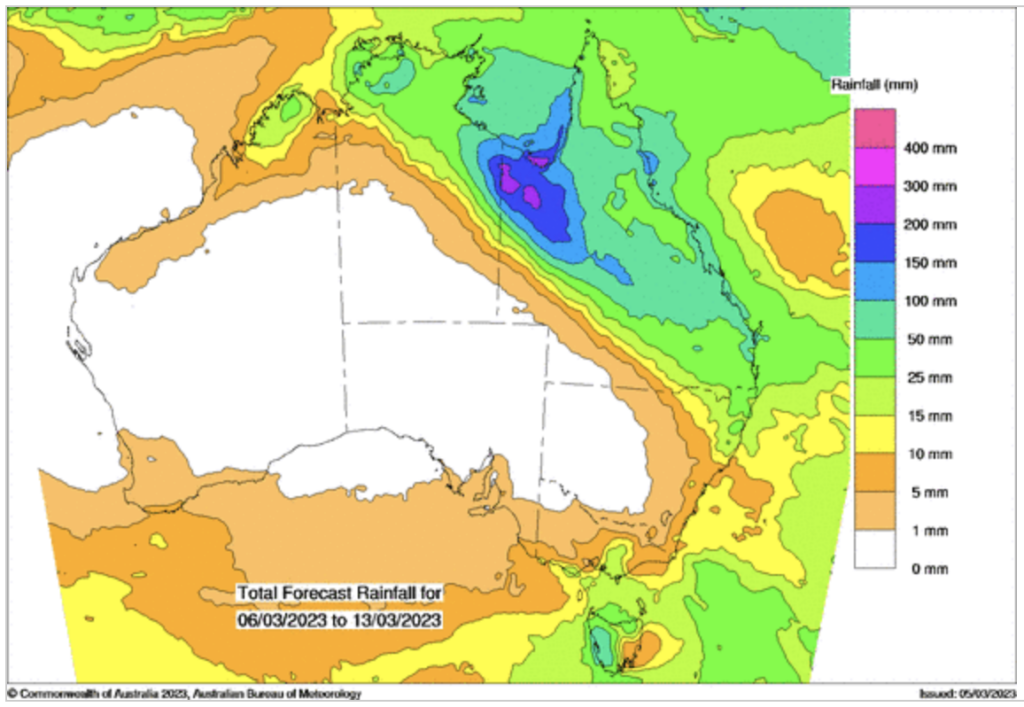

Australian Weather

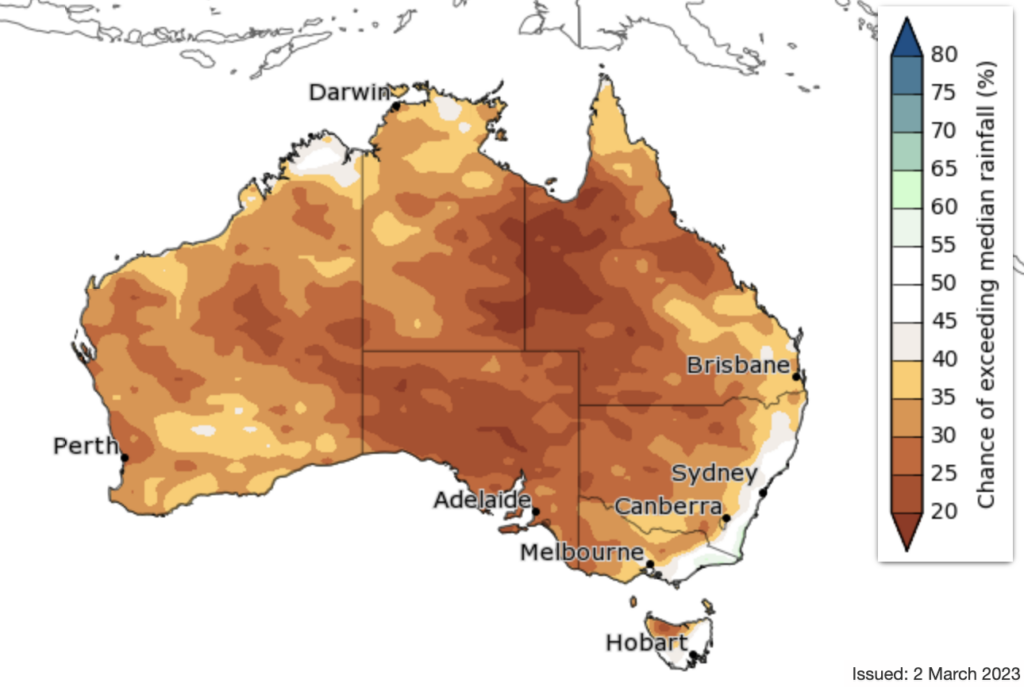

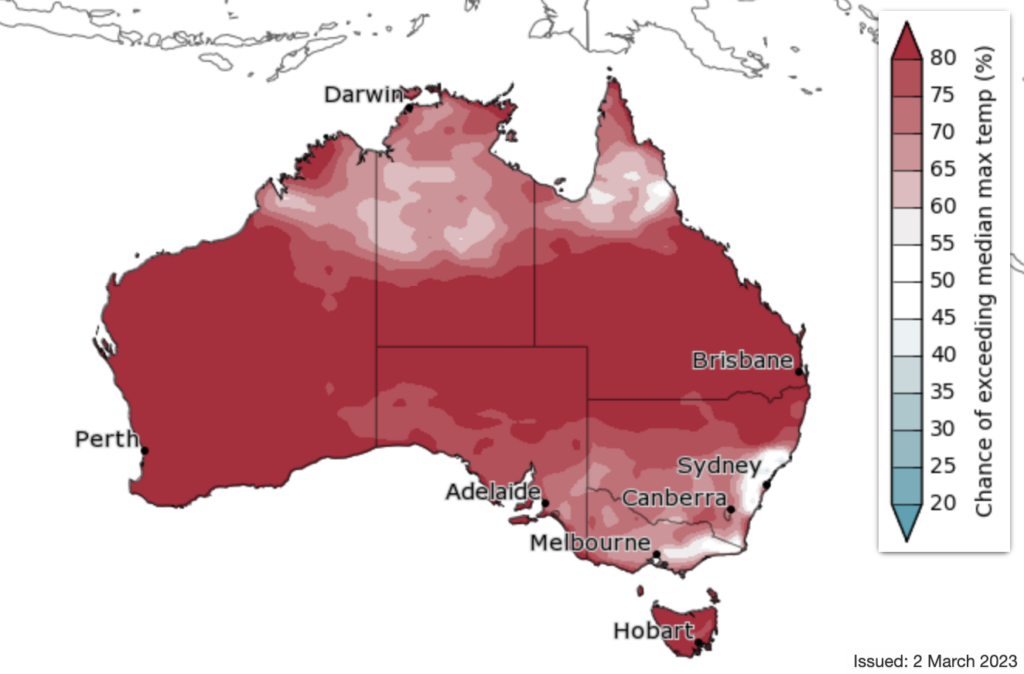

The Australian Bureau of Meteorology’s (BOM) latest Climate Outlook details that most of Australia will see a drier and hotter than normal autumn. This is largely a condition of the weather patterns that have been in place for the summer months where Australia’s cropping areas have seen below average rainfall. Only the tropical north received above average rainfall through summer during its wet season. BOM said there is a 60-80% chance of most of Australia seeing below median rainfall with a similar chance of above median maximum temperatures.

Source: http://www.bom.gov.au/

Source: http://www.bom.gov.au/

This suggests that Australia’s 2023/24 wheat crop is likely to fall back to 25-26MMT with the drier season outlook. Most crop forecasters have the crop higher, however it is anticipated that the national wheat crop will fall below 30MMT with a return to a normal yield on the weather forecast for a drier and warmer season.

Source: http://www.bom.gov.au/

Source: http://www.bom.gov.au/

AUD – Australian Dollar

The Australian dollar was weaker overall last week valued against the Greenback. The AUD/USD jumped from weekly lows below 0.6700 and climbed 0.44% on Friday. Factors like a risk-on impulse and an offered US Dollar (USD) keep the Australian Dollar (AUD) positive. The AUD/USD is currently trading at 0.6737. Looking ahead and all eyes this week will be on the Reserve Bank of Australia (RBA) official cash rate announcement. The Reserve Bank is expected to lift the cash rate for the tenth consecutive time to a decade-high 3.6 per cent on Tuesday in a move that could be followed by at least two more this year if the bond market is right. This will move the AUD higher against the USD.

The post Basis Commodities – Australian Crop Update – Week 10, 2023 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.