Australian Crop Update – Week 44, 2025

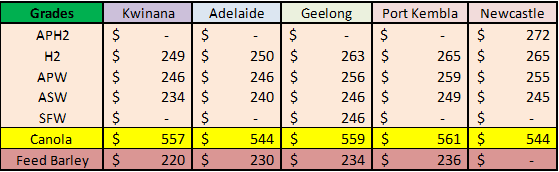

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Last week’s cash markets were relatively directionless as harvest got underway with little grower selling. Canola prices were firmer where the dry finish in Southern New South Wales (NSW) and smaller production has the domestic oilseed crushers rightly nervous. Victoria (VIC) wheat was softer in the new crop following 15-20mm of rain.

On the export front there is still a lot of chatter about the size of the barley program to China. Some have suggested it may already be well in excess of 2.5 million metric tonne (MMT) of sales as China demand has been pricing for some time in both bulk and container terms. Interestingly, it is now very difficult to get offers for export stem before the new year and discussions with a number of exporters suggest they are now focused on Q1 2026 sales.

Australian 2025-2026 Harvest Update:

We took a tour through the Eastern states and in general the north is in excellent shape with yields up in record territory. As you move further south into Southern NSW conditions and yield dropped off sharply but the later crops could still benefit from further rain. This is also the case in VIC. It is too early to draw any meaningful conclusions about quality but it is clear yield is being prioritised over protein so we are expecting, in the east at least, the majority of the wheat crop to be a mid protein APW/AH2 grade.

Grain deliveries in Queensland (QLD) and NSW are increasing as harvest is in full swing in these states. Most of the QLD deliveries have been chickpeas with high protein wheat starting to increase over the weekend. Canola and early wheat are underway in Northern NSW. Canola harvest has just started with the first deliveries of barley in VIC commencing also. South Australian (SA) bulk handlers have also reported early season wheat coming in albeit in small quantities. This will ramp up over the coming week with the dry and favourable harvest conditions.

Based on estimates, Southern NSW wheat, barley and canola yields will fall short of last year. Some crops have been baled for hay rather than seeing them through to harvest. The absence of soil moisture at the start of the season and mediocre in crop rain left crops holding out for finishing rains that didn’t eventuate. This has little to no impact on global markets - except to say Port Kembla may not be as busy as one would expect - but it is significant for the domestic markets that draw from these areas.

In Western Australia (WA), cooler temperatures and timely rain continue to support a big crop getting bigger. However, a low international price for grains has limited inputs so we, like many other commentators, are expecting a low protein year in the west.

The pulse harvest is also gathering pace, with northern crops on track to deliver better yields for chickpeas and faba beans, and lentil harvesting just getting started in the south. Markets for all three pulses remain depressed due to competition from Canada on lentils, and limited interest from India on chickpeas and Egypt on faba beans respectively. Because of the relatively low prices, off-the-header sales of chickpeas, faba beans, and lentils are shaping up to be well down on last year, with barley, canola and hay expected to be more attractive options for prompt sales.

Export Stem & Ocean Freight Market Update:

There was 380 thousand metric tonne (KMT) of wheat, 340KMT of barley and 120KMT of canola added to the shipping stem in the past week. About half of the wheat, 90% of the barley and all of the canola put on the stem last week was from WA.

The ocean freight market saw Atlantic rates fall as the FFA markets were also sold off. The Pacific market has been stable other than a small amount of weather-related disruption causing ships to miss cancelling dates. Sentiment is for more of the same going forward.

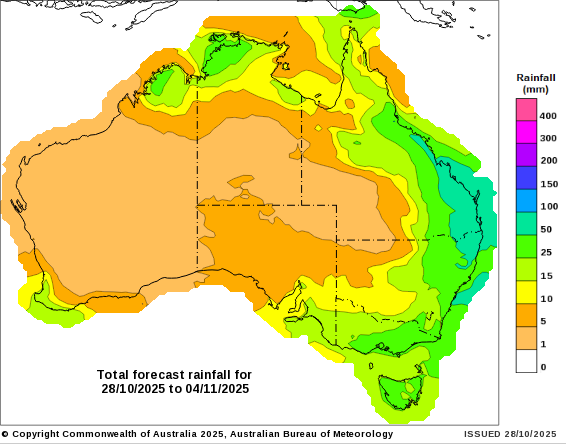

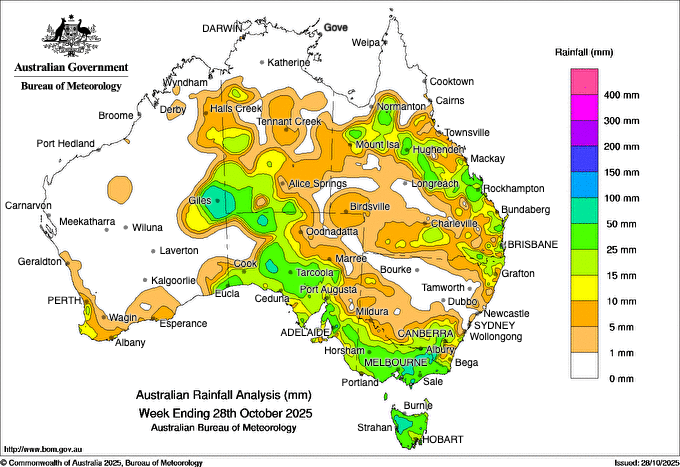

Australian Weather:

WA and SA are expected to get a break from any rainfall over the next week to ten days as the grain harvest and bailing season moves into full production. Eastern states have experienced seasonal storms with QLD and coastal NSW receiving widespread rainfall. Southern NSW and VIC will see up to 30-50mm over the next week which will fortify yields but slow any harvest progress. Daytime temperatures are expected to be mild over the next week providing respite from last week’s highs.

8 day forecast to 4 November 2025

http://www.bom.gov.au/

Weekly rainfall to 28 October 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian Dollar (AUD) was little changed against the US Dollar (USD) last week, as traders digested a fresh batch of mixed US macroeconomic data that sparked short-term volatility but failed to establish a clear directional trend. The AUD/USD pair is trading around 0.6535, largely unchanged after a week of sharp intraday moves following the release of the US Consumer Price Index (CPI) and S&P Global Purchasing Managers’ Index (PMI) reports. From a technical standpoint, AUD/USD continues to consolidate within a narrow 0.6480–0.6540 range, suggesting a period of indecision after the pair’s recent breakdown on the daily chart.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.