Australian Crop Update – Week 45, 2025

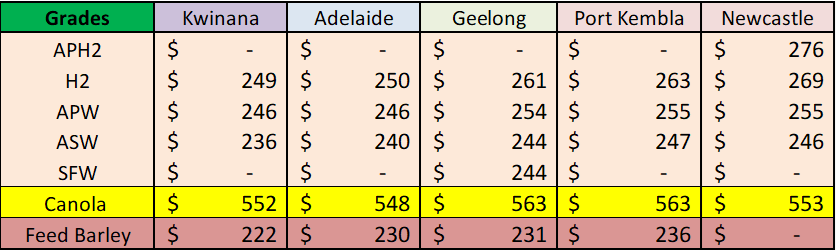

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

The cash markets remained focused on the harvest this week with limited grower selling keeping exporters on the defensive commitment wise until they see grower selling increase. Pricing is being driven by the harvest pace, harvest quality and old crop shorts. The combination of this is making local prices regionally focused, choppy and broadly illiquid. Even so, it appears to be easier to sell barley and canola. Faba beans and chickpeas were also firmer as an exporter short covering was seen in the northern markets. Canola bids remain firm on the back of a below average production outlook for the Southern New South Wales (NSW and Victorian (VIC) market where a lot of the domestic crush is located.

Australian 2025-2026 Harvest Update:

Harvest is progressing across all areas of Australia now. Harvest receivals continue to climb as the northern harvest advanced in Queensland (QLD) and NSW. The Western Australia (WA) harvest is progressing quickly helped by warm, dry days. Record high vegetation index levels indicate bumper yields that should see a bigger crop than last year.

Preliminary yields are aligning with expectations of a near-record crop across these areas, and although soil moisture levels had become very low in some areas prior to the rain, crop quality has held up well.

It is too early to be making any calls on quality, but the East Coast wheat proteins do seem to be lower than expected and hence the protein premiums could possibly widen if this trend continues. There have also been some higher screenings in the wheat coming off in western and southwestern QLD and northwestern NSW, but this is finding heathy demand (blending). It’s too early to make quality comments on the WA wheat crop as very little wheat has been received but the big yields lean to an ASW dominated harvest and 60 pct of receivals to date (only 200 thousand metric tonne (KMT)) have been ASW.

Export Stem & Ocean Freight Market Update:

There was 230KMT of barley, 184KMT of wheat, 90KMT of chickpeas and 55KMT of canola put onto the shipping stem in the past week. It should be noted that close to 1 million metric tonne (MMT) of barley has already been put onto the stem. Most of the barley additions are in WA but there are also some in South Australia (SA) and VIC. In talking to some of the exporters, all of this demand seems to be China and Japan related with SA and VIC getting some premiums for fair average quality sales.

The physical ocean freight market is still slowly easing but levels overall remain relatively firm. Forward curves are flattening at levels above prior expectation - suggestive that the traditional Q1 dip will not be as pronounced. The market is moving beyond January as the forecast low point - probably now more like mid-February in line with stereotype profile of the Chinese NY period. Sentiment also persists that Atlantic will ease disproportionately to the Pacific basin.

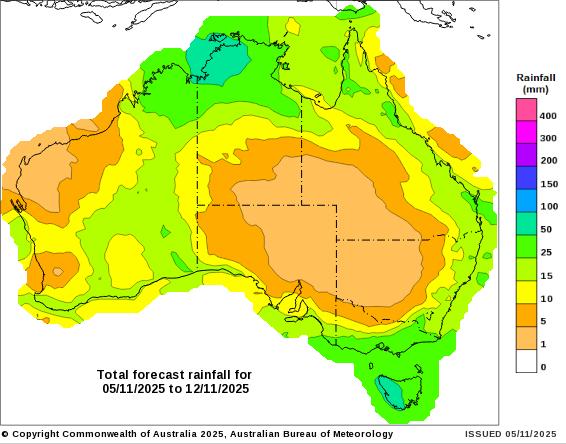

Australian Weather:

Rainfall across Southern NSW and VIC last weekend was welcomed, especially for late-sown crops. Harvest remains at an early stage, with relatively cool conditions slowing crop maturity. The seven-day forecast indicates more rain is on the way for VIC and the eastern parts of Southern NSW and we think this will be beneficial to crops in those areas.

8 day forecast to 12 November 2025

http://www.bom.gov.au/

Weekly rainfall to 4 November 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar (AUD) edged lower on Friday, with the AUD/USD pair trading below .65 in the wake of the US Fed meeting last Thursday. The decline comes as renewed US dollar (USD) strength exerts downward pressure on the Aussie, driven by several supportive factors for the greenback. The USD is benefiting from diminishing expectations that the Federal Reserve (Fed) will adopt a more dovish stance in the near term. A sustained break below the 0.6500 level could open the door for additional downside in AUD/USD.

Locally, the RBA met yesterday and in the wake of stronger than anticipated inflation data they kept the cash rates the same. The RBA staff will need to upgrade near-term forecasts for inflation.

Markets seldom move in straight lines, and more pockets of headline/data driven AUD volatility should be anticipated over the period ahead.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.