Australian Crop Update – Week 46, 2025

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Domestic markets remained sluggish through last week with limited changes to the cash bids/offers. On the East Coast slow farmer selling is very thin and is putting some upward pressure on domestic buyers with signs that domestic feeders are stepping up for purchases in the nearby slots - the first to blink. Northern wheat and barley bids were firmer as the Queensland (QLD) harvest draws to a close with higher protein wheat grades especially well sought. Part of the increase in the wheat market in the north has been from exporters trying to encourage grain deliveries into the up-country sites. Canola is being sought in all port zones by crushers and exporters with purchases being made at levels above the published bids. South Australia (SA) bids were little changed. Western Australia (WA) wheat was $1 per metric tonne (/MT) to $3/MT higher, barley and canola steady.

Internationally Australia took out some feed wheat tenders in the Philippines at a widely reported level of 260 - close to 240 FOB and a look at the stem confirms that barley, canola and chickpeas dominate the export stem up until Christmas. However, unless the grower blinks and starts selling wheat, we seem destined for a very slow start to milling wheat exports given where replacement levels are versus international competition and consumers ideas on value.

Australian 2025-2026 Harvest Update:

Unsettled weather is slowing Australia’s harvest pace although it hasn’t been wet enough to cause any significant quality concerns. Patchy storms delivered heavy rains in parts of Southern QLD and Northern New South Wales (NSW), but they weren’t widespread. Some areas in Western NSW recorded upwards of 60mm while areas in Victoria (VIC) were around 10-15mm. Yields have been generally coming in at or above expectations. Barley yields of 4-5 metric tonne per hectare (MT/ha) have been the norm with some farmers achieving better. WA wheat yields have generally been 2.5 MT/ha or better with early harvest to the east higher than last year. Premiums for high quality milling wheat are climbing with wheat protein levels generally coming in 0.5 to 1.0-pc below expectations. Most of the wheat deliveries are making APW and ASW, and Noodle wheat with smaller volumes of AH11.5. Little wheat has been coming in above protein so far. Farmer selling remains slow and reserves with many opting to hold back in hope of higher prices. Wheat harvest in QLD and Northern NSW is 80-90% complete. Wheat harvesting in the western areas of Northern NSW is seen as ~50% while the eastern areas are still in the early stages. Harvest is just starting in the western parts of the NSW Central West while canola and barley is well-underway. It’s still very early in the WA, VIC and SA harvest as can be seen by the BHC deliveries. It is also still relatively cool which will be good for yield but means this harvest will have a long tail.

Export Statistics – September 2025

Australia exported 1.92 million metric tonne (MMT) of wheat in September, modestly higher than the 1.86MMT in August. This lifted Australia’s FY 25 wheat exports to 23.5MMT. Indonesia was the largest destination with 4.5MMT followed by the Philippines with 3.5MMT, then Thailand and Vietnam both taking around 1.6MMT. South Korea was next with 1.5MMT, then Japan with 1.15MMt and then China and Malaysia with a tad over 1.0MMT. China’s exports tumbled from 3.75MMT in 23/24 to 1.05MMT in 24/25. Exports to Africa nearly tripled year on year to 2.37MMT. Most of this was when Russia’s export quota came into effect in Q2 and Q3 2025.

Barley exports for Sep were 309.6 thousand metric tonne (KMT). This puts Australia’s FY 25 barley exports at 8.3MMT. WA has exported 5.5MMT of barley for 24/25, VIC 1.2MMT and 0.74MMT from both NSW and SA. China was the dominant destination with ~6.0MMT which was similar to 23/24. Japan was the next largest with ~0.6MMT and then Saudi with ~0.4MMT. A bit over 0.4MMT of malting barley was exported to Latin America.

Australia’s canola exports for FY 25 were 5.4MMT down from 6.1MMT in 23/24. WA accounted for 2.9MMT of the canola exports followed by VIC with ~1.3MMT, NSW 0.92MMT and SA with 0.38MMT. Europe was the major destination with 3.7MMT, then 0.62MMT to the UAE, Pakistan ~0.5MMT and 0.28MMT to Japan.

Chickpea FY25 exports were 2.1MMT, lentils 1.05MMT down from ~1.5MMT in 23/24 with the smaller crops in SA and Vic. Faba bean exports were 0.65MMT.

Export Stem & Ocean Freight Market Update:

It was a strong week for shipping stem additions. This included ~660KMT of wheat, 360KMT of barley and 360KMT of canola. Most of the wheat was put on in WA but there was also ~200KMT put onto the stem in SA. SA also added 215KMT of barley for the week. The monthly split of the stem shows that 900KMT of barley is forecast to be shipped in November with ~450KMT already on the stem for December. There is also 860KMT of wheat scheduled to be shipped in November and 660KMT of canola.

The ocean freight market is still struggling to find its next direction as we edge closer to the Christmas period. Rates are holding flat for the most part however there are signs for softening or firming depending which sector you study. The Panamax sector was subdued in the early part of the week as prompt ships struggled to find cover. However, by Friday, the sentiment had turned. In the Atlantic more demand appearing from South America was enough to give owners hope while in the Pacific, owners welcomed the sight of fresh coal demand coming from Indonesia and East Australia. These factors were enough for this sector to close higher on the index than the previous week.

The Supramax/Ultramax treaded water in the Pacific as the market is being described as "positional". Ultras are still trading at a 2-3kpd premium to Supras but without a fresh bout of cargoes we would expect to see rates contract. On the near term outlook owners are holding onto hope rates should hold (and possibly firm) going into Q1 as the expectations of a bumper Australian grain harvest grow. The Atlantic was a lackluster affair for the Supramax/Ultramaxes throughout the week as all areas conceded ground until Friday when the USG suddenly sprung into action with fresh cargoes leading to the index to jump 1000 points on the USG fronthaul route.

The Handy sector was quiet all week in both basins as the market struggled with sluggish activity and rates slipping below last done levels.

Australian Weather:

Southeast Australia will see unsettled weather over the weekend and extending into next week. This is likely to include showers over the weekend with the chance of thunderstorms next week.

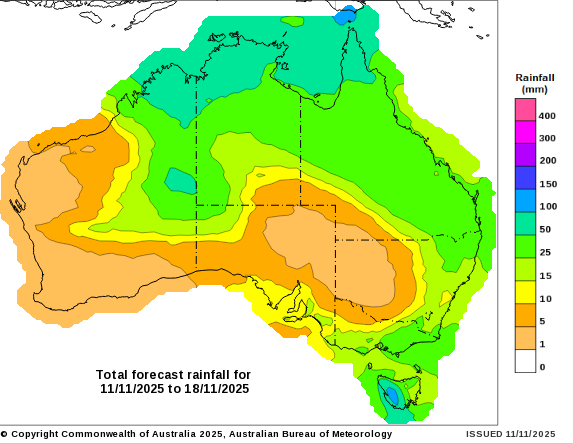

8 day forecast to 18 November 2025

http://www.bom.gov.au/

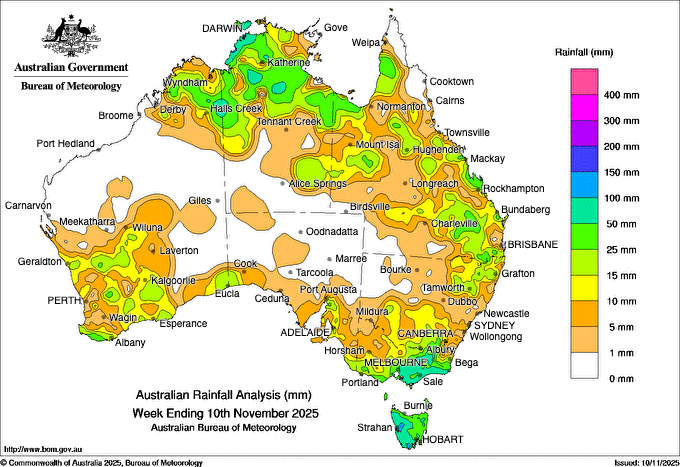

Weekly rainfall to 10 November 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian Dollar (AUD) showed steady strength to close last week, with the AUD/USD pair trading above a key support level at 0.6450. The currency’s resilience reflects growing investor confidence that an improvement in Australian labour market conditions should reinforce views that the RBA will remain on a different interest rate path to its peers. We think the mix of sticky Australian core inflation, a resilient jobs market, and signs of improvement in growth momentum may mean the RBA doesn’t cut interest rates again this cycle. Markets don't move in straight lines and more bouts of headline/data driven volatility should be anticipated. But on net, we continue to project the AUD to make gains into year-end and over early-2026 because of improvement in US/China trade relations, diverging policy trends between the RBA and other central banks such as the US Fed, more favourable yield spreads, and/or firmer growth in China as its stimulus push gains traction.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.