Australian Crop Update – Week 47, 2025

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Local markets remained depressed for most of the week with the mix of big crops, low global prices, slow farmer selling, strong export competition (particularly from South America) all influencing a slow start to the marketing campaign. There are plenty of bids below the market, but not too many sellers. Some of the malaise may also have been influenced by the USDA’s first reports since the federal government shut down ended, so plenty of data to catch up on and digest. Bulls may now wish that the US government would go back into a shutdown as the market is reminded of its bearish fundamentals across corn, wheat and beans. Sell the fact as they say.

Southern markets were little changed week on week. Southern barley markets are fickle, with the bids climbing against slow farmer selling. Western Australia (WA) wheat and barley was little changed for the week, highlighting the growing spread between export offers between the west and east.

Australian 2025-2026 Harvest Update:

Grain harvesting is beginning to advance more quickly across Australia’s cropping zones this week. The Queensland (QLD) harvest is mostly finished with Northern New South Wales (NSW) harvest also well advanced. The Victorian (VIC) barley harvest is estimated at 33% complete with South Australia (SA) and WA also picking up the pace in the past week for barley and canola at least.

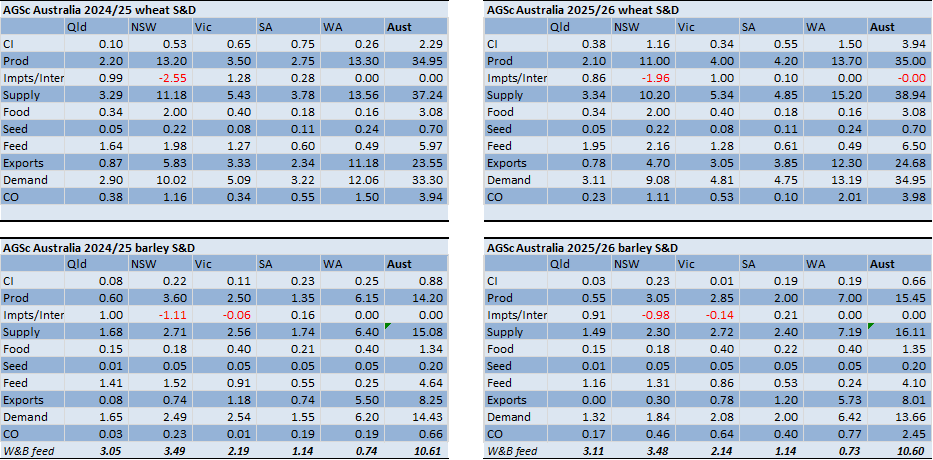

Ag Scientia Balance Sheet Updates:

We released changes to Australia’s 2024/25 and 2025/26 balance sheet. The main changes this month are the finalisation of the 2024/25 marketing year exports following the release of the ABS Sep-25 exports. Australia’s 2024/25 wheat exports were 23.5 million metric tonne (MMT), barley exports were 8.25MMT and canola exports 5.4MMT. The most notable part of the finalisation of 2024/25 was that NSW and QLD’s quarter 4 exports were the largest wheat export quarter for the 2024/25 marketing year - who would of thought it. Whereas quarter 3 was the largest wheat export quarter for VIC, SA and WA. The point of this is that it tightens the 2024/25 ending stocks in QLD and Northern NSW from the anticipated heavy stocks that were being talked about just a few months earlier.

We haven’t made many changes to the new crop numbers, although our bias, based on a cool finish, is that we will see an increase in production numbers over the coming month. Total wheat production is conservatively forecast at 35.0MMT, barley 15.4MMT and canola 7.0MMT. WA is expected to see record crops which should see CBH receivals of ~26MMT. Late rain in SA and Vic will benefit late crops in these states. NSW is very good in the north but poor in the south. The northern harvest is advanced, and yields have been strong. Harvest activity is now focused on the Central West and just cranking up in the Riverina. We are working on below average yields in Southern NSW.

It’s going to be an interesting season.

Export Stem & Ocean Freight Market Update:

It was a leaner week for shipping stem additions this week with ~750 thousand metric tonne (KMT) of grains, canola and pulses added down from ~1.4MMT in the previous week. This included 55KMT from Newcastle and 100KMT VIC as well as 25KMT in SA and 160KMT in WA. A further 130KMT of barley was added to the stem in the past week, the smallest in four weeks. However, pulse additions were stronger with 130KMT of chickpeas, 108KMT of lentils and 20KMT of faba beans

In the world of ocean freight, little has changed except to say owners have expectations of a firmer than usual start to 2026 - well they would, wouldn’t they.

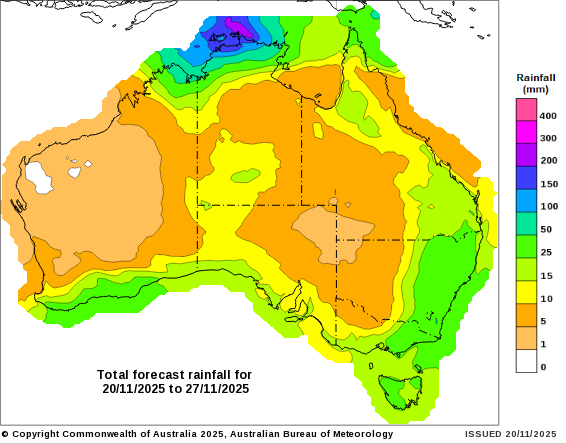

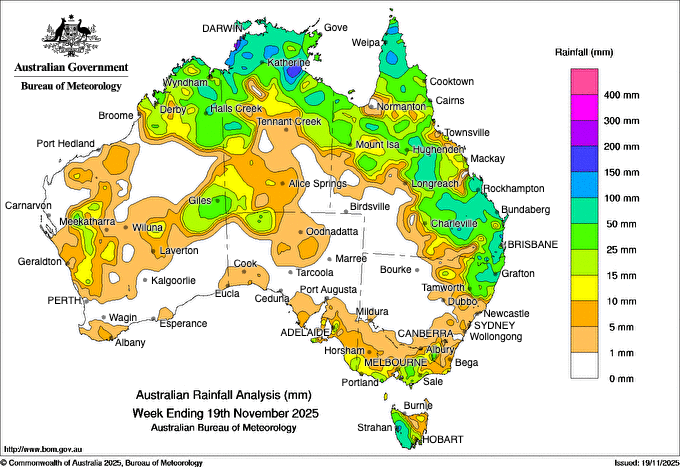

Australian Weather:

Storms hit QLD and Northern NSW, last week but this will have limited impact on the harvest with most of the crop off in these areas. The storms are beneficial for summer crops in Central QLD, Southern QLD and Northern NSW.

Elsewhere dry weather saw the headers working around the clock.

8 day forecast to 27 November 2025

http://www.bom.gov.au/

Weekly rainfall to 19 November 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The AUD/USD pair traded higher on Friday, hovering near 0.6530 and marking a gain of around 0.30% for the day. The move reflects renewed demand for the Australian Dollar (AUD), supported by solid economic data from both Australia and China, while the US Dollar (USD) continues to face a cloud of uncertainty. Together, these factors have encouraged investors to adopt a slightly more optimistic stance toward the AUD as they headed into the weekend.

Markets have largely abandoned the idea of an RBA cut this year, not because policymakers are hawkish, but because the data isn’t giving them room to ease. With no major domestic releases this week, the Australian dollar will take its direction from the US as agencies begin clearing the backlog of delayed reports following the government shutdown there.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.