Australian Crop Update – Week 43, 2025

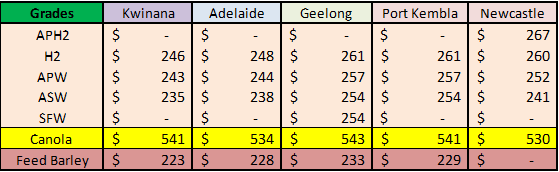

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Local grain prices pushed higher last week aided by the weak Australian dollar, yield punishing weather across southeastern Australia and slow farmer selling. Traders are reporting that wheat is difficult to buy in Southern Queensland (QLD) and Northern New South Wales (NSW) where farmers are holding out for higher prices. We see the sharp increase in the wheat prices across NSW and Victoria (VIC) as the bulk handlers’ attempt to draw wheat into up-country storages. The market is reporting that wheat and barley old crop offers have dried up across Southeast Australia, making it virtually impossible to cover old crop positions (Nov/Dec). Western Australia (WA) wheat bids were generally a couple of dollars firmer, helped by the void of farmer selling on the east coast. The market is very much in flux with weather and the north and south moisture levels as the 2025/2026 harvest gets underway.

Australian 2025-2026 Harvest Update:

Warm weather continues to allow barley and early wheat harvest in QLD, NSW, South Australia (SA) and WA. The themes are unchanged, WA, Northern NSW and QLD are on track for above average yields while the dry finish is shrinking yields in Southeast Australia. It’s early days but most are reporting that farmer selling is negligible. High protein wheat is being harvesting in Southern QLD and Northern NSW. There are also reports of some screening issues. The hot, dry finish has been conducive for higher wheat proteins across eastern Australia, but this is also likely to result in screenings and possible test weight issues. The market impacts are that Australia is still going to have large wheat, barley and canola crops.

Export Stem & Ocean Freight Market Update:

New crop barley, canola and wheat are starting to come onto the stem more liberally. A further 115 thousand metric tonne (KMT) of barley was added to the stem in WA through the week, as well as 170KMT of canola and 115KMT of wheat. East coast additions are slow and waiting for the harvest to advance. Traders are becoming increasingly cautious about shorting growers due to slow farmer selling and yield estimates taking a further hit this week with the hot and windy weather conditions. East coast additions amounted to just 30KMT of wheat put on the stem into Melbourne.

Market sentiment was mixed this week with uncertainty creeping in as China’s newly introduced port service fees began to take effect. While the full impact of these measures is yet to be seen, there’s little doubt they will disrupt traditional trade flows in the weeks ahead. After an early surge in Capesize rates on the back of this news, momentum eased and the week ended on a steadier tone. The power struggle between the US and China has left many market participants watching from the side lines and unsure of near term direction. Still, fixing levels held firm across both basins. The USG and ECSA regions continue to show resilience and balance, while the Pacific remains steady with tight tonnage lists particularly around Southeast Asia and Aussie. Additionally, there has been minimal movement in period rates which suggests confidence in the market remains (at least in the short term). Across all dry bulk segments, the week ultimately closed slightly up across the board. Attention now shifts to the week ahead as the market looks for clearer signals amid ongoing uncertainty, further influenced by recent political developments in the Middle East.

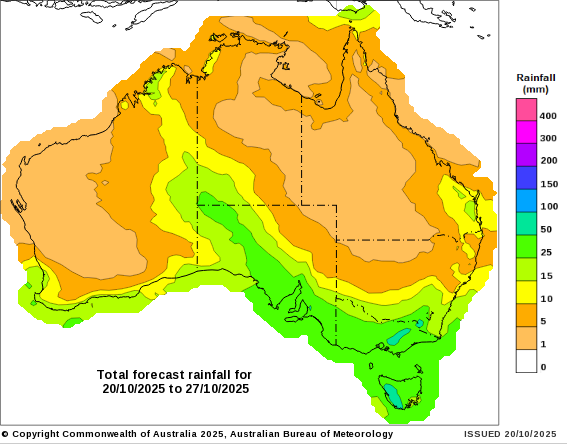

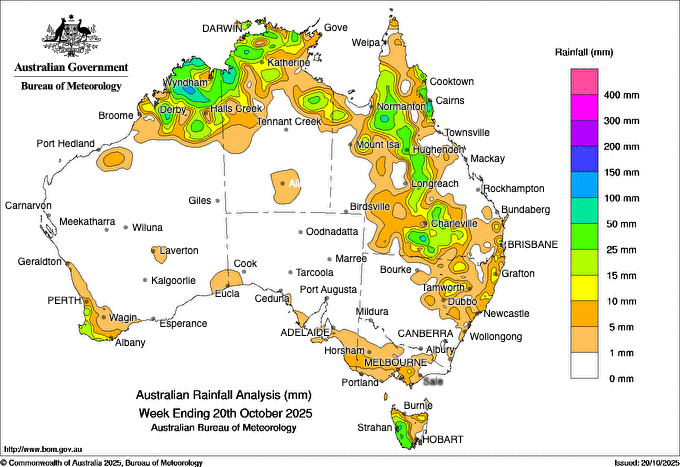

Australian Weather:

Hot, dry winds sapped significant yield potential out of crops through Southeast Australia in the past week, as well as a good deal of optimism out of the market. Declining yield and production potential across Southeast Australia also appears to be bolstering grower resolve to hold back on grain sales at current prices. While it was another dry week across Australian cropping areas, it was the hot gustily winds on Wed/Thu that will have hurt crops. Areas stretching from NSW, VVIC and SA were hit by hot temperatures and gusty winds which would have sapped any remaining moisture from already parched crops. Temps reached 37-38 C with wind gusts of upwards of 40-50km/hr. Until then, mild temperatures across most of Southeast Australia had been shielding crops from the lack of soil moisture. The burst of hot weather will lock in average to below average yields in a lot of areas across Southeast Australia. The bottom line of the above is that NSW yields won’t be as good as last year. Northern crops have lost potential with the hot, dry finish while the southern crops are likely to have suffered the most.

8 day forecast to 27 October 2025

http://www.bom.gov.au/

Weekly rainfall to 20 October 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian Dollar (AUD) remained under pressure on Friday, with the AUD/USD pair declining by 0.5% to trade around the 0.6450 level during the European session. The currency’s weakness reflects a combination of intensifying global economic risks and softening domestic fundamentals, both of which are prompting investors to adopt a more cautious stance toward the AUD. One of the key factors dragging the Australian dollar lower is the resurfacing of trade frictions between the United States and China. As the world’s two largest economies engage in renewed disputes over tariffs, technology restrictions, and geopolitical influence, risk appetite has taken a notable hit.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.