Australian Crop Update – Week 42, 2025

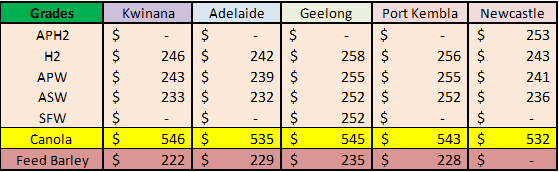

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Domestic markets were firmer last week helped by a 2% decline in the AUD as well as deteriorating crop conditions across Southeast Australia. Grain and canola prices were broadly firmer in all zones with sorghum and pulses weaker. Grain prices in Southeast Australia saw the biggest gains with markets up USD7 per metric tonne (/MT) for the week for protein grades as crops come under stress with the absence of finishing rains.

Exporters are patient, however across most zones where supplies will be large, there will be a requirement for sizable export programs to move the new season crop. This has changed however for Southeast Australia where the crop is shrinking. These areas will still have significant export surpluses, but the surplus will be lower. Northern and Western Australia (WA) markets are export competitive at current prices however international demand is lacklustre and farmer selling is slow at current prices. The forecast Australian wheat crop of >34 million metric tonne (MMT) will require prices to be export competitive through much of the season to attract sales for a 24-25MMT export task.

Australian 2025-2026 Harvest Update:

Barley harvest is underway in Queensland (QLD) keeping pressure on the delivered prices into the feedlots and for the first export vessels. Early wheat harvest has already started in some parts of the South West of QLD. The rapid dry down of the crop with hot, dry weather in recent weeks is expected to trim yields slightly but result in higher proteins. Reports of wheat being harvested in the west of QLD is consistently delivering >13% protein. This pattern is expected to continue into Northern New South Wales (NSW) as wheat harvesting pace picks up in the next 7-10 days.

Export Stem & Ocean Freight Market Update:

New crop vessels are starting to be added to the stem with 242k thousand metric tonne (KMT) of barley put on the stem in WA last week. This included 4 x 60KMT vessels which is assumed to be heading to China. There was also 200KMT of canola put on the stem in WA and 280KMT of wheat added to the stem which will be mostly old crop.

On the freight market, a sluggish start to last week with regional holidays in China and Korea caused activity levels to be to subdued. Rates gently eased as a result in the Pacific but not to the extent some charterers were hoping for which led to a decent standoff in the bid/offer spread. However, once China returned to the office on Thursday, there was a shift in the sentiment with more cargo demand appearing on all sectors. Panamaxes was active from Nopac, Australia, Indonesia and was still being lured towards ECSA, causing tonnage to remain on limited supply as rates began to climb again. The Ultramaxes followed a similar trend. Rates lost ground in the early part of the week as standard Nopac/Pacific rounds were being concluded 1-2kpd less than previous weeks however the tide changed and showed sign of improvement (albeit at a slower pace than the Panamaxes) by Friday. The Handysize sector trended sideways throughout the week. Despite the low activity levels, tonnage remained tight.

Looking forward there is an expectation of greater demand coming from Australia (especially on grains) so sentiment is looking positive leading up to Christmas in the Pacific.

A close watch going forward for the shipping markets is the USTR implementation of tariffs due this week on Chinese owners/tonnage and the counter measures announced on Friday by China on US owners/tonnage. The Israel/Gaza war has taken initial steps towards peace after two years of conflict and if it continues down that path, we would expect to see a greater traffic willing to transit the Suez/Red Sea/Bab-El-Mandeb corridor.

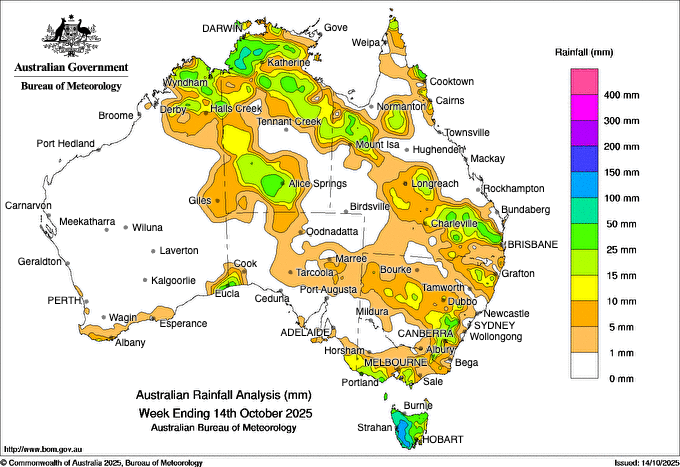

Australian Weather:

There are deteriorating crop outlooks in Southeastern Australia as traders and domestic buyers moved on securing volume. Traders were securing wheat throughout last week in Victoria (VIC) and Southern NSW with bids climbing by USD7-10/MT during the week. Time for crop saving rains across the region is starting to run out and while the Australian Bureau of Meteorology forecasted a wetter than normal spring, weather across eastern Australia hasn’t materialised. VIC cropping areas only received about 20mm of rain in September which is 50-60% of the monthly average. Forecasts remain dry for the next week or so. Soil moisture reserves are critically low following below average in crop rainfall.

8 day forecast to 21 October 2025

http://www.bom.gov.au/

Weekly rainfall to 14 October 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar (AUD) is showing signs of stability at the start of the new week, recovering some of last week’s losses against the US dollar (USD). On Monday, the AUD/USD currency pair climbed back above the key US$0.6500 level after briefly dipping to its lowest point since August 27, around US$0.6472, during Friday’s trading session.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.