Australian Crop Update – Week 39, 2025

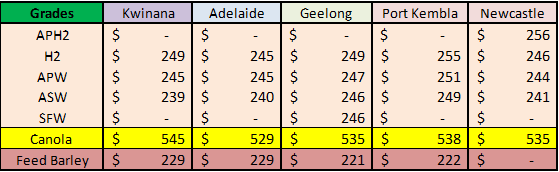

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

ocal grain markets ended last week mixed across the port zones. Cash bids for wheat and barley in Southern Queensland (QLD) and Northern New South Wales (NSW) were a couple of dollars higher for the week. Buyers started to lift prices as farmer selling slowed, particularly in the new crop. Grain prices were softer further south which has resulted in a narrowing of the southern risk premium. Western Australia (WA) wheat prices bounced last week on the back of recent kick in export demand.

Australian 2025/2026 Crop Forecast - September 2025:

2025/26 wheat, barley and canola production has been raised by the improving crop conditions. Wheat production is forecast at 34.2 million metric tonne (MMT), barley at 14.6MMT and canola at 6.5MMT. The production estimates are similar to ABARES and are justified on planted areas and current crop conditions supported by vegetation index ratings. Australia’s 2025/26 wheat exports forecast has been raised to 25.0MMT (+1.8MMT year on year), barley exports at 8.0MMT are about the same as 2024/25, canola exports of 4.75MMT are down 0.65MMT on 2024/25.

Australian Pulses Update:

Australia exported 24,951 metric tonnes (MT) of chickpeas and 89,320MT of lentils in July, according to the latest data from the Australian Bureau of Statistics. Lentils exports in July rose 79percent (pc) from the June total of 50,032MT, with India the biggest market on 44,465tMT followed by Bangladesh on 22,651MT, and Sri Lanka on 18,522MT.

Export Stem & Ocean Freight Market Update:

Less that 500 thousand metric tonne (KMT) of wheat was added in the past week for late September and first half October shipment (mostly Newcastle NAT).

On Ocean freight, Panamaxes are gently easing again in both basins after a couple of strong weeks of gains. The Altantic is suffering from a lack for fresh demand hitting the market, especially from ECSA, causing tonnage supply to grow. Owners are yet to admit to the new norm which is causing the bid/offer spread to widen considerably, but without a fresh flow of cargo hitting the market, it will leave owners little choice to accept charterers revised levels. The Pacific followed a similar path as activity levels lost pace as charterers began to push rates lower as the week progressed.

The Ultramax sector is in a holding pattern as the participants appear to be happy to trend sideways after a few strong weeks of growth.

The Handysize sector has again proven to be remarkably resilient (as seen all year) in both basins. The Altantic is witnessing a slight uptick in rates but nothing substantial while the Pacific can be described as holding firm. Although, there may be a notable two-tiered market emerging in Pacific (especially in Southeast Asia) with the rate spread between large modern handies compared to older smaller handies growing slightly wider than expected recently. Australia is a close watch in the Pacific as subdued activity levels over the past few weeks has been a contentious talking point.

Australian Weather:

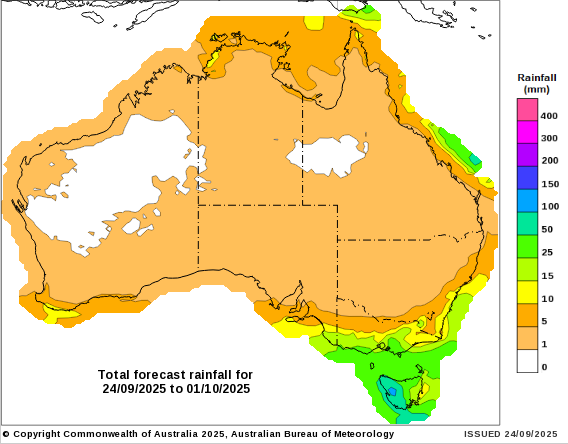

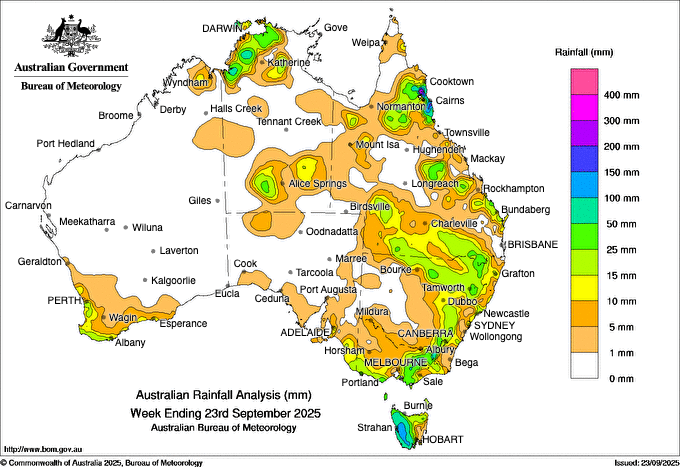

There were showers across NSW late in the week of up to 25mm in some regions fortifying crop development. There were also some light showers in Victoria (VIC) of 5-10mm. The forecast is mostly dry for the next 10 days over the major cropping areas. Soil moisture levels are above average in Southern QLD, Northern NSW and WA while Southeast Australia is average to above average. Southeast Australia needs another good rain event to finish the crop. Nearby temperatures are below average for the next week but are set to warm in late September.

8 day forecast to 1 October 2025

http://www.bom.gov.au/

Weekly rainfall to 23 September 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar (AUD) continued its downward trajectory against the US dollar (USD) last week, marking consecutive days of declines in the currency pair. The AUD finished in negative territory for the first time in four weeks, reflecting the ongoing strength of the US dollar following the Federal Reserve’s recent monetary policy announcement closing the week at 0.6582.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.