Australian Crop Update – Week 40, 2025

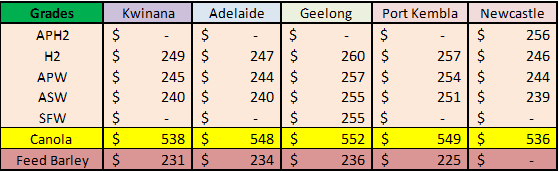

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Local wheat and barley bids were firmer last week in most areas. This is attributed to the weaker AUD while global export values were close to unchanged. The AUD dipped by a further 0.7% last week to 0.6540 and is now back 1.5% in the past two weeks. Wheat futures ended the week modestly lower but Black Sea wheat quotes were firmer. IGC pegged Russian 12.5 pro at USD228 per metric tonne (/MT) FOB mid-week, up from USD226/MT a week earlier. IGC kept its Australian APW FOB quote unchanged at USD244 FOB/MT through the week while the ASW quotes were down to USD241/MT FOB, which we are putting down to a looming large Western Australia (WA) crop which is expected to be ASW dominated. Australian barley markets were also firmer. Risk premiums in Southern New South Wales (NSW) and Victoria (VIC) are building with the absence of a finishing rain.

Australia exported 155,289 metric tonnes (MT) of canola in July, according to the latest data from the Australian Bureau of Statistics. July shipments were up 53 percent from the June figure of 101,766MT, but were roughly one third of the 386,033MT shipped in July 2024. Japan on 76,357MT, the United Arab Emirates on 64,335MT, and Malaysia on 6,584MT were the three biggest markets for canola shipped in July 2025. As often happens in July, European ports were absent from the destination list to reflect Australia’s biggest canola market switching to its own new-crop rapeseed supplies.

Australian 2025/2026 Crop Forecast - September 2025:

2025/26 wheat, barley and canola production has been raised by the improving crop conditions. Wheat production is forecast at 34.2 million metric tonne (MMT), barley at 14.6MMT and canola at 6.5MMT. The production estimates are similar to ABARES and are justified on planted areas and current crop conditions supported by vegetation index ratings. Australia’s 2025/26 wheat exports forecast has been raised to 25.0MMT (+1.8MMT year on year), barley exports at 8.0MMT are about the same as 2024/25, canola exports of 4.75MMT are down 0.65MMT on 2024/25.

Australian Pulses Update:

Falling chickpea and lentil prices are yet to produce a run of forward sales from growers in the past week. Domestic demand remains limited as those with livestock are happy to wait for harvest pressure to drive prices down further. Weak chickpea prices have so far failed to spark volume forward sales of wheat and barley in the northern region also. Export demand has been lacklustre with international markets reverting to spot purchases and awaiting the market to find a floor before engaging ahead of the Australian new crop harvest.

Export Stem & Ocean Freight Market Update:

It was a relatively quiet week for shipping stem additions. There was 271 thousand metric tonne (KMT) of wheat added to the stem in the past week down from 541KMT a week earlier. Most of the additions were in WA. There was 60KMT of canola put on the stem in Kwinana and no barley added to the national stem last week.

As China's golden week fast approaches the overall market appears to be well-balanced and will hold firm throughout the long holidays. The Atlantic for the Panamax and Ultramax sectors are still being well supported with grain demand, especially loading ex ECSA. The North Atlantic has been more subdued over the past week compared to the previous month with limited fresh enquiry hitting the market. The charterers are trying to lower the rates for Trans-Atlantic rounds but owners have managed to resist for more.

The Pacific for Panamax and Ultramax was active early in the week as charterers looked to cover prior to Golden Week. Australia was active with mineral demand and Indonesia coal export was healthy. The Fareast and Nopac was quieter than the recent norm, but rates held steady for most of the week. However, by Friday a sense of softness had begun to creep into the sentiment as market participants took a cautious outlook. The Handysize index gained ground again and closed above $15,000 (strongest level all year).

The Pacific remained active as rates trended sideways for the most part as a general lack of available tonnage was still a major factor (not helped by Typhoon Ragasa wreaking havoc on Philippines/South China regions) while the Atlantic had another positive week buoyed by an increase in cargoes ex CONT as the USG and ECSA held steady.

Australian Weather:

The Australian Bureau of Meteorology (BOM) issued its latest climate outlook for the coming weeks and months. It continues to point to above average rainfall for the eastern half of Australia for Oct to Dec and neutral weather for WA. Assuming the BOM’s forecasts are correct, the big issue is the timing of the rain for Southeast Australia. These areas lack enough moisture to finish crops without yield losses. The weekly forecast shows below average rain for most of Australia’s cropping regions through to Oct 12th and then more of a neutral period for the next week. Dry weather in the first half of Oct and possibly warm temps would result in yield losses through Southeast Australia. Some crops in these parts will be already starting to dry down and will be losing yield potential by then. This would result in lower yields through Southeast Australia, but this is still likely to be compensated by the strong yield outlook for WA. A 5% drop in production across Southern NSW, VIC and South Australia would be offset with a 5% lift in WA production, which is looking likely. Finishing temperatures over the next month will be critical.

8 day forecast to 6 October 2025

http://www.bom.gov.au/

Weekly rainfall to 29 September 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar (AUD) held its ground against the US dollar (USD) to close last week at .6540, pausing a two-day losing streak driven by renewed strength in the Greenback and broader market risk aversion. The AUD/USD pair had come under pressure earlier in the week as stronger-than-expected economic data out of the United States bolstered demand for the USD.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.