Australian Crop Update – Week 38, 2025

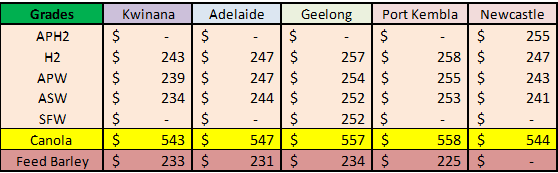

2025-26 - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Australian domestic markets were softer last week across all zones under the weight of weaker international prices, a stronger AUD as well as improving prospects for Australian winter crop. There were reports of farmer selling in northern NSW early last week, but this disappeared later in the week as the AUD continued to climb. The general view is that farmers will sell as little as they can at harvest and store what they can in the hope of better prices post-harvest. It is shaping up to be a more difficult marketing environment for the farmers than the 2024/25 crop when pulse and canola prices were relatively healthy and these sales allowed farmers to be more selective sellers of wheat. The decision of what crops farmers are prepared to sell at harvest to keep their bankers happy will be more difficult this year than last.

There were reports that Australian exporters had sold reasonable volumes (0.5 million metric tonne (MMT) plus) in recent weeks into Southeast Asia. Aussie wheat has been competitive with other origins into Southeast Asia. Sales were reportedly for Nov/Dec, and even some Jan we are told. These sales along with a significantly early barley program into China, feed wheat into the Philippines and Canola into China and Europe have certainly tightened the stem for buyers of early new crop milling wheat.

Australian New Crop Estimate

The USDA topped ABARES in its September WASDE report when they forecast the Australian 2025/26 wheat crop at 34.5MMT and barley at 15.0MMT. NDVI data shows that crop conditions in Northern New South Wales (NSW), Southern Queensland (QLD) and Western Australia (WA) are well above average, but not as good as last year. Crop conditions across Southeast Australia are better than average however they need some additional rain to finish. It should be said that most of the crop looks late, so we still have a bit of time to go.

Export Stem & Ocean Freight Market Update:

It was a very lean week for shipping stem additions. Total stem additions for week 37 were only 138 thousand metric tonne (KMT) of wheat. This included 110KMT of wheat in WA and 28KMT in Brisbane QLD. There were no other new nominations with other grains.

The ocean freight market remains steady with demand in the Atlantic driving strong front-haul business. That said, we don't see too much more upside on freight rates in Pacific - it's more a question of how long can owners sustain current levels. FFA performance suggests the firm market will last into November. There was a $25pmt drop in bunkers over the last week.

Australian Weather:

The Australian Bureau of Meteorology (BOM) updated its long-range forecast overview. This continued with the pattern of a wetter than normal spring for the eastern half of Australia. Rainfall is likely to be above average (60% to 80% chance) for most of the eastern half of Australia, with October showing the strongest signal for above average rainfall. The west is showing equal chances of above average/below average. During October and November, northern Australia gradually builds towards the wet season, bringing increased humidity, storms, and showers. The BOM is forecasting a higher chance of above average temperature for Oct/Nov for southeast Australia and southeast WA. Another southerly front is forecast for Victoria (VIC) and Southern NSW late this week which could offer rain for VIC. South Australia (SA) remains mostly dry.

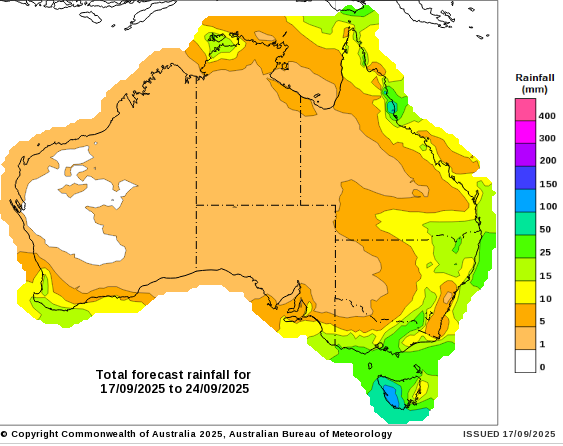

8 day forecast to 24 September 2025

http://www.bom.gov.au/

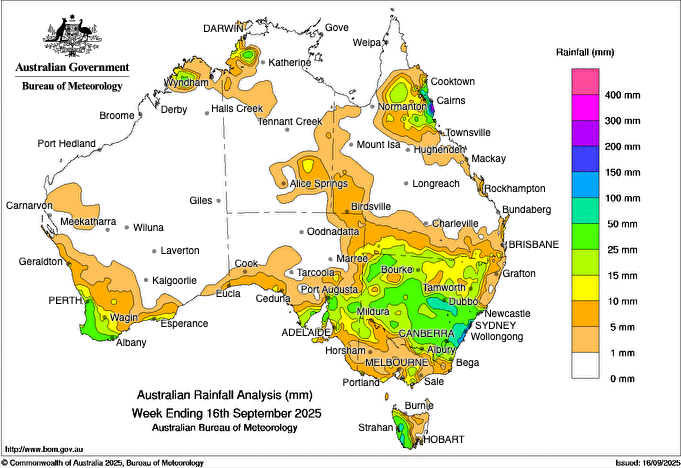

Weekly rainfall to 16 September 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar (AUD) rallied to a fresh 10-month high against the US dollar (USD) on Friday, with the AUD/USD pair reaching levels near 0.6670 during the European trading session. The surge in the Aussie comes as risk-sensitive currencies outperform against the USD buoyed by an improving global risk appetite and evolving central bank expectations. Market sentiment has turned decisively optimistic ahead of the Federal Reserve’s monetary policy decision scheduled for Wednesday. Investors are increasingly confident that the Fed is nearing the end of its tightening cycle, with growing bets on a rate cut either at the upcoming meeting or later in the year. These dovish expectations have weighed on the US dollar and provided a broad-based lift to higher-yielding currencies like the AUD.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.