Australian Crop Update – Week 37, 2025

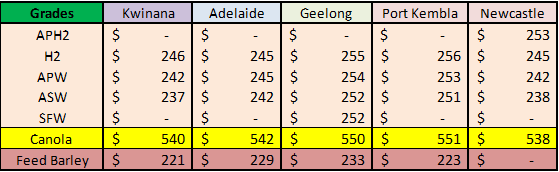

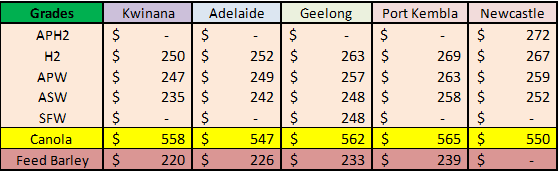

2024-25 Old Crop - USD FOB Indications

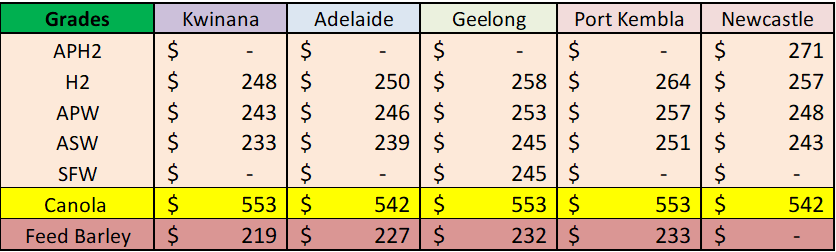

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

The Australian wheat and barley cash markets remain relatively quiet as we settle into the intercrop period between old crop executions and new crop selling. Consumers continue to be comforted by the large crop outlook here and elsewhere in the world while farmers are wondering what the trigger for an improvement in prices will be. Farmers are in no hurry to sell new crop supplies at current prices which are at best break even with production costs, although above average yields will help this equation. Many feed grain consumers have already started to build some new crop coverage and are in no hurry to extend this with talk of a potential wet harvest particularly in the east. It remains a struggle for exporters to make any nearby sales with very limited FOB stem availability. Australian wheat has been competitive into Southeast Asia, Southern Africa and the Middle East in recent weeks. This appears to have allowed for the nearby logistics to have been used up.

The ABARES forecast Australian 2025/26 barley crop of 14.6 million metric tonne (MMT) weighed on Australian prices with reports that China - who has already bought a significant number of 2025/26 cargoes - backing off their buying to $245 c&f from $250 a couple of weeks ago.

ABARES has also lifted its forecasts for Australia’s pulse crops, with lentils now seen at a record 1.7MMT, according to estimates released in its September 2025 Australian Crop Report. Lentil area is seen at a record 1.136 million hectares (MHa), 99,000ha above the record of 1.037Mha set last season. Most of Australia’s lentil crop is grown in South Australia (SA) and Victoria (VIC), and the improvement in the SA season after a rugged start has seen both area and production estimates increase substantially. In New South Wales (NSW), the estimated lentil planted area has increased by 150 percent (pc) to a record 75,000Ha, while the production estimate has tripled to 90,000 metric tonne (MT).

Australia’s chickpea crop at 2.102MMT is forecast to be the second-biggest on record after last year’s 2.267MMT harvest, and from a record planted area of 1.078MHa, just ahead of the 2024-25 planting of 1.039Mha.

The national field pea crop is seen at 220,000MT from 184,000Ha, while lupins are seen at 840,000MT from 551,000Ha, including 650,000MT from 400,000Ha expected from Western Australia (WA).

The national estimate for faba bean production has risen 26pc over the quarter to 854,000MT, mostly because of a 40pc rise for NSW, and a 25pc rise for SA, where conditions have improved considerably in the South East of the state, home to much of the SA crop.

In VIC and SA, ABARES said after a mostly dry and sporadic start to the winter-cropping season, average to above-average June and July rainfall across most regions supported crop establishment and growth.

The ABARES pulse numbers and limited consumer demand have put new crop pulses prices under pressure. This included chickpea and faba bids in the north as well as faba beans and lentils in the south. Traders were reporting some small new crop business however the tonnages were small with little momentum to generate further trade.

Australian Export Update

Australia exports reached 2.359MMT of wheat in July which was approximately the same as June. NSW and Queensland (QLD) exports were larger, and WA was down on last month. Australia has exported 19.8MMT for the Oct/Jul which is 2.2MMT more than the same time last year. Indonesia was the largest destination with 548 thousand metric tonne (KMT), followed by the Philippines with 449KMT, then Korea with 259KMT and then Vietnam 202KMT. China was only 65KMT. Australia’s 2024/25 wheat exports are now expected to exceed 23MMT from previous expectations of 22.5MMT.

Barley exports for July were 634KMT with more than 500KMT shipped from WA. China was the largest destination with 491KMT followed by Japan and Mexico with 34KMT. There was 401KMT of sorghum exported in July. This included 179KMT from Brisbane, 66KMT Mackay and 145KMT Newcastle. Canola exports were 155KMT for July.

Export Stem & Ocean Freight Market Update:

There was 476KMT of wheat added to the stem in the past week. This lifts the wheat additions in the past two weeks above 1.1MMT. NSW accounted for 202KMT of last week’s wheat additions followed by 159KMT in WA with new vessels also in VIC and SA.

The ocean freight market appears to be in a holding pattern over the last week as market participants try to ascertain if rates will continue to push or trend sideways in the near future. The Atlantic is still holding firm with a general lack of tonnage and strong exports from USG/ESCA continue to be the main contributing factors for all sizes. The strength of the Atlantic, especially from ECSA, is continuing to draw tonnage from the Indian Ocean/Southeast Asia regions on the Panamax which is helping keep rates firm in both areas. The Handysize sector in the Atlantic held steady in most loading areas however by Friday rates ex USG felt under pressure with rumours some owners were willing to consider lower than last done levels for transatlantic rounds. The Pacific Basin looks to be more balanced over the past few trading days. Reported activity has been lower than previous weeks in Southeast Asia but the fixing levels held firm while in the Fareast a steady stream of backhaul steels has helped the rates trend sideways, despite charterers best efforts to bid lower than last done.

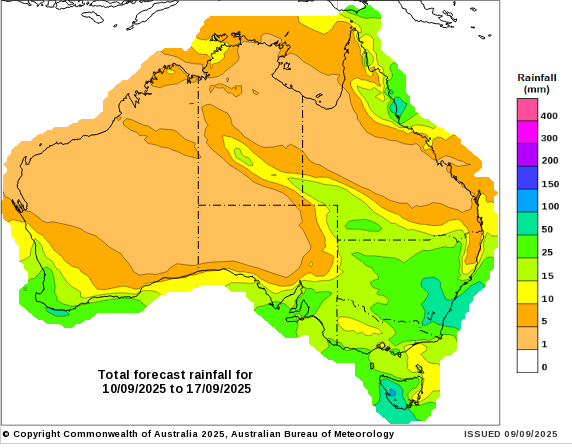

Australian Weather:

Crop conditions in Australia remain favourable to crop development. Perth had its wettest winter in more than three decades and the wet weather continues. Weather models have added widespread rain for eastern Australia over the next week. The heaviest rain over the coming week is expected to fall over southeastern Australia. The driest areas of Southern NSW are slated to see 20-40mm. Australia’s winter grain crop is big and still growing and this is comforting local and global buyers.

8 8 day forecast to 9 September 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

Last week, the AUD/USD exchange rate experienced moderate fluctuations, reflecting a cautious market environment shaped by ongoing global economic developments. The Australian dollar opened at approximately 0.6538 USD on September 1 and gained modest strength over the following two days, reaching a short-term peak near 0.6545 USD on September 3. However, this upward momentum proved short-lived, as the currency pair gradually retreated to close the week around 0.6516 USD on September 5. These movements were primarily driven by market speculation regarding potential shifts in U.S. Federal Reserve monetary policy.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.