Australian Crop Update – Week 36, 2025

2024-25 Old Crop - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

The domestic grain markets in the nearby were softer last week as good rain forced the grower to confront the old crop / new crop inverse. However, traders were reportedly more aggressive sellers into feed grain markets than milling, despite the increased optimism about crops across Australia on account of forecasts for a wet spring - particularly on the East Coast. The nearby FOB market was defined by a distinct lack of liquidity as most sellers have sold what they had and are now focused on new crop planning. That said, we are hearing some trades of barley have been made to China - and wheat - and this has kept the Western Australian (WA) markets well supported.

In general, we are rapidly entering the technical intercrop period when harvest logistics, maintenance programs and weather can play havoc with traders best laid plans. That said - Australia remains on track for a >34 million metric tonne (MMT) wheat crop in 2025/26 and a >14MMT barley crop with good August rain across most states lifting production estimates. ABARES had raised its wheat production estimates. Australia's wheat output is projected at 33.8MMT, although the production is poised to be 22% above the 10-year average. Wheat production is now seen at similar levels to FY 2023/2024. Barley, canola and pulse production was also raised. Australia’s 2025 barley crop was lifted by 1.7MMT to 14.6MMT, equal to the record crop in 2020. Australia's canola output in 2025/26 is estimated at 6.4MMT, up 1% from a year ago. Last year’s canola crop was also raised. In other crops, ABARES said Australian lentil production is forecast to rise 34% to 1.7MMT while chickpea output is likely to drop 7% to 2.1MMT.

Export Stem & Ocean Freight Market Update:

It’s been a busier week for stem additions. 690 thousand metric tonne (KMT) of wheat was added to the stem in the past week, the most in 10 weeks. This comprises 340KMT from WA and 200KMT in New South Wales. There was also a 64KMT vessel added from BNE FI and 80KMT in Victoria (VIC). Barley additions also improved with 115KMT for the week. This included 60KMT in WA and handy size ships in Pt Kembla and Geelong. Australia is on track for 22.5MMT of wheat exports for 2024/25 as well as 8.1MMT of barley and 5.4MMT of canola.

It was another positive week for shipping as all sectors gained ground, although at a slower pace than previous weeks. The Panamax sector has been well supported in the Atlantic by an abundance of fronthaul cargoes from the Americas causing tonnage to remain tight. Asia was also active, especially from Australia with a steady stream of mineral demand to help underpin the market. There also appears to be no slowing on recent gains in the Ultramax sector. The Handysize sector has followed the trend of the unit larger with the same general principles applying: increased demand in most key loading zones combined with tight tonnage supply. Another contributing factor assisting tonnage supply to remain tight in Asia is a recent spate of typhoons around the Philippines/Vietnam/South China region, causing vessel schedules to be affected.

Australian Weather:

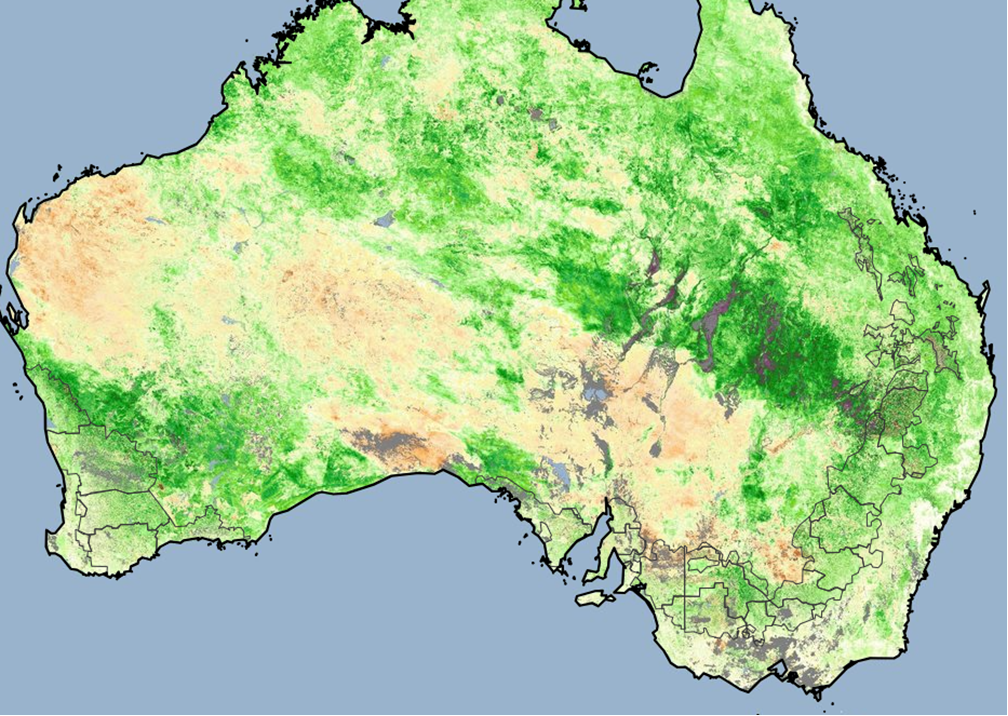

The current vegetation index continues to point towards another big wheat and barley crop in 2025/26. The rainfall averages of the Australian cropping zones have improved the NDVI ratings steadily improving through July and August following the late start. The next 10-14 days is again positive for rainfall in areas that need the additional moisture.

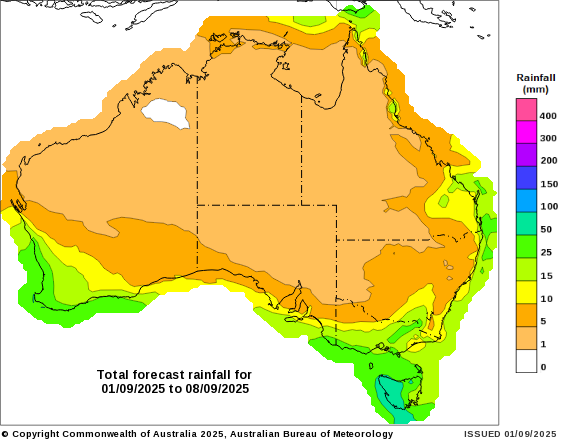

8 8 day forecast to 9 September 2025

http://www.bom.gov.au/

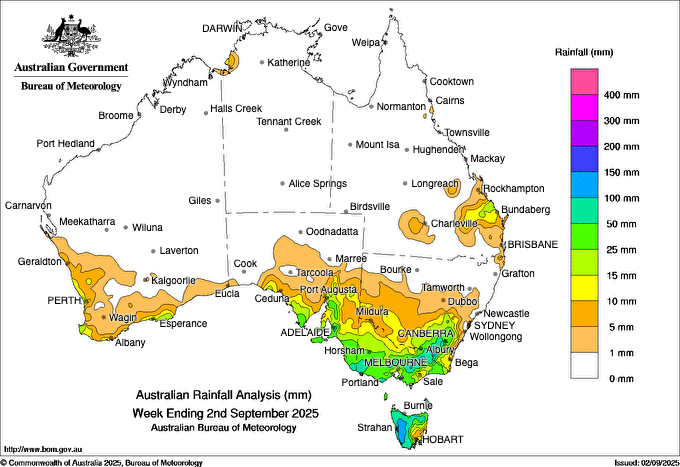

Weekly rainfall to 2 September 2025

http://www.bom.gov.au/

That said the Indian Ocean Dipole (IOD) is becoming increasingly negative and is pointing to a wet spring for much of Australia. The IOD index needs to drop below -0.4 and remain there for several weeks to be classified as a negative IOD event. The latest weekly IOD value was -0.91 on August 17, marking the fourth consecutive week below the negative IOD threshold. If the index drops below -0.94 in the coming weeks it will become the strongest negative IOD value we have seen since October 2010, which was Australia's 2nd wettest October on record and is the reason why many are being cautious about selling milling grades into new crop and are instead wanting a few feed shorts to trade around.

AUD/USD Currency Update:

Last week, the AUD/USD currency pair traded within a relatively tight range, fluctuating between approximately US$0.6462 at its lowest point and US$0.6539 at its highest. This limited range suggests a period of consolidation and cautious trading activity among investors. The Australian dollar demonstrated some resilience against the US dollar despite a mix of economic data and broader market uncertainties.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.