Australian Crop Update – Week 31, 2025

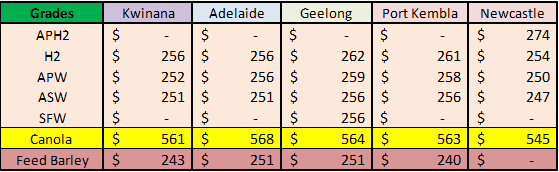

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

US wheat futures traded in a tight range last week. Northern Hemisphere harvest pressure and ample global supplies capped the upside. However, robust U.S. export demand and Russian production issues is offering underlying support. Global inputs kept with the negative theme with CBOT wheat down 1.5% for the week and the AUD creeping 0.8% higher. Australian domestic markets were sold lower last week ahead of forecast rain on Friday and the weekend. Weather models forecasted widespread rain of 20-40mm across all of Australia’s cropping regions for the past week.

Wheat bids drifted lower in all cropping zones, with some of the biggest declines seen in South East Australia where they were still holding premiums compared to northern New South Wales (NSW) and southern Queensland (QLD). Wheat bids were back UD2-5 across the country. APH13 remains well supported in the north on tight supplies and a solid export program into Asia. APH13 is now quoted USD24 per metric tonne (/MT) over APW10.5, while AH12 is only USD4/MT. New crop 2025/26 wheat bids aren’t being shown in all crop zones with most of the focus still on the 2024/25 supplies.

Barley values also came under pressure with last week’s rain with old crop feed barley was back USD2/MT. Sorghum prices in southern QLD and Northern NSW were being supported in the first half of the week on exporter short covering but tumbled when the exporter buying disappeared late in the week.

Australian New Crop Forecast 2025/26 Season:

ABARES is forecasting total winter crop plantings for 2025/26 to be modestly lower to 25.4 mill ha from 26.1 mill ha in 2024/25. Most of this is in wheat with reduced plantings in NSW as the planting rains in the western fringe wasn’t as favourable as 2024/25. Western Australia (WA) is also slightly lower.

The 2025/26 wheat production forecast is up to 30.7 million metric tonne (MMT), up from the previous 30MMT. National barley production forecast to is also higher to 13.4MMT, with most of the increase in WA. Canola production is steady at 5.6MMT. The increases have been due to slightly increased plantings rather than altered yield assumptions which are still based on historical averages.

Pulse plantings are expected to remain strong in 2025/26. ABARES has QLD and NSW edging higher (+1-2%) and holding above 1 mill ha vs the 5 year average (YA) of 570k ha. South Australia (SA) and Victoria (VIC) lentil plantings are expected to remain large. This is also about 1 mill ha vs the 5YA of 700k ha. Faba bean plantings are seen as similar to 2024/25. Oat and lupin plantings in WA are both expected increase by >10% from 2024/25 levels.

Export Stem & Ocean Freight Market Update:

It’s been a lean week for shipping stem additions. They amounted to 273 thousand metric tonne (KMT) of wheat and 154KMT of barley. WA accounted for 240KMT of the weekly wheat stem additions. WA also led the barley additions but there was also 44KMT put on in Geelong. There’s been 100KMT of barley added to the Geelong stem in the past couple of weeks.

Australian Weather:

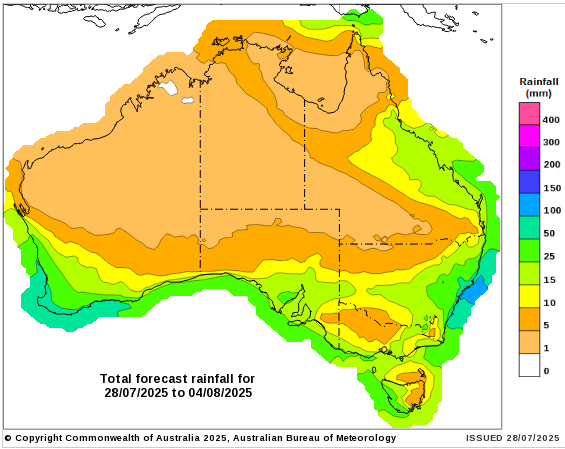

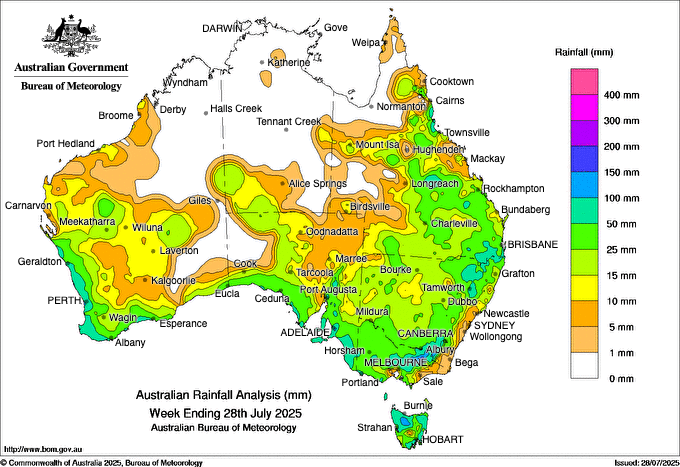

Rainfall totals were lighter across NSW last week with 15-20mm across most of the state. It was patchier in the north where some areas received rain earlier in the week as well as showers on Friday. Most areas saw 15-30mm with the heavier falls to the east. QLD received 20-30mm for the week. Last week’s rain stabilised the crops in all zones and provides confidence Australia is on track for a 30MMT wheat harvest and a 13MMT barley crop. More unsettled weather is forecast across Australia in the week ahead which is expected to see follow-up showers, particularly for NSW and SA.

8 day forecast to 4 August 2025

http://www.bom.gov.au/

Weekly rainfall to 28 July 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The AUD/USD gained approximately +0.17 % over the week, making the Australian dollar one of the modest winners among G10 currencies. The rise was supported by growing risk appetite as markets priced in improving trade sentiment and awaited key data and central bank updates. Notably, AUD/USD climbed to around 0.6619–0.6625, reaching eight month highs before pulling back slightly by the end of the week. Technically, the AUD/USD pair faces resistance around 0.6590 to 0.6687.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.