Australian Crop Update – Week 28, 2025

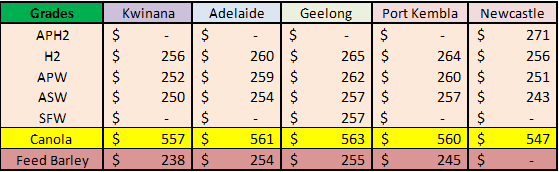

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Opening calls for US ag markets are sharply lower for the start of this week following last week’s short covering recovery on ongoing favourable weather in the US Midwest, the absence of a trade deal with China from Trump’s Iowa meeting and OPEC’s weekend announcement of a larger than expected increase in crude oil output which is expected to send crude oil lower. Sluggish demand and ample supplies continue to drive global grain markets, including Australia.

Australian domestic markets have been quiet over the past week. The absence of export demand and the focus now on the weather with local consumers covered meant very little activity. Traders were reporting some light farmer selling in the north but no avalanche of farmer selling with the new financial year. Southern markets are also steady to a tad higher where farmer selling remains reserved on the back of tighter old crop supplies and uncertainty about the new crop outlook with crops late germinated and in need a soft spring to achieve near average yields. End users are mostly comfortably covered through to spring.

Australian Export Statistics Update:

The Australian Bureau of Statistics released its May Australian grain export data late yesterday. Overall, wheat exports were similar to April but barley and canola shipments for the month were larger.

Australia’s wheat shipments for May were 2.574 million metric tonne (MMT) which is similar to April and up from the ~2.1MMT level in Feb and Mar. Western Australia (WA) accounted for 1.25MMT but New South Wales (NSW) was healthy at 539 thousand metric tonne (KMT). Indo was the largest destination with 413KMT followed by Thailand with 241KMT and then Philippines with 210KMT. China shipments fell back to 71.4KMT. Collective shipments to Africa remain historically large at 510KMT for May. Larger feed wheat shipments into Asia and increased exports to Africa are making up for the smaller shipments to China. Australia has shipped 15MMT of wheat from Oct to May. This leaves 7MMT to be shipped from June to Sep at an average rate of 1.75MMT/month. We are expecting exports of around 2.5MMT in June and then tail away to ~1.5MMT/month through Jul/Sep.

Barley exports for May jumped to 863KMT from 678KMT in April. China accounted for 774KMT or 90% of the monthly exports. This lifts Oct/May exports to ~6.1MMT.

Canola exports for May were strong at 617KMT. This lifts the Oct/May canola exports to 4.8MMT.

Export Stem & Ocean Freight Market Update:

The panamaxes market was relatively flat throughout the week, although by Friday, ECSA appeared to be gaining some ground with activity levels picking up. North Atlantic was largely uninspiring and the returns for vessel was a mixed affair depending on the delivery point and cargo as tonnage list grew faster than fresh cargoes. The Pacific, by comparison, was generally active in most areas and rates remained steady. The Supramax market was the best performer as both basins welcomed upwards pressure on all routes. The Atlantic was active from USG and ECSA while the CONT/Med regions started to get fresher enquiries by Friday. The Pacific was active from Indonesia which helped drive rates in Southeast Asia and Australia while in the Fareast, more steel demand appeared causing tonnage list to tighten. Period interest has returned with many looking for opportunities to find coverage for the remainder of 2025. The Handysize market followed a similar trend to the Panamaxes as tonnage and cargoes appeared well balanced in all regions as rates trended sideways.

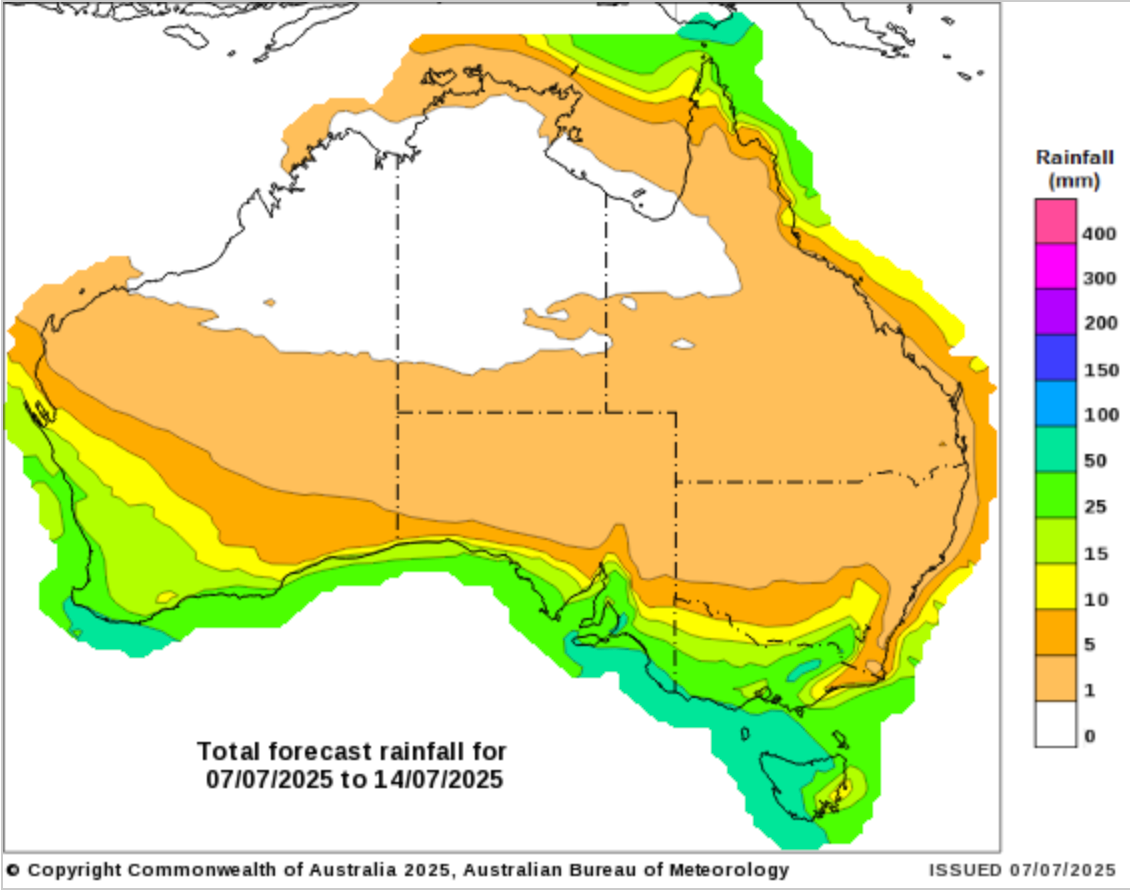

Australian Weather:

We are expecting more of the same through July where uncertain local weather is being weighed against sluggish exporter demand for Australian wheat. Australia’s wheat exports are expected to tail off in Jul/Sep as markets swing to cheaper 25/26 Black Sea supplies. Farmer selling in the south will remain slow with the crop/weather uncertainties. More light showers are expected for southern WA and southeast Australia next week but nothing significant. Northern cropping areas remain dry.

8 day forecast to 14 July 2025

http://www.bom.gov.au/

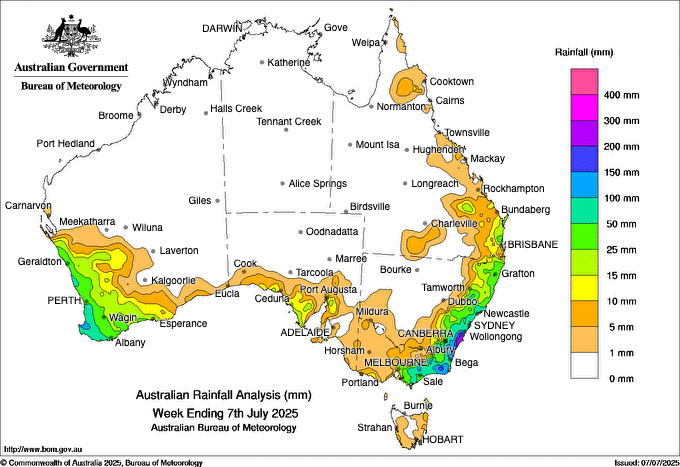

Weekly rainfall to 7 July 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar (AUD) saw a mixed, but generally upward trend, against major currencies last week. It edged up approximately 0.34% against the US dollar (USD), fluctuating between US$0.6531 and US$0.6582. Despite two prior interest rate cuts in 2025 and easing inflation, consumer confidence remains soft. Looking ahead the market is keenly focused on the RBA Board meeting scheduled for July 7-8, with the decision due. The overwhelming consensus among market economists and Australia's "big four" banks (ANZ, CBA, NAB, Westpac) is for the RBA to cut the official cash rate by 25-basis points (0.25%), lowering it from the current 3.85% to 3.60%.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.