Australian Crop Update – Week 27, 2025

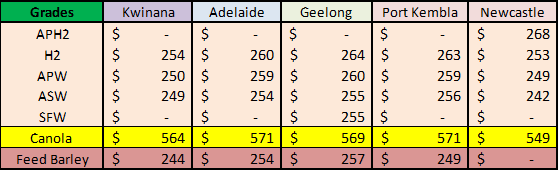

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Sharp declines in US grain markets triggered general trade selling across the Australian domestic east coast markets in the past week, sending cash markets solidly lower. US CBOT and KC wheat futures tumbled 7-8% for the week, corn futures lost 4%, while Canadian canola finished more than 6% lower. The combination of last week’s correction in the US wheat futures and beneficial follow up rain across eastern Australian cropping areas encouraged selling. Traders appear to have taken out all the old crop bids in New South Wales (NSW) and this flowed through to the Victorian (VIC) market by the end of the week. Farmer selling has improved on the improved rain through June but remains thin in all zones. Crop conditions in southern Queensland (QLD) and northern NSW remain good to excellent, but farmer selling in the old crop remains reserved with traders saying they are still having to pay higher for the odd spot loads, when needed. However, demand is limited with end users well covered and not inclined to chase more volume with the favourable outlook.

Export Stem & Ocean Freight Market Update:

A further 700 thousand metric tonne (KMT) of wheat was added to the shipping stem in the past week. This comprised 380KMT from Western Australia (WA) as well as 150KMT from NSW (120KMT Pt Kembla) with VIC, Brisbane and South Australia (SA) also chipping in. A further 120KMT of sorghum was added to the stem in the past week with 90KMT of this from QBT Brisbane after they update their stem.

An interesting week after the recent escalation then de-escalation in the Middle East. It was a wait and watch situation on Monday while the market was trying to discern how severe the short-term shock would be, however by Wednesday, with peace "restored" to the volatile region, the activity levels gained pace and hire rates started to push.

The Panamaxes gained ground across both basins with steady demand coming from most major loading areas and the overall index gained circa 1300 points over the week.

The Supramax sector was a mixed bag as the USG market showed signs of contraction after a few strong weeks, ECSA remained steady, while in the Asian area fresh demand from Indonesia and Nopac helped placed upwards pressure on rates. By end of week, available tonnage was shrinking causing charterers to chase wider than anticipated to found coverage.

The Handysize market has been more stable than its bigger cousins. The Atlantic was active from ECSA, USG, USEC while the Cont, Med regions were quiet. The Pacific was generally active across most areas causing rates to push circa 1-1.5kpd week-on-week for standard rounds while short period rates have pushed back above 13k for nice modern large handies (after slipping in the 12k's for a few week).

Bunkers appear to have settle back close to the levels prior to the Middle East conflict.

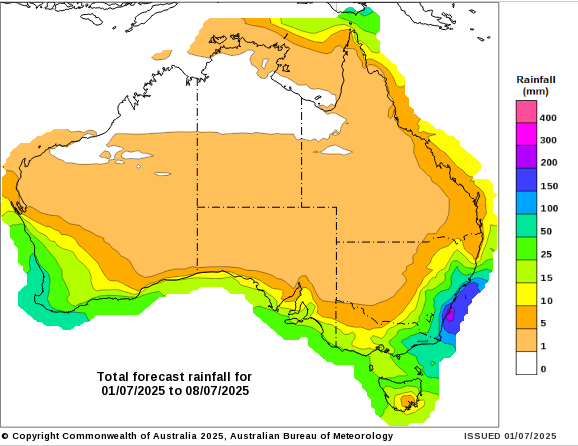

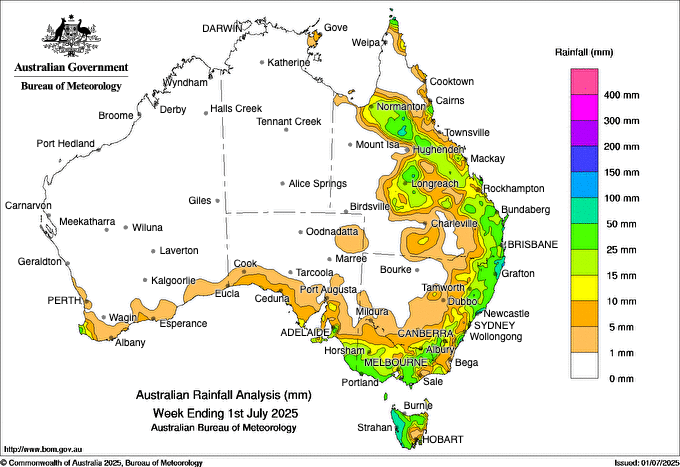

Australian Weather:

Southeastern Australia received widespread showers over the past week associated with the deep low in the bight and southerly front moving across the regions. Parts of SA received better than expected rains although the rain struggled to penetrate far inland. There was 10-20mm across the VIC, and NSW also benefited from follow up rain. Rainfall in southern NSW was at the upper end of the model forecasts with 15-20mm across the state. The week ahead appears more coastal with a large cold front expected to hit the east coast on Tuesday which should push inland to cropping regions.

8 day forecast to 8 July 2025

http://www.bom.gov.au/

Weekly rainfall to 1 July 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

The Australian dollar traded within a narrow range on Friday, holding onto gains won Thursday, consolidating its recovery back above US$0.65. Having pierced through US$0.6550 on Thursday after the USD DXY index hit its lowest level in over 3 years the AUD settled into a 50-point range bouncing between US$0.6510 and US$0.6560 closing the day a quarter percent lower at US$0.6530. Renewed trade threats prompted whippy price action with details of a US/China trade framework helping add a floor beneath the AUD while the abrupt termination of trade discussions between the US and Canada ensured uncertainty and risk aversion remained in play. The AUD outperformed the Canadian dollar after President Trump terminated trade talks in response to Canada’s plan to implement a digital services tax. Trade and geo-political tensions continue to dominate direction while China PMI numbers and commentary from Fed policy makers dominate the macro ticket.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.