Australian Crop Update – Week 24, 2025

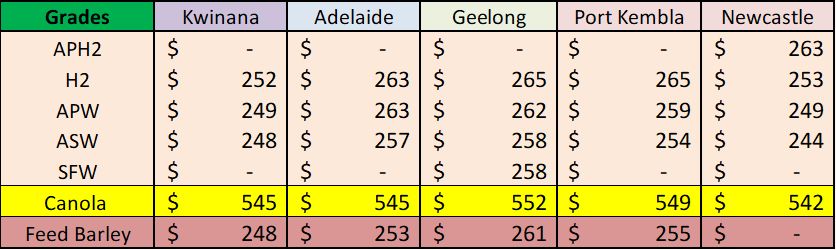

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Australian domestic markets were softer last week ahead of forecast rain across South East Australia. The local markets have seen some selling following the late May rain in Southern New South Wales (NSW) and improving weather outlook in Victoria (VIC) and South Australia (SA) and we expect this to accelerate into the new financial year in July. Candidly lack lustre global demand and favourable Northern Hemisphere production forecasts should weigh on Australia’s grain exports in the July-September quarter. Australian milling wheat is losing ground to competitive offers from Black Sea suppliers. A large carry out will develop if exports do not pick up before the end of September.

Australian 2025/2026 Production Update:

ABARES issued its June crop report early last week which offered its initial 25/26 production estimates. ABARES flagged the varying crop conditions across the country with the extremely dry weather in Southern NSW, VIC and SA. This means that much of the 2025/26 winter crop has been dry sown and will require adequate and timely rainfall during June to allow for crop germination and establishment. By contrast, conditions have been favourable in Queensladn (QLD), Northern NSW and Southern Western Australia (WA), reflecting the above average early autumn rainfall.

Australia's wheat production is projected to drop 10% this year to 30.6 million metric tonne (MMT) but remain above the 10-year average, ABARES said. Barley production is forecast to fall by 3% to 12.8MMT. Canola production is projected to decline by 6% y/y to 5.7MMT. Pulse production is forecast to remain elevated with chickpea production forecast at 1.9MMT and lentils at 1.5MMT.

Export Statistics Update:

ABS also reported 2.63MMT of wheat exports in April up from 2.11MMT in March, making it the largest export month for the 24/25 season so far. This puts Australia’s Oct-24 to Apr-24 wheat shipments at 12.5MMT. Container wheat exports were 176 thousand metric tonne (KMT) in April, which was the smallest month since January.

Indonesia was the largest export destination for Apr with 395KMT followed by South Korea with 223KMT and then the Philippines with 202KMT. However, it was larger exports into Africa that allowed the additional 0.5MMT of monthly shipments in April vs the March figures. Australia’s wheat exports into Africa jumped to 570KMT vs 55KMT in March. This was the largest month of wheat exports into Africa since May 21. There was also 105KMT of durum wheat shipped to Italy in April.

Barley exports for April were 680KMT down from 830KMT in March. WA accounted for 526KMT of the April exports. China was the largest destination with 397KMT followed by Japan with 116KMT. A further 66KMT was shipped to Saudi.

Sorghum exports jumped to 464KMT in April up from 188KMT in March. This was made up of 320KMT from QLD and 102KMT from NSW but also 42KMT from WA. Canola exports for April were 563KMT down from the 904KMT in March.

Export Stem & Ocean Freight Market Update:

It was a positive week for Panamaxes in both basins off the back of more grain and minerals demand. The gains in the Pacific were less noticeable than the Atlantic but sentiment is positive. In contrast the Supramax and Handysize sector were generally flat across all regions. The Pacific remained lacklustre the whole week but with the supply and demand equation being well balanced, we are expecting a sideways trend for the short term. The Handysize continued its recent path of minimal upwards or downwards swings in both basins as it appeared it has found its equilibrium. There is little evidence or suggestion that we will experience major changes in this sector for the foreseeable future.

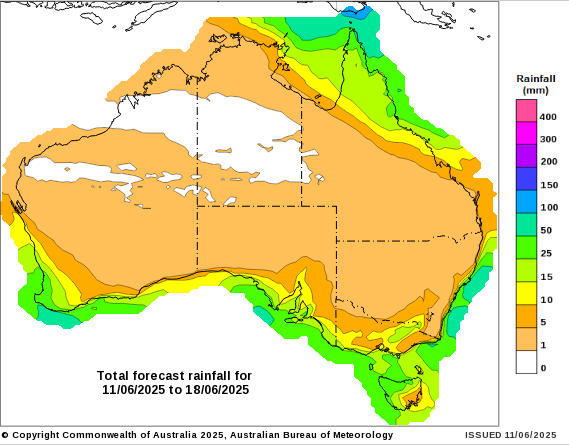

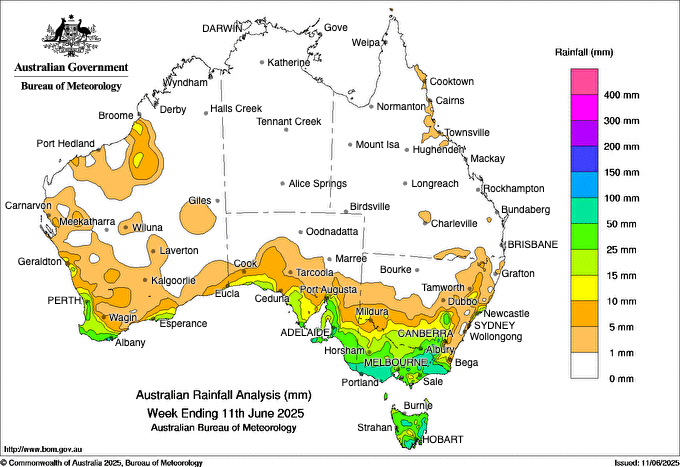

Australian Weather:

Much of Australia’s driest cropping areas received welcome rain over the past week. This included WA’s Geraldton zone as well as parts of SA and VIC. Overall, the weather models performed reasonably well with the ECMWF AIFS accurately forecasting the cropping areas totals. Last week’s rain should germinate most of the dry planted crop in SA and VIC, but more rain is needed.

WA – Most of the Geraldton zone received a general 20-60mm for the week. Last week’s rain is enough to get all of the planted WA winter crop germinated. Rainfall totals were lighter in the Kwinana zone, with the heaviest falls also closer to the coast. Most of the Great Southern received 10-15mm with the isolated areas less than 10mm. Although the rainfall totals were lighter in the Great Southern, these parts benefited from good April rain. In the Esperance zone, falls ranged from 5-20mm.

SA – Variable falls but it was probably the state’s best cropping area rainfall for several months. The Eyre Peninsula saw a general 10-15mm with some isolated areas getting 15-20mm. Isolated storms resulted in a patchy 20-40mm in the Upper North. Most of the Mid North, Yorke Peninsula and Adelaide Plains saw 10-25mm which should get >80% of the dry planted crop germinated. The Upper South East received 20-30mm.

VIC – Good falls in the southern Wimmera and Western Districts. It looks like >80% of the Wimmera received 20mm or more. The Western Districts received its best rain since September last year with a general 30-60mm across the area. The Mallee saw lighter rain, which was consistent with model projections. There was 10-15mm in the southern Mallee and 8-15mm across the northern Mallee. There appeared to be around 15mm across most of the central Vic cropping areas

NSW – there was also some patchy rain across NSW. This included 20-30mm in central west around Nyngan, Nevertire, Trangie, Dubbo, Peak Hill and Pakes. Walgett also picked up 17mm, but the rest of the north west received limited rain. Areas around Wagga, Henty, Corowa and Yarrawonga also saw 20-30mm.

8 day forecast to 18 June 2025

http://www.bom.gov.au/

Weekly rainfall to 11 June 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

Having edged back below US$0.65 on Friday evening after US Non-farm payroll data printed marginally ahead of market expectation the AUD started the new week trading between US$0.6490- US$0.6510. US/China trade talks absorbed much of the markets attentions as key officials met in London. While it was unable to extend toward last week’s 2025 high it has held onto gains above US$0.65 leading into this week’s open.

In the longer term, many analysts feel the various Trump Administrations policies could act to constrain US growth and/or dampen investor confidence in holding US financial assets. In time, we think this may see the USD steadily weaken, and this can help the AUD trend higher over the coming year. Certainly, a move back over 70 is being spoken about which is not going to help the Australian farmer churn through carry out and a 30 million plus new crop wheat harvest. Also helpful for the AUD’s longer-term outlook are steps being taken by authorities in China to boost domestic activity, particularly commodity intensive infrastructure investment. As is the resilience of the Australian jobs market and core inflation dynamics.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.