Australian Crop Update – Week 25, 2025

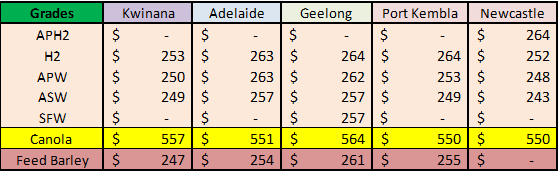

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

It’s been a quieter week for the Australian domestic markets following last weekend’s belated weather break in South Australia (SA) and Victoria (VIC). East Coast prices have pressed lower over the past week under farmer and trade selling in the north, and trade selling the south. East Coast wheat and barley bids were generally down $2-3 per metric tonne (/MT) this week. While there are plenty of sellers, buyers have now become hard to find on the domestic and export side of the trade. Feed Lots and consumers are generally well-covered for nearby needs and are in no hurry to extend purchases further having positioned with new crop coverage through the week. Exporters remain hesitant buyers with the lack of volume demand from overseas buyers. Export sales remain difficult and there is no sign of this changing any time soon with the northern hemisphere harvest just starting where larger crops are expected in Europe, Russia and the United States.

Australian 2025/2026 Production Update:

Drought across South East Australia has been influencing domestic grain and fodder markets across the entire east coast over the past three months. Last week’s rain in SA and VIC has sapped the market weather urgency for the 2025 winter crop although it does little to ease the nearby fodder shortages other than offer a green tinge to the pastures through winter. However, it does change the sentiment. Traders will be less inclined to trade the old crop from the long side now that farmers have received rain and are more likely to revert to a more neutral position as they wait and see how the winter wheat evolves. Farmers are also more likely to release old crop grain supplies now that it has rained. The rain will germinate fodder, cereal, canola and legume crops across VIC and SA. These areas need good rainfall across the winter as well as a favourable spring weather to achieve average yields. Nonetheless, the immediate goal of timely planting rains to germinate crops by mid-June looks to be accomplished. New crop prices across southeastern Australia will still have weather premiums over other regions because of the absence of soil moisture which leaves these crops more exposed to the spring weather.

Export Stem & Ocean Freight Market Update:

There was 460 thousand metric tonne (KMT) of wheat, 95KMT of barley, 110KMT of canola as 60KMT of sorghum added to the stem in the past week. Most of the wheat was added in Western Australia (WA) with New South Wales (NSW) contributing 166KMT (most in the Port Kembla zone). WA accounted for all of the weekly barley and canola additions.

The Panamaxes have continued to gain ground, buoyed by the underlying stability of grain volumes coming from US and ECSA. Combined with a tight tonnage count in the Atlantic, the sentiment remains bullish in the Atlantic for the short term. The Pacific achieved more moderate gains compared to the Atlantic but more mineral demand appearing has caused the indexes to turn green.

It’s a tale of two stories in the Supramax sector. We are seeing strong growth in the Atlantic, again off the back of steady demand from US and ECSA. While in the Pacific a hint of softness has creeped into the sentiment as charterers begin to bid lower than last done levels with a lack of fresh cargoes appearing in the market to counteract the growing tonnage count.

The Handysize market has generally been trending sideways in both basins with the general feeling of being well balanced. The Australian market appears to be a tad quieter with the usual end of financial year rush ending.

Looking forward, the main area for concern is the Israeli-Iran conflict and trying to discern what the flow on effect will be. We have already witnessed a spike in bunkers prices (circa USD 40-50/MT in most main bunkering ports) and a growing list of owners wanting to avoid sending vessels to Persian Gulf ports.

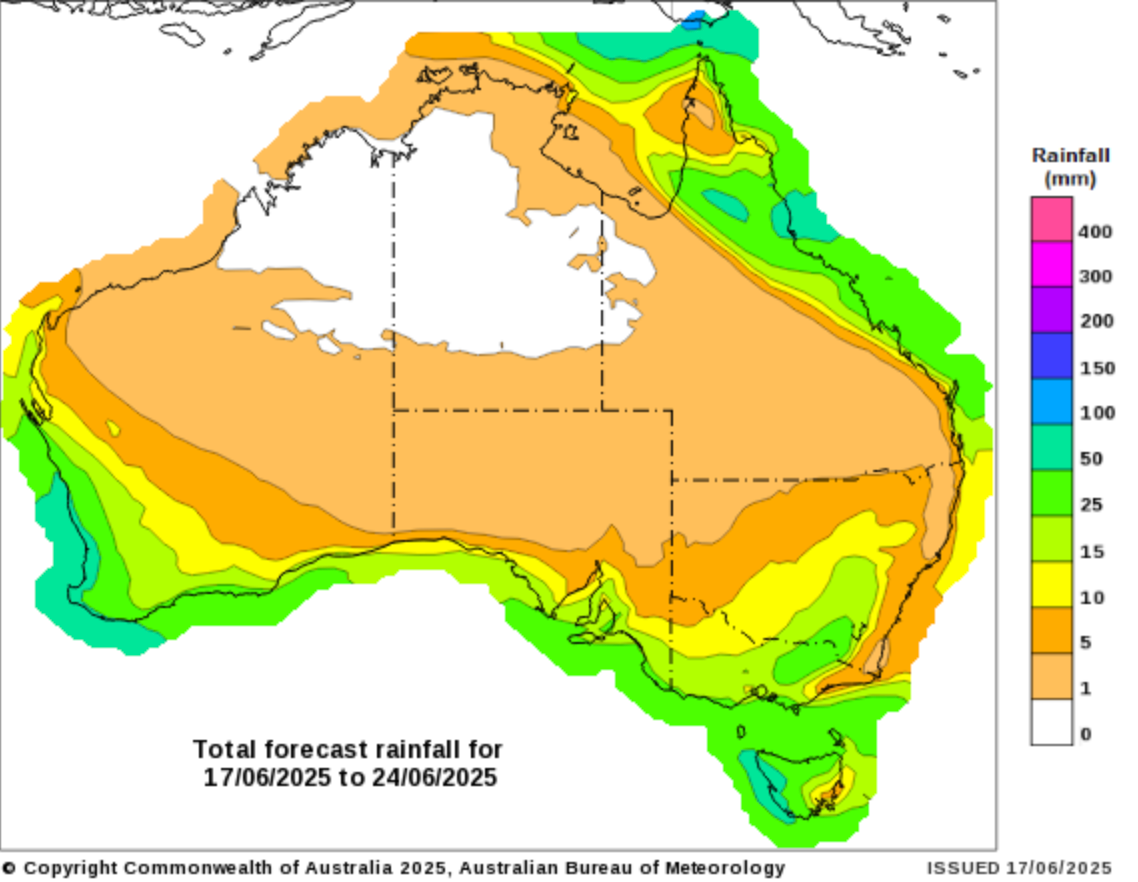

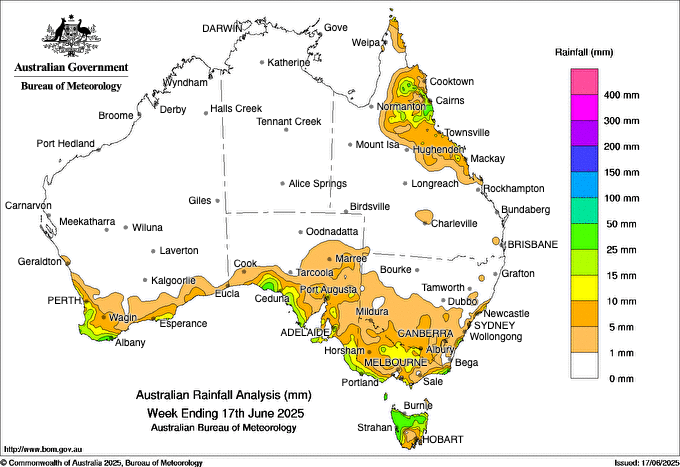

Australian Weather:

Southern markets have been comforted by last week’s rain but weather risks for southeastern Australia remain elevated. Nearby forecasts are mostly dry apart from some traces. Areas closest to the coast are in line to pick up more showers over the next week but the major cropping regions are not forecast to see much rain. The Australian Bureau of Meteorology’s extended weather model points to drier than normal conditions for VIC and most of WA’s cropping areas in July. This offers for more difficult markets. Subsoil moisture reserves are below average across much of WA and Southeastern Australia whereby farmers will remain reluctant sellers.

8 day forecast to 24 June 2025

http://www.bom.gov.au/

Weekly rainfall to 17 June 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

Last week, the Australian dollar (AUD) experienced notable volatility against the US dollar (USD), primarily influenced by escalating geopolitical tensions and shifting investor sentiment. The AUD/USD exchange rate closed at 0.6487, marking a 0.7% decline from the previous day. This drop was attributed to a surge in demand for safe-haven assets following Israeli airstrikes on Iranian nuclear facilities, which heightened global geopolitical risks. According to UOB Group's FX analysts, the AUD/USD pair is currently trading within a range between 0.6430 and 0.6550. The major support level is identified at 0.6430, suggesting limited downside risk in the near term. The outlook for this week’s analysts suggests that the AUD/USD pair may continue to trade within the established range, with geopolitical developments and central bank policies being key factors to watch in the coming weeks.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.