Australian Crop Update – Week 23, 2025

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

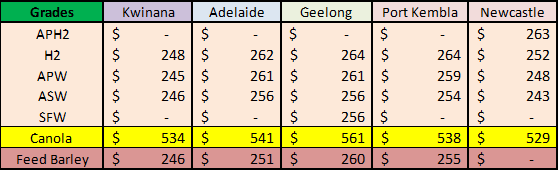

Australian domestic markets were sold lower by farmers and traders following last week’s soaking across Southern New South Wales (NSW) and some more patchy rain in Victoria (VIC) and South Australia (SA). Weaker global inputs also added to last week’s domestic sell off with US and French wheat futures under pressure. Black Sea cash markets also weaker as we approach northern hemisphere new crop.

That said traded volumes were thin and exporters are standing back with domestic end users having already built coverage. Last week’s sell down puts the nominal Newcastle APW at $248 FOB which on a CFR equivalent is in the low $270’s into SE Asia vs PNW HRW 11.5 in the high $260’s CFR and new crop Black Sea wheat in the low $260’s. Last week’s selloff has improved the export competitiveness for Northern NSW, but it’s still more expensive that other competition.

For the time being, Australian wheat values across the zones remain a function of heavy old crop supplies in Queensland, Northern NSW and Western Australia (WA), sluggish export demand and dry weather across south east Australia and some areas of WA, which are casting doubts over the size of the 2025/26 crop.

According to ABARES, Australia's wheat production is projected to drop 10% this year to 30.6 million metric tonne (MMT) but remain above the 10-year average. Barley production is forecast to fall by 3% to 12.8MMT. Canola production is projected to decline by 6% year on year to 5.7MMT. Pulse production is forecast to remain elevated with chickpea production forecast at 1.9MMT and lentils at 1.5MMT. ABARES flagged the varying crop conditions across the country with the extremely dry weather in southern NSW, VIC and SA. This means that much of the 2025/26 winter crop has been dry sown and will require adequate and timely rainfall during June to allow for crop germination and establishment, they said. By contrast, conditions have been favourable in QLD, Northern NSW and Southern WA, reflecting the above average early autumn rainfall.

Longer term weather models are now looking at a possible negative IOD developing in the winter. Warm sea surface temperatures near Indonesia are expected to heat up further over winter, possibly triggering a negative Indian Ocean Dipole (IOD) event. The IOD is an index that measures the difference in sea surface temperatures across the equatorial Indian Ocean. IOD events typically occur between May and November and break down when the monsoon moves over Indonesia in late spring or early summer. They are typically associated with increased moisture to the north west of Australia which offers more rain across central and eastern Australia as well.

Export Stem & Ocean Freight Market Update:

There was 542 thousand metric tonne (KMT) of wheat and barley added to the stem in the past week.

ABS wheat exports to March and stem to June put exports at 17.2MMT which is 78% of our forecast 22MMT. Using the same analysis, barley exports are already 94% complete. Wheat exports seasonally decline from July onward as the northern hemisphere new crop competition is felt.

Negativity has seeped into the Panamax and Supramax sector as rates faced downward pressure in both basins all week. As tonnage supply grew in both markets, fresh cargo inquiry failed to keep pace and charterers were bidding below last done levels with owners having no other choice but to accept if they needed coverage. A possible positive from the previous week was that we didn’t witness a steep decline in rates, rather a gentle easing. Looking forward, despite the recent swings across the different size sectors, the market is still indicating a fairly flat and well-balanced market for the remainder of 2025.

Australian Weather:

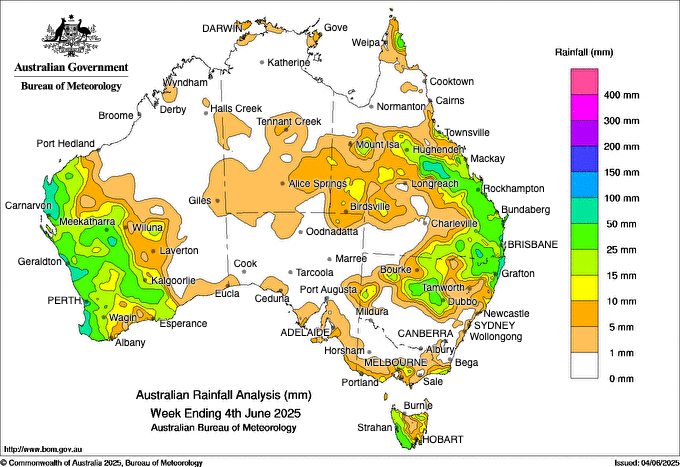

WA saw rain later last week (Thu/Fri) receiving 15-30mm. WA is expected to see more showers in the week ahead as a slow-moving low passes over southern WA on the weekend and early next week offering lingering showers across the cropping areas.

Dry weather remains a concern for SA and VIC where most of the crops have been planted dry but are awaiting rain to germinate. This week will be mostly dry with some possible showers later in the week. The late start and dry sub soil moisture reserves mean these areas will be at significantly higher risk of below average yields.

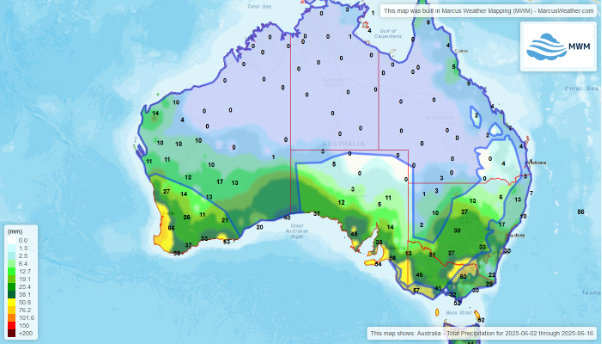

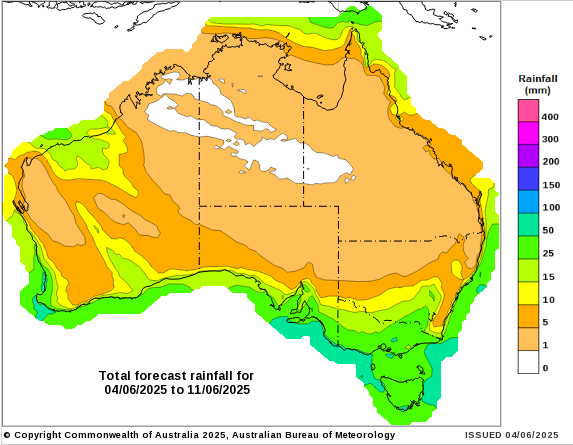

8 day forecast to 11 June 2025

http://www.bom.gov.au/

Weekly rainfall to 4 June 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

Over the past week the Australian dollar (AUD) experienced a modest appreciation against the US dollar (USD). The USD faced downward pressure due to concerns over US fiscal stability, including a sovereign credit downgrade and trade tensions with the European Union. On the local front the Reserve Bank of Australia (RBA) reduced the official cash rate by 25 basis points to 3.85%. Despite this dovish move, the AUD held steady, supported by expectations of further rate cuts and a softer inflation outlook. Looking ahead this week the AUD/USD pair is expected to continue trading within a tight range, influenced by upcoming economic data releases and global market developments.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.