Australian Crop Update – Week 22, 2025

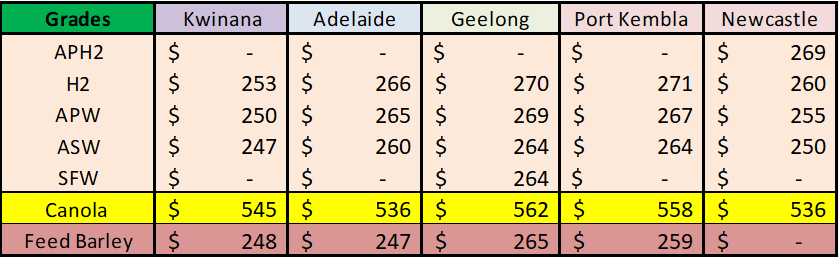

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

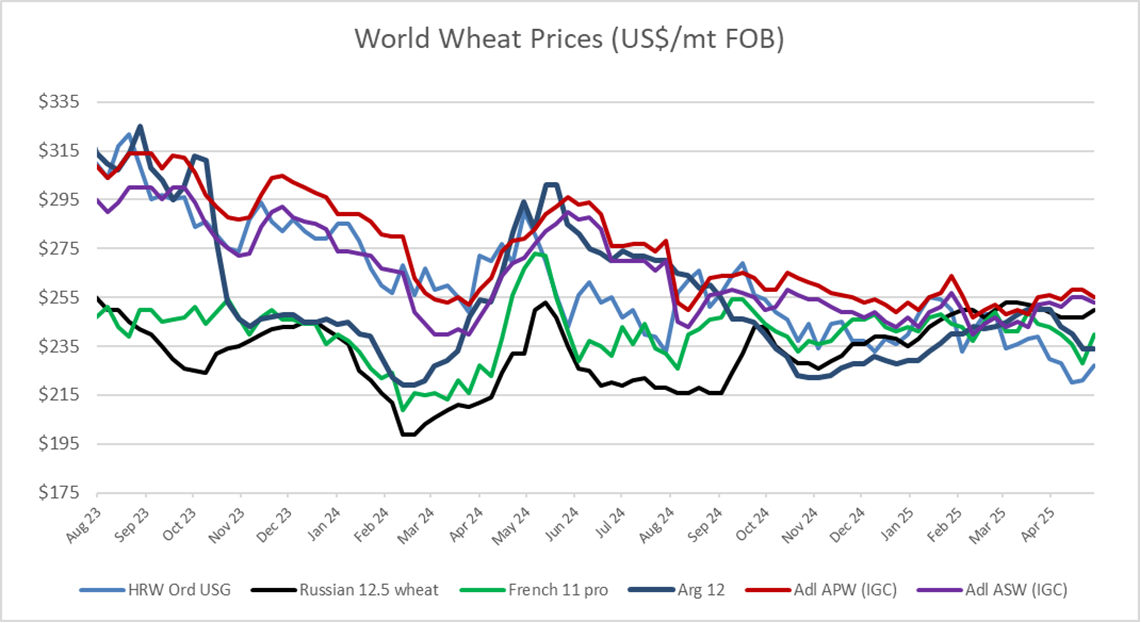

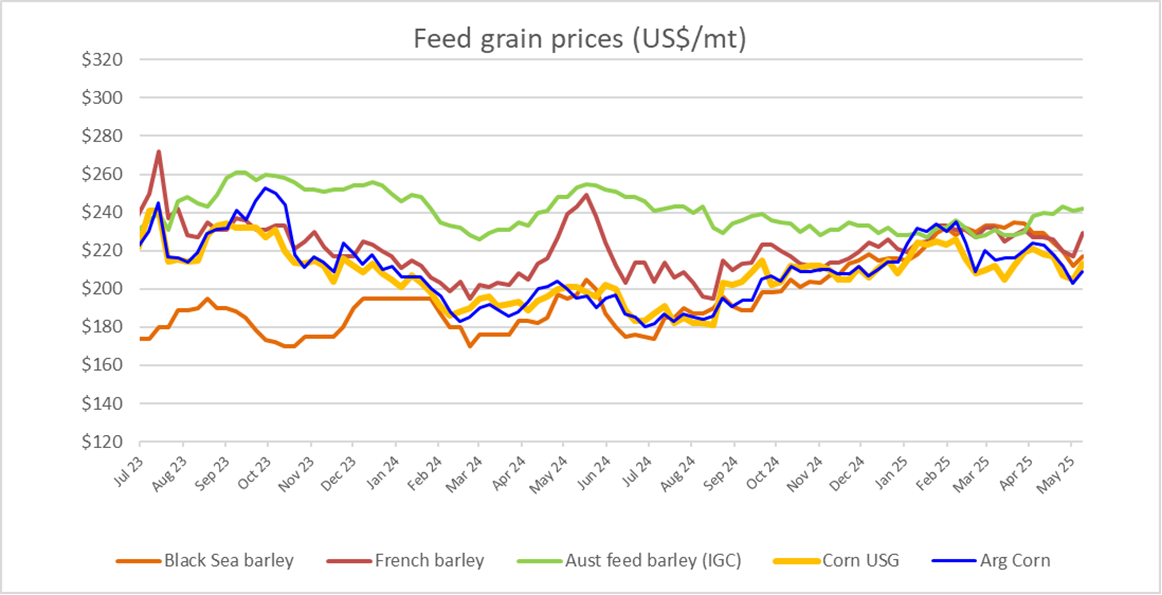

Australian Grains Market Update

Rain in New South Wales (NSW) and more general rain in the forecast for this week and into June resulted in a flurry of activity in the Australian domestic grain markets over the last week. Wheat and barley sellers emerged which put some pressure on prices particularly for those slots that are starting to compete with northern hemisphere new crop positions. The changes in price were relatively small as the strength of the AUD took out some of the benefit.

How much rain South Eastern (SE) Australia will see in the next couple of weeks will be important. At best, SE Australia will see its autumn break at the start of winter. At worst they could be still waiting for enough rain to germinate dry planted crop. Areas will need at least >20mm to germinate dry planted crops. New crop markets will react once/if this is received to the downside for wheat, barley, canola and pulses.

Export Stem & Ocean Freight Market Update:

There was 518 thousand metric tonne (KMT) of wheat added to the stem in the past week. All of this was in Western Australia (WA). It included 268KMT in Kwinana, 150KMT in Geraldton and 50KMT each in Esperance and Bunbury. There was also 300KMT of barley put on the stem in the past week with 195KMT of this in WA as well as individual cargoes in South Australia (SA) and Victoria (VIC). A further 51KMT of canola was put on the stem in VIC.

In general, the ocean freight markets were stable over the last week. The Pacific was more active in the early part of the week with demand appearing from Australia and North Pacific. However, by Friday, a softer feel had started to seep through with fresh enquiry starting to dry up. For the most, Supra/Ultra sector was fairly stable throughout the whole week with a general feeling the cargo/tonnage equation is well balanced. The Indian Ocean had continued to deliver strong returns for Owners with tonnage said to be scarce causing Charterers to pay up. Demand/cargo volume has been stable in the Handysize sector.

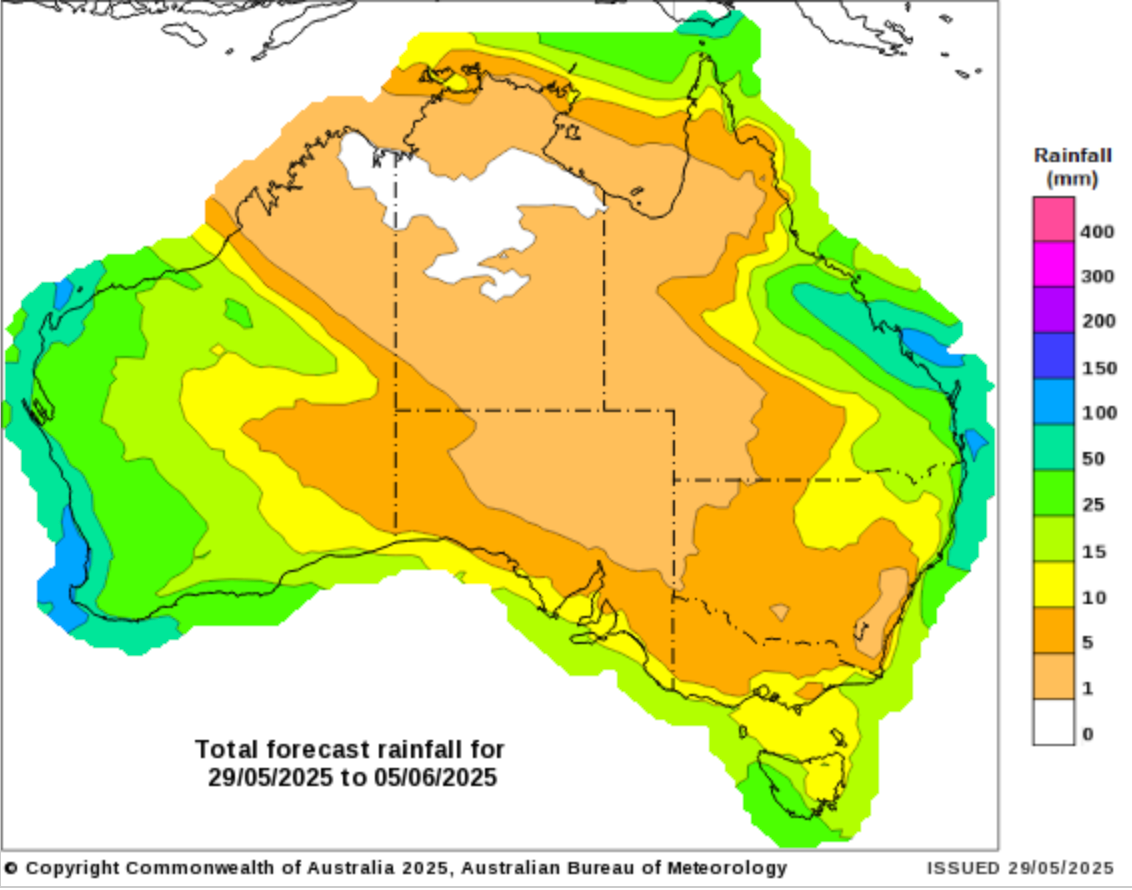

Australian Weather:

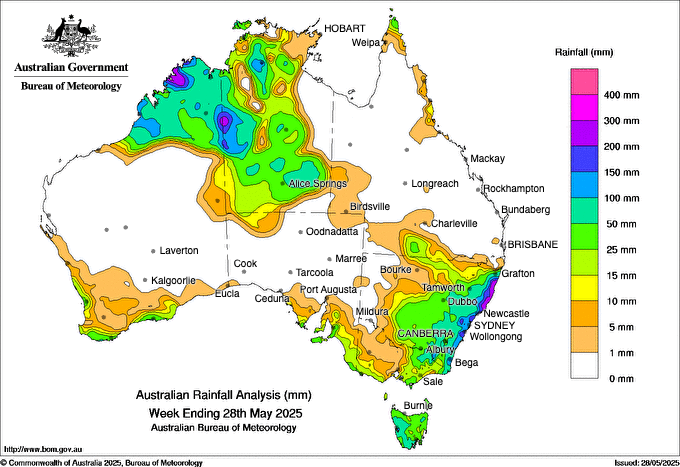

Southern NSW received welcome rain in the past week and Adelaide and the Hills also received good amounts of rain (the best in nine months) with most of the rest of SA receiving around 10-14 mm. Tropical moisture is building across northern WA, and this pattern will influence the weather across much of Australia throughout the week. This is expected to see more rain in Queensland (QLD) and NSW through the week. Southern WA will see a cold front later in the week which is expected to result in cropping areas showers on the weekend. The big question is how much rain SE Australia will see. Weather models aren’t forecasting any significant rain for SA and VIC cropping areas this week but are offering a better chance in the following week and into June. The model accuracy is significantly lower the further out we go. The good news for southern Australia is the lows are now hitting the mainland, whereas before they have been much further south in the Southern Ocean.

8 day forecast to 5 June 2025

http://www.bom.gov.au/

Weekly rainfall to 28 May 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

Over the past week, the Australian dollar (AUD) experienced a modest appreciation against the US dollar (USD), reflecting a broader trend of USD weakness driven by softer-than-expected US economic data and shifting expectations around Federal Reserve interest rate cuts. The upside faces strong resistance from a descending trendline and the 0.6500 psychological barrier, a level that has repeatedly capped gains this month. At the same time, the AUD is drawing additional strength from encouraging signals on the global trade front. China’s Foreign Ministry confirmed that Beijing and Washington have agreed to maintain open communication channels following a high-level diplomatic exchange. Local Markets are betting on further interest rate cuts to come, after the Reserve Bank took the knife to the cash rate at its May meeting.

A burst of trade and economic optimism washed through markets overnight with US traders back on deck after their long-weekend break. The mood music around US/EU trade relations was positive. Following on from the weekend announcement that the US had extended the EU tariff deadline to 9 July markets were buoyed by President Trump’s social media post stating the “EU has called to quickly establish meeting dates”.

The uptick in the USD on the back of the more positive expectations about a US/EU trade deal and outperformance of US financial markets has exerted a bit of downward pressure on the AUD and NZD over the past 24hrs.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.