Australian Crop Update – Week 21, 2025

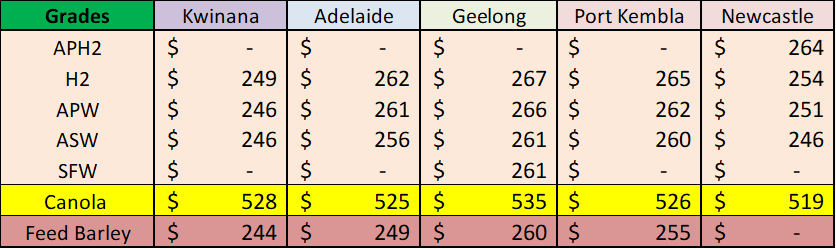

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Global markets inputs were little changed last week. US wheat futures ended little changed with corn edging lower with the favourable weather. US wheat tried to rally through the week from lows, but sellers soon emerged on big winter wheat crop expectations and cheap Black Sea new crop offers. The AUD/USD was modestly lower.

The Australian domestic markets for protein in the east and south have widened in the past week with the north a tad softer while southern markets strengthened on dry weather and domestic shorts. There appears to have been some increased farmer selling in New South Wales (NSW) but sellers remain scarce further south. Victoria (VIC) and South Australia (SA) markets were firmer. VIC barley was up USD 2-8 per metric tonne (/MT) for the week and wheat up ISD3-6/MT. Faba Beans for feeding were also up USD 8-12/MT. It’s a challenging market with domestic shorts and slow farmer selling pushing values higher to generate new export demand with old crop values tracking higher. SA is heading into a drought market with wheat and barley USD10/MT over east and west coast values now.

Australian wheat is currently quoted at $255-258 FOB while new crop Russian 12.5 is indicatively quoted at $225 FOB. This puts Black Sea wheat into Asia at ~$260 CFR vs Australian at >$275. New crop Black Sea barley is also being offered much cheaper than Australian. China reportedly bought 400 thousand metric tonnes (KMT) plus of French / Ukrainian at $250-254 CFR vs old crop Australian at $241 FOB.

Australian Export Statistics Update:

Australia exported 838,793 metric tonnes (MT) of barley and 208,907MT of sorghum, with China the leading destination by far for malting and feed barley, as well as sorghum, according to the latest data from the Australian Bureau of Statistics. Malting barley exports at 206,248MT more than doubled from the 87,635MT shipped in February, with China accounting for 152,265MT, Vietnam 25,477MT, and Peru 22,000MT.

Feed barley, March volume at 632,545MT dropped 29 percent from the 889,689MT shipped in February, with China the destination for 561,903MT, followed by Saudi Arabia on 55,730MT, and Vietnam on 3267MT.

Sorghum exports continued their annual climb to reflect new-crop availability, with the March being close to double the 106,298MT shipped in February. Behind China on 166,973MT, Kenya on 29,998MT, and Taiwan on 7994MT were the major destinations.

Export Stem & Ocean Freight Market Update:

There was 837KMT of wheat additions on the stem in the past week making it the largest week in nine weeks. Western Australia (WA) accounted for nearly 400KMT and NSW close to 300KMT. The other states chipped in with smaller volumes. A further 186KMT of barley was put on the stem in the past week, with all but 10KMT of this coming from WA. There was also 55KMT of sorghum added to the stem in Newcastle NAT.

Strong wheat additions in the past week confirms the strengthening in Australian wheat shipments through April and May. We expect this will continue into June and into July. The understanding is that exporters have been working hard to increase export sales over the past couple of months with sharp prices, and this is now showing on the shipping stem. The stem is pointing to May wheat shipments of ~2.7 million metric tonne (MMT) up from ~2.3MMT in April. However, buyers will have little appetite for Australian wheat beyond June when cheaper Black Sea become available.

An overall lacklustre week for the drybulk shipping market that was interrupted with holidays and various shipping events around the globe. For the most part, the market was trending sideways on all sizes with a possible hint of softness creeping in by Friday, which is usual after a couple of days of low activity.

The Panamaxes in the Atlantic faced pressure by midweek as demand couldn’t keep the same pace as growing tonnage count causing rates to contract slightly, while in the Pacific support was found with Australian exports increasing but Nopac and Indonesia were noticeably quiet.

The Supra/Ultra's were generally quiet in both basins and became a very positional market with vastly different rates being heard on similar routes for similar ships. The exception was US Gulf where demand was strong throughout the week. The Handy market held stable for the most part with the overall sentiment being fairly well balanced in both basins.

Looking forward we still find the overarching outlook to be conservative for the remainder of 2025. Many operators are going short on tonnage and cargo exposure as they are not prepared to make major calls either way, instead happy to take a short term approach until the market can give clear signals of the direction.

Australian Weather:

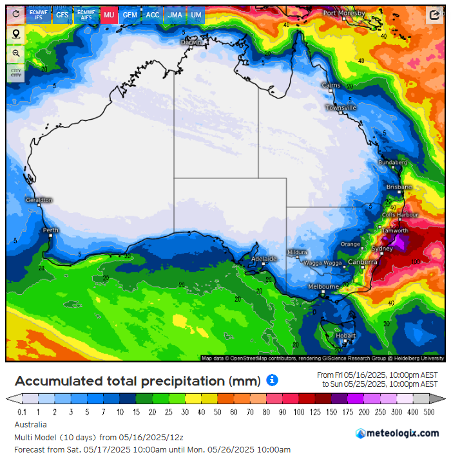

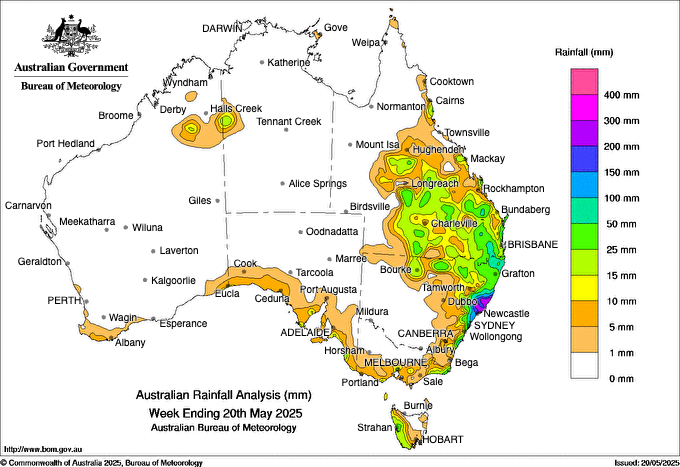

Queensland (QLD) and parts of NSW received some showers and isolated storms last week. Mid-week, recorded rainfall ranged from 15-45mm with heavier rains confined to small parts of the states. Many areas were dry planted and in need of rain to complete winter crop sowings having missed the heavier falls in early April. Forecasts remain mostly dry for Australia’s main cropping regions for the coming week. The northern cropping areas may see some lingering instability offering showers but the dominate high over the country’s south east is dominating weather patterns.

The Australian Bureau of Meteorology (BOM) released its latest climate outlook for June to September. BOM is forecasting that there is a 60-80% chance of above average rainfall for much of inland Australia. Rainfall is expected to be within the typical range for June to August for western WA, much of VIC, parts of the east coast and across the far tropical north. However, the breakdown of the BOM’s weekly and fortnightly maps shows they don’t expect the rain to start to improve until the second week in June.

8 day forecast to 27 May 2025

http://www.bom.gov.au/

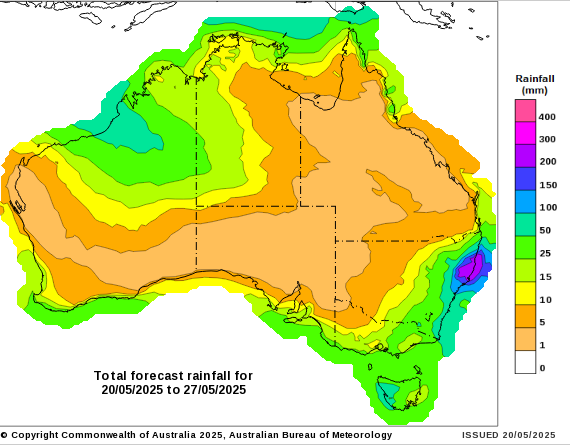

Weekly rainfall to 20 May 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

Over the past week, the Australian dollar (AUD) experienced a modest appreciation against the US dollar (USD), reflecting a broader trend of USD weakness driven by softer-than-expected US economic data and shifting expectations around Federal Reserve interest rate cuts. The AUD/USD exchange rate increased by approximately 1.09% over the week, closing at around 0.6427 on Friday, May 16. This rise was part of a broader trend where the AUD reached a weekly high of 0.6433 and a low of 0.6361, reflecting market volatility during the week. Key factors influencing this movement included weaker-than-expected US retail and producer price data, which bolstered expectations of Federal Reserve rate cuts.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.