Australian Crop Update

FOB replacement values using Australian track bid/offer – not an indication.

Harvest Progress

The 2021/22 harvest is now well underway in the northern part of the country with the first harvest loads being received in Western Australia and Queensland.

Local Weather

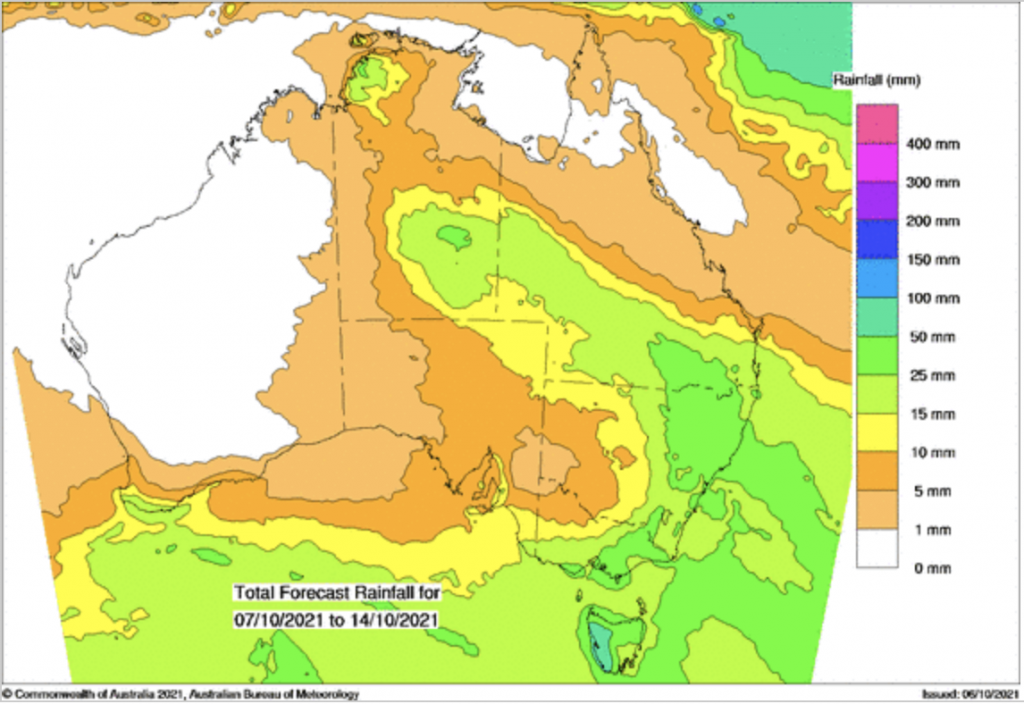

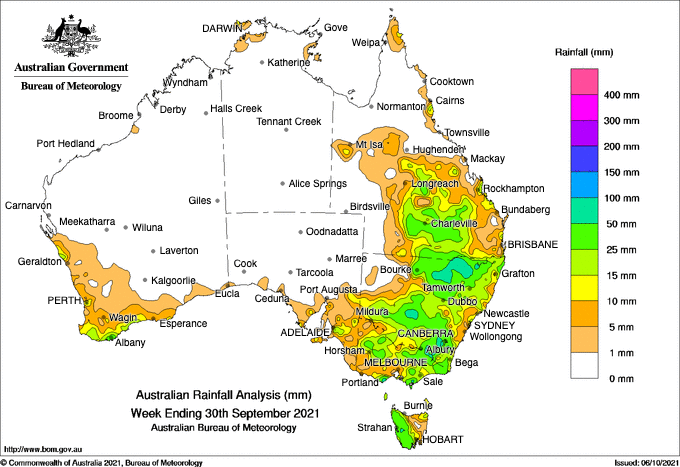

Widespread rain fell across the East Coast after an extended period of dry weather, and this was well received by crops in need of finishing rain. WA also received rain, albeit lighter and patchier. Nonetheless, it’s beneficial for finishing crops and helps limit further yield losses. Parts of South Australia also picked up handy rain, particularly through the Murray Mallee.

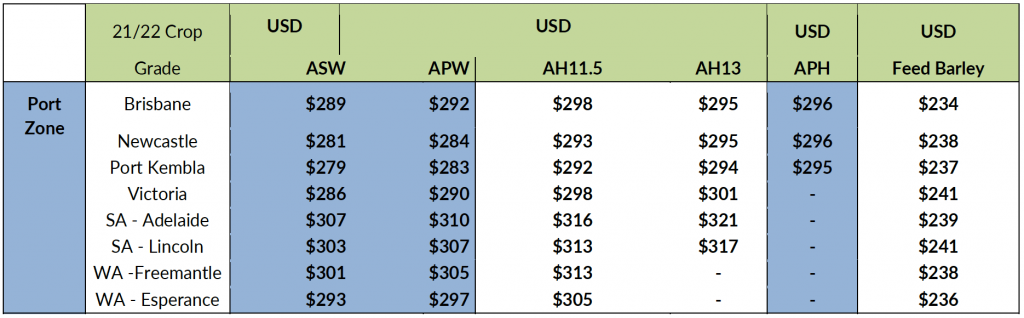

Local Grain Markets

Cash markets for the nearby have had a bid side tone for the last ten days or so with a lower Australian Dollar leading to strong export demand from bulk and container traders. The wheat market has been further supported by the USDA small grains report, which was bullish for wheat, neutral for corn and bearish for beans. Farmers are already reasonably sold on canola, but the wheat sales should crank up in the next few weeks. The biggest risk now is a wet harvest and quality downgrades. Although it is still early and the majority of the crop is still green, it is a risk nonetheless.

Supply and Demand

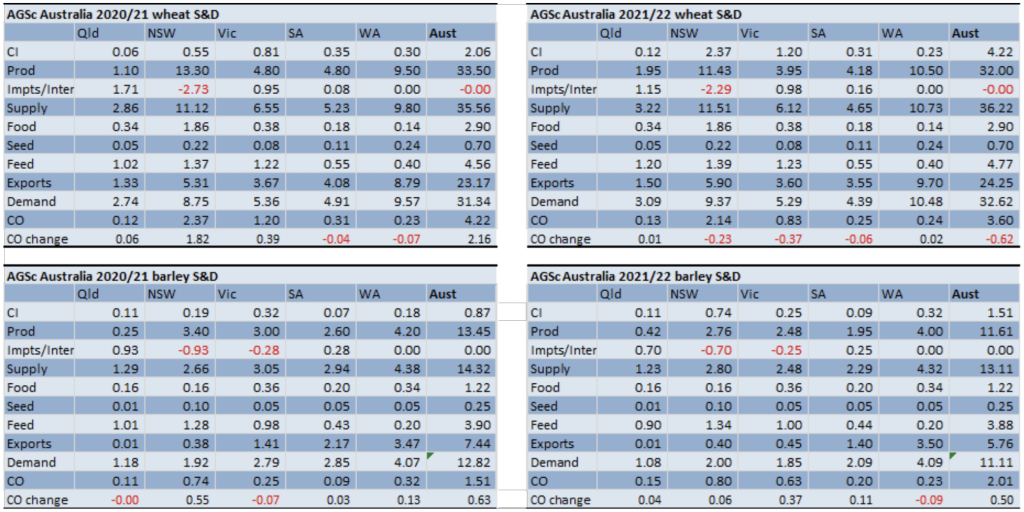

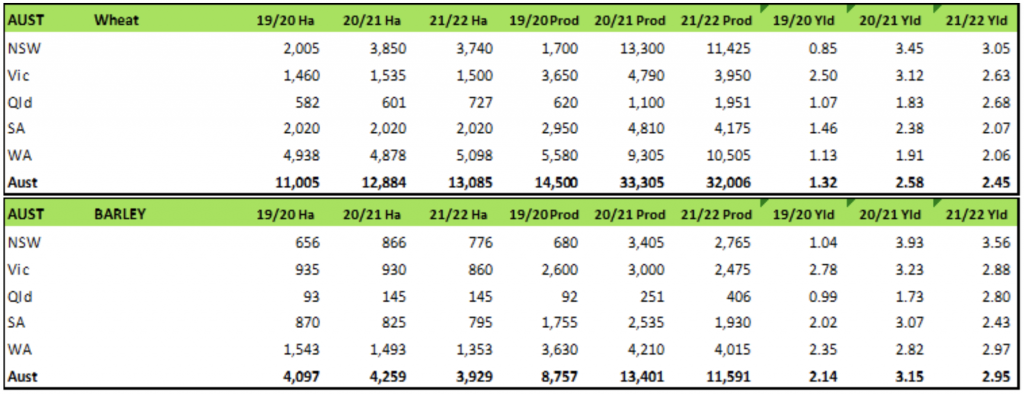

We have updated the Australian wheat and barley balance sheets increasing national wheat production to 32.0MT from the previous 31.1MT on 20/9. Australian barley production is modestly higher at 11.6MT. NSW wheat production has been raised to 11.4MT (10.75 MT previously). Domestic demand remains unchanged.

Ocean Freight – Bulk and Container

On the ocean freight front, it is hard to tell where we go to from here. There are a myriad of factors potentially pulling the markets one way or another and consequently, it feels like we are going sideways. Period numbers are consistent, and it feels like despite on-coming holidays across Asia that the markets will remain steady. Bunkers have generally firmed in line with oil prices, but again, it is hard to say where they are heading over the medium/longer term.

The Australian container market continues to struggle with logistics and container freight issues. Exporters over the past six to nine months have seen ocean freight rates rise two to three fold. They’ve also seen a disruption in services and container supply. In general, the market is challenged with freight rate validities for containers as ocean freight liners are now primarily offering container rates on a one month validity, with general rate increases across all destinations month to month. Larger exporters with supply chains and their own packing facilities have been able to leverage container lines for space and equipment.

Internationally, there are several core reasons why the container shipping industry is in disarray. COVID has been the major disruptor with consumers not only focusing more on online purchases increasing demand for smaller shipments delivered to their door, but regulations for countries have also changed in relation to testing and quarantine protocols causing delays. The Ever Given vessel disruption in the Suez Canal continues to have flown effects in relation to a backlog of containers throughout Europe causing delays and demurrage for waiting vessels to unload. There is also a lack of logistics support for rail cars and trucking supply within the United states having a major effect on the China / USA tried lanes. All of these issues coupled by a sense of profiteering by the container lines continues to disrupt the industry. Expectations are that this new norm will be in place for the next 12 to 18 months before supply chains have adjusted.

Australian Dollar

The Australian Dollar continues to be range-bound against the USD.

To receive this information directly to your inbox as soon as it’s released, sign up for our newsletter below.

The post Australian Crop Update appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.