Australian Crop Update – Week 4, 2024

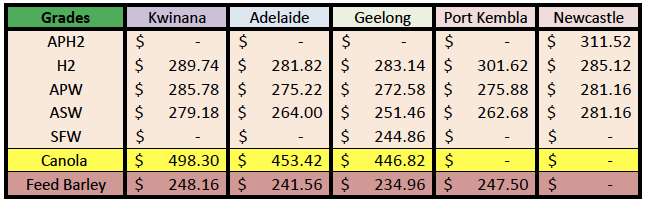

2023/2024 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

New Crop - CFR Container Indications PMT

Please note that we are still able to support you with container quotes. However, with the current Red Sea situation, container lines are changing prices often and in some cases, not quoting. Similarly with Ocean Freight we are still working through the ramifications of recent developments on flows within the region – please bear with us.

Please contact Steven Foote on steven@basiscommodities.com for specific quotes that we can work on a spot basis with the supporting container freight.

Australian Grains Market Update

Australian domestic markets were steady to softer last week across most port zones with the 1.4% drop in the Aussie dollar offering limited support. Traders have been unwilling to chase supplies unless it is against nearby shorts. Even then, the trade has been more inclined to swap stocks rather than buy outright which is keeping activity low.

Sluggish demand from China continues to cap global commodity prices. China's influence on global commodity markets can’t be overstated as they dominate global trade. This is true for ag commodities but also across the energy and mineral space. In 2023, China accounted for about 71% of the world's iron ore imports and about 58% of copper ore concentrates. They also import about 26% of the world trade in coal and 12% of the global crude imports. In ag commodities, China takes around 61% of the world's soybean imports, 87% of the sorghum and 29% of the barley. They also account for 12% of the world's corn imports and 6% of the world's wheat trade. In absolute terms, China imported about 103 million metric tonne (MMT) of soybeans in 2023 as well as around 52MMT of corn, sorghum, wheat and barley. China will remain the world's dominant commodity importer in 2024, but a slowing economy takes the shine off the import totals and investors become less willing to chase bullish stories without the backdrop of demand growth from the world's major importer.

Global wheat markets are soft and export sales are difficult to make and there is nothing on the horizon to suggest this is about to change. Australian wheat remains relatively expensive against other origins and core markets in Asia have been taking in supplies from a broad range of origins rather than paying up for Australian. Even local consumers appear to be well covered until April for feedlots and the flour mills.

There is nothing in the domestic supply and demand that suggests buyers should alter their current position of holding back from farmer purchases. Farmer selling remains reserved as well, but the absence of any significant exporter shorts, favourable local weather and sluggish global demand suggest trade buying is likely to remain lacklustre until the local prices come off.

Now that harvest is completed and estimated production data is all but fully reported, the national wheat crop for 2023/24 has been documented at 25.3MMT. Export estimates for this season are at 19.4MMT which is up on previous reports because of the need to shift wheat exports from Victoria (VIC) to avoid large carryover stocks with the bigger crop. Western Australia (WA) however has been reduced with the smaller crop. The national barley crop is 10.2MMT with exports of 6.6MMT. National canola production is 5.55MMT with exports of 4.75MMT.

Ocean Freight & Shipment Stem Update:

The Ocean freight market continues to be caught in the usual “hands off” market that proceeds the Chinese New Year. This malaise has been exacerbated by news last week that the JWC (joint war committee), a London based Insurance body placed a large area of the North West Indian Ocean in a “war zone” which makes chartering vessels and insuring cargo through the Red Sea very difficult indeed.

600 thousand metric tonne (KMT) of wheat, 120KMT of barley and 90KMT of canola were added to the stem in the past week. South Australia (SA) accounted for 343KMT of the weekly wheat additions which will give the state’s tally a boost. There was 140KMT of wheat added to the stem in WA as well as 120KMT of barley. Another 60KMT of canola was put on the NSW lineup last week as well as 30KMT of wheat. VIC wheat exports still look slow after the bigger than expected crop.

Australian Weather:

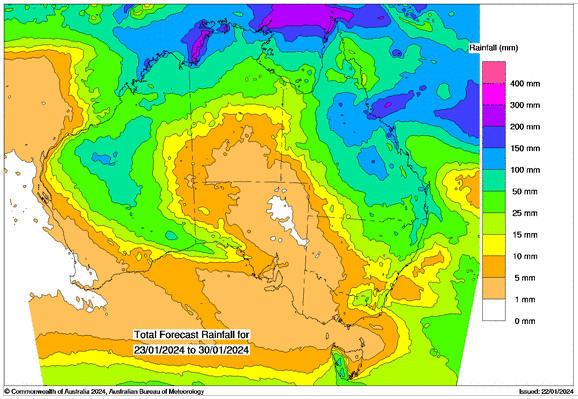

New South Wales (NSW) received more widespread rain last week. There was 15-50mm across most of the state’s cropping areas. Sorghum crops are extremely well-watered and will be on track for well-above average yields. The rain is also reaching the western areas which is allowing farmers to bank soil moisture ahead of winter crop plantings in the autumn, which is reducing the amount of rain they will need at planting to time. Overall, the country has a strong moisture profile ahead of the 2024/25 winter crop promoting optimism for a big wheat, barley and canola season once again.

8 day forecast to 30th January 2024

Source: http://www.bom.gov.au/

Weekly Rainfall to 22nd January 2024

Source: http://www.bom.gov.au/

USDA Report Summary:

USDA released a raft of reports last weekend including the Jan 2024 WASDE report, the Dec 1 US quarterly stocks report and the US winter seedings estimate. The reports were broadly bearish with USDA raising US corn and soybean yields and lifting ending stocks. USDA trimmed Brazil’s summer crops and lifted the Argentine soybean crop, but total supplies increased. USDA also raised China’s corn crop by more than 10MMT which pushed global stocks solidly higher.

US wheat inputs were little changed. USDA jiggled around with the previous season's domestic usage which resulted in a slightly smaller carry in stocks. Globally, USDA lifted world 2023/24 production by 1.9MMT which was in Russia and Ukraine. Russian was up 1MMT to 91MMT and Ukraine 0.9MMT larger at 23.4MMT. World exports were raised by 2.3MMT to 209.5MMT (-10.7MMT year on year (y/y)). Russia increased by 1MMT to 51MMT, Ukraine was up 1.5MMT to 14MMT, Canada was up 0.5MMT to 24MMT and Australia was up 0.5MMT to 19MMT. EU exports were cut by 1MMT to 36.5MMT on the slow export pace. World wheat stocks were raised by 1.3MMT to 260MMT while major exporter wheat stocks were up 3.1MMT to 60.1MMT. EU ending stocks were raised by 2.5MMT to 15.3MMT.

Changes to the corn numbers were bearish on multiple fronts. USDA raised the US 2023/24 US corn yield to 177.3 bpa, a new record high. They lowered the harvested area to 86.5 million acres, but this still resulted in a record crop of 15.34 bill bu. Globally, USDA trimmed Brazil’s crop by 2MMT to 127MMT and left Argentina unchanged at 55MMT. The US crop was up 2.7MMT at 389.7MMT (+41.3MMT y/y). USDA also increased China’s crop by 11.8MMT to 288.8MMT (+11.6MMT y/y). World corn exports were trimmed by 0.7MMT to 190.8MMT on the back of a 1MMT reduction in EU imports. World corn ending stocks were increased by 10MMT to 325MMT (+10MMT in China and +1MMT in the US).

USDA raised the US soybean yield by 0.7 bpa while the harvested area was cut by 400k acres. The total crop was increased by 24 million bu to 4.165 bill bu. Stocks were trimmed slightly. USDA lifted the biofuel demand in the US by a further 1.5% and lowered exports, Biofuels demand now accounts for 48% of the US soyoil demand up from 40% in 2021/22. Globally, USDA cut Brazil’s soybean crop by 4MMT to 157MMT while Argentina was lifted by 2MMT to 50MMT. South America’s (Brazil, Arg and Paraguay) 2023/24 production is 217MMT which is +22MMT y/y. World soybean stocks were 0.4MMT higher to 114.6MMT which is +12.7MMT on y/y.

AUD/USD Currency Update:

Last week we saw the Australian dollar fall from its late December high, however it has since bounced off technical support at 0.6525. The focal point now is on whether the pair can close above the range of 0.6570-0.6580 on a weekly basis. If it does, a potential rally toward 0.6650 and subsequently 0.6700 may be on the horizon.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.