Australian Crop Update – Week 34, 2025

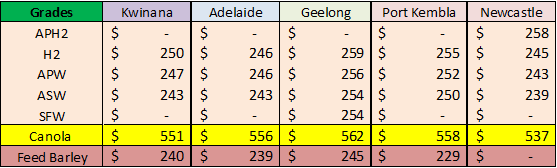

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Local Australian markets drifted lower with limited activity in the past week. Global influences were again negative with the declines in CBOT wheat and corn following the bearish August WASDE report. Most of the domestic focus is now on the new crop but there is limited farmer selling or exporter buying. Growers are reportedly selling some old crop supplier in Northern New South Wales (NSW) and Southern Queensland (QLD) ahead of harvest which begins at the end of next month.

Grower and trade sales of new-crop chickpeas, faba beans, and lentils remain relatively slow reflecting the lateness of most crops, and uncertainty of yields. Lentils prospects have improved greatly for South Australian (SA) and Victorian (VIC) lentils thanks to recent rain, but yields will depend on a kind finish to the growing season. Northern NSW and Southern QLD fava beans crops look to be in good condition, like last year, however the southern crop’s condition is still a matter of debate. Trade talk is that Egypt, the destination for nearly all the faba beans Australia exports, is very well supplied, and unlikely to present the demand - and shipping program - we saw last year.

Export Statistics – June 2025:

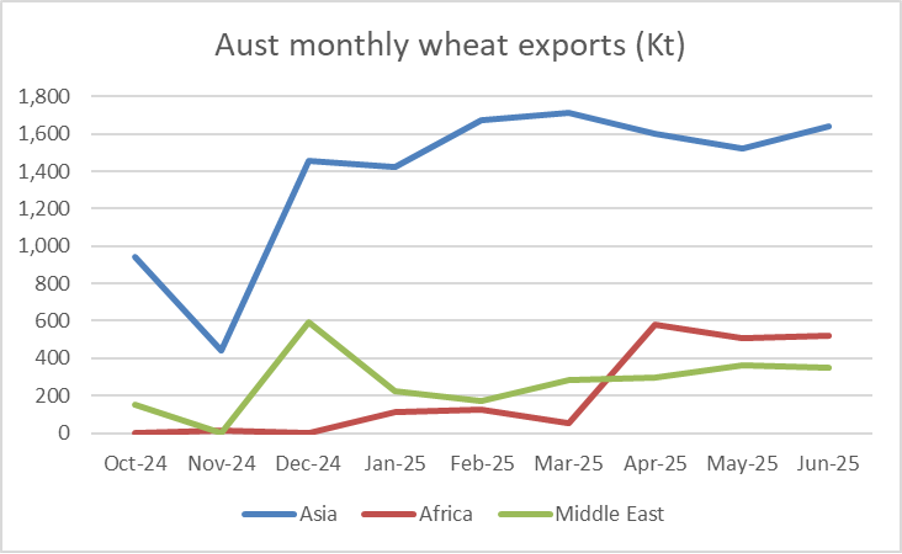

Australia shipped 2.54 million metric tonne (MMT) of wheat in June, slightly down from the 2.59MMT in May. This included 1.42MMT from WA and 0.58MMT from New South Wales (NSW). Container wheat exports were 155 thousand metric tonne (KMT) with Victoria (VIC) falling to 43.5KMT. Indonesia was the largest destination with 649KMT which is the largest monthly shipments to them since Aug 23. Philippines was the next largest with 328KMT. China was just 111KMT. Larger shipments in Africa and the Middle East are helping to make up for the smaller Chinese imports. Australia has shipped 1.6MMT of wheat to African countries in the April to June and 1MMT to the Middle East. Asian exports have been holding around 1.5-1.7MMT/month.

Barley exports remain strong with a further 800KMT shipped in June, just shy of the 845KMT in May. WA accounted for 518KMT of this with 170KMT from VIC and 90KMT South Australia (SA). China made up 78% of the June exports with 622KMT followed by Japan with 152KMT.

There was 245KMT of sorghum exported in June down from 506KMT in May. Nearly all of this went to China. There was 118KMT shipped from Brisbane, 27KMT from Gladstone and 75KMT from Newcastle. Sydney accounted for the remainder.

Canola exports tumbled in June to 102KMT down from 659KMT in May.

Lentil exports were healthy at 61KMT up from 47.2KMT in May. Chickpea exports came in at 43.4KMT which was the biggest month since March. Most of the chickpea exports went to Pakistan with the bulk of the lentils going to Bangladesh. This may be a reflection of the headache traders have had executing into India.

Export Stem & Ocean Freight Market Update:

Shipping stem additions have slowed. There was 158 thousand metric tonne (KMT) of wheat, 60KMT of canola and 30KMT of barley added to the stem in the past week. There was 100KMT of wheat added to the stem in Geraldton.

Australia shipped 2.54 million metric tonnes (MMT) of wheat in June, slightly down from the 2.59MMT in May. Indonesia was the largest destination with 649KMT which is the largest monthly shipments to them since Aug 2023. Philippines was the next largest with 328KMT. China was just 111KMT. Larger shipments into Africa and the Middle East is ensuring the export pace is maintained with 1.6MMT of wheat shipped to African countries from April to June and 1MMT to the Middle East. Asian exports have been holding around 1.5-1.7MMT/month. Barley exports remain strong with a further 800KMT shipped in June, just shy of the 845KMT in May. China made up 78% of the June exports with 622KMT followed by Japan with 152KMT.

Lentil exports were healthy at 61KMT up from 47.2KMT in May. Chickpea exports came in at 43.4KMT which was the biggest month since March. Most of the chickpea exports went to Pakistan with the bulk of the lentils going to Bangladesh. This may be a reflection of the headaches traders have had executing into India.

Panamaxes are holding steady while Ultramaxes and Handysize continue to gently firm buoyed by an increase in Indo coal and Aussie grains. With tonnage still feeling tight, there is a confidence that the market will continue to hold firm at least in the near term as fresh demand continues to hit the market.

Australian Weather:

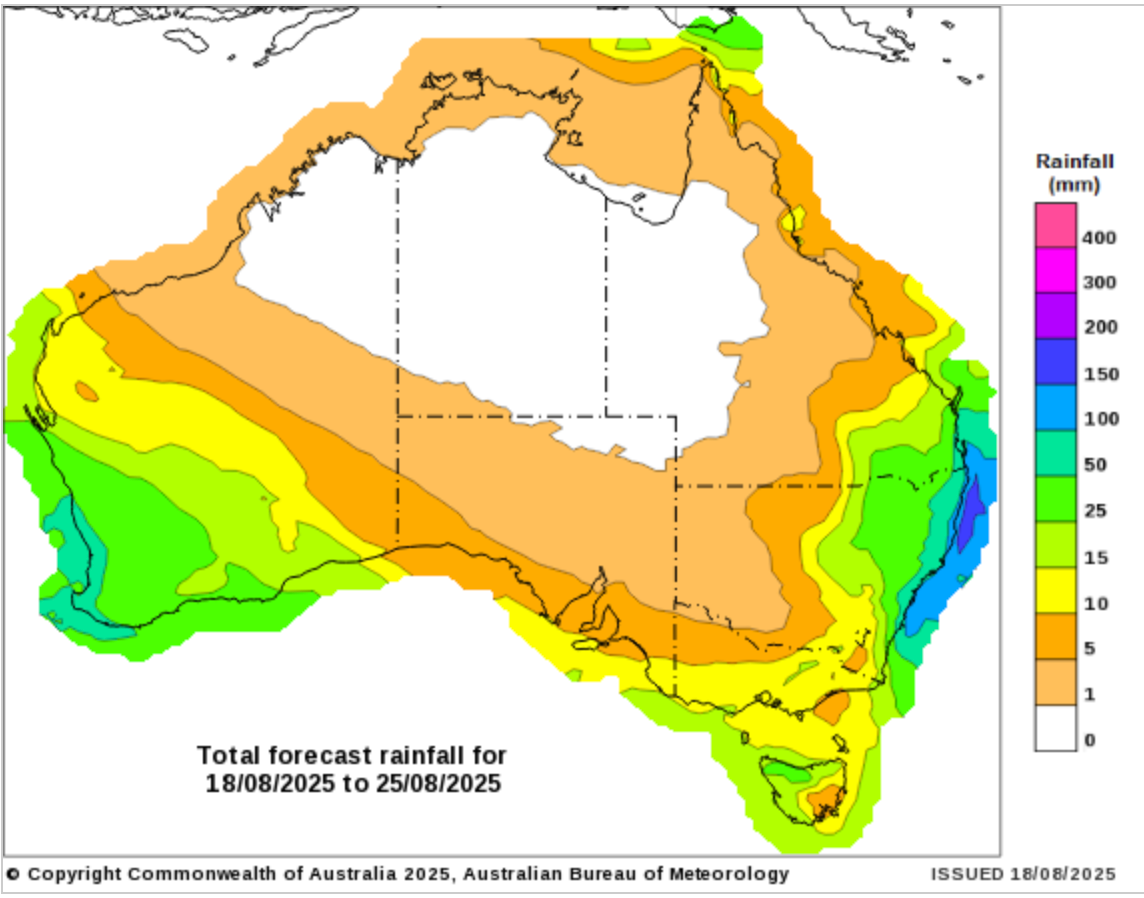

Australia’s Bureau of Meteorology released its latest long-range weather forecast last week with above average rainfall predicted for eastern Australia for September to December. The latest forecasts offer more rain for Western Australia (WA), Southern QLD and possibly Northern NSW in the next week but Southeast Australia is expected to see limited rain in the next 7-10 days were crops are already two to four weeks later than normal in their development.

8 day forecast to 25 August 2025

http://www.bom.gov.au/

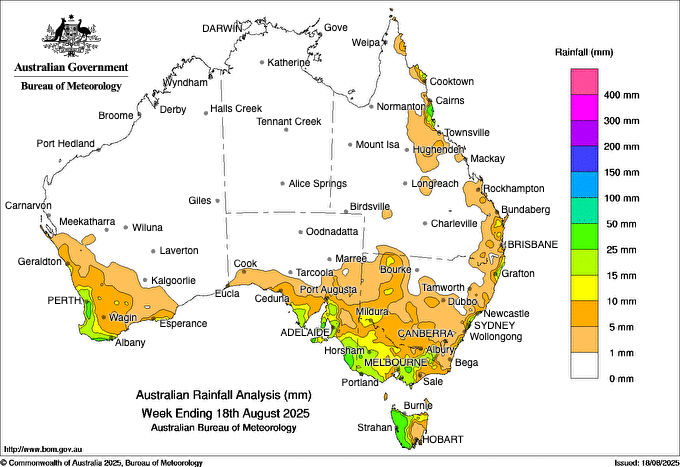

Weekly rainfall to 18 August 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

During the week of August 11 to 17, 2025, the Australian dollar (AUD) exhibited modest movement against the U.S. dollar (USD), ending the period with a slight overall decline, fluctuating between a low of 0.6498 USD and a high of 0.6556 USD. The weekly average settled around 0.6518 USD, marking a mild weekly loss of approximately 0.10%. Overall, the AUD’s performance remained relatively stable, reflecting a cautious trading environment and limited domestic inputs.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.