Australian Crop Update – Week 33, 2025

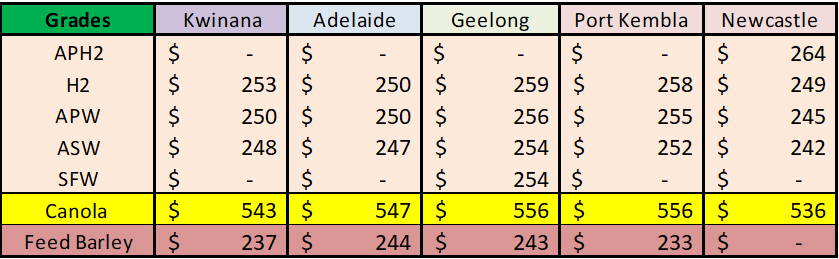

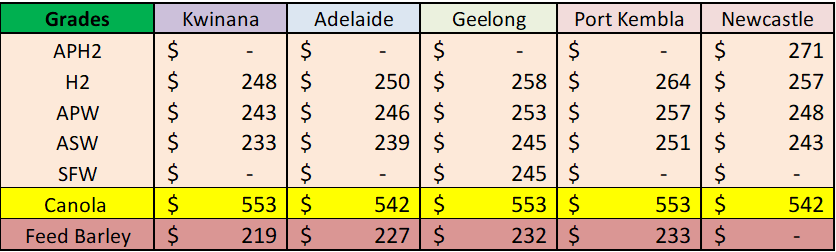

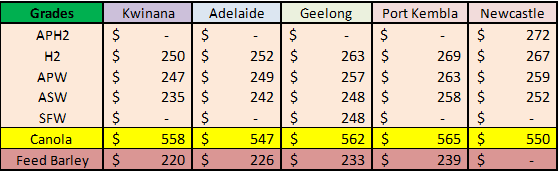

2024-25 New Season - USD FOB Indications

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australian Grains Market Update

Local Australian markets finished mixed last week with bearish global influences weighing in on grain bids. There were signs however that cheaper prices were starting to trigger export demand late in the week with larger volumes being traded to cover apparent shorts. Western Australia (WA) APW10.5 was quoted USD 250 per metric tonne (/MT) FOB which is seen as competitive into Asia. Export buying interest is reportedly picking up at these levels for bulk and container buyers with interest emerging on the lower prices for the nearby months. Most of the demand appears to be for Sep/Nov as the inverse from old to new crop condenses. It was reported that AH12 wheat sold at around $260/MT FOB. Container exporters were also reporting improved demand albeit at prices that were difficult to work. Nonetheless, demand is surfacing at current prices.

Export Statistics – June 2025:

Australia shipped 2.54 million metric tonne (MMT) of wheat in June, slightly down from the 2.59MMT in May. This included 1.42MMT from WA and 0.58MMT from New South Wales (NSW). Container wheat exports were 155 thousand metric tonne (KMT) with Victoria (VIC) falling to 43.5KMT. Indonesia was the largest destination with 649KMT which is the largest monthly shipments to them since Aug 23. Philippines was the next largest with 328KMT. China was just 111KMT. Larger shipments in Africa and the Middle East are helping to make up for the smaller Chinese imports. Australia has shipped 1.6MMT of wheat to African countries in the April to June and 1MMT to the Middle East. Asian exports have been holding around 1.5-1.7MMT/month.

Barley exports remain strong with a further 800KMT shipped in June, just shy of the 845KMT in May. WA accounted for 518KMT of this with 170KMT from VIC and 90KMT South Australia (SA). China made up 78% of the June exports with 622KMT followed by Japan with 152KMT.

There was 245KMT of sorghum exported in June down from 506KMT in May. Nearly all of this went to China. There was 118KMT shipped from Brisbane, 27KMT from Gladstone and 75KMT from Newcastle. Sydney accounted for the remainder.

Canola exports tumbled in June to 102KMT down from 659KMT in May.

Lentil exports were healthy at 61KMT up from 47.2KMT in May. Chickpea exports came in at 43.4KMT which was the biggest month since March. Most of the chickpea exports went to Pakistan with the bulk of the lentils going to Bangladesh. This may be a reflection of the headache traders have had executing into India.

Export Stem & Ocean Freight Market Update:

A further 311KMT of wheat and 90KMT of canola was added to the stem in the past week. There was new barley vessels put onto the stem in the past week. There was also some faba beans and lentils put on the stem in Adelaide. WA accounted for 223KMT of the wheat that was put onto the stem in the past week, and the remainder was in Quattro Pt Kembla. All the canola was in WA. Stem additions are slowing but this comes as no surprise. There has been 660KMT of wheat added to the WA stem in the past four weeks compared to 725KMT in the previous four weeks.

Australian Weather:

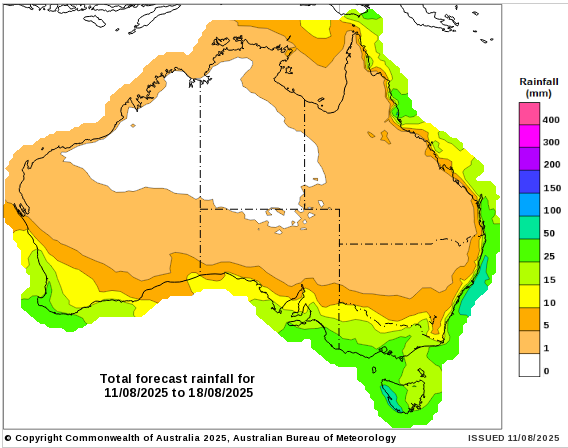

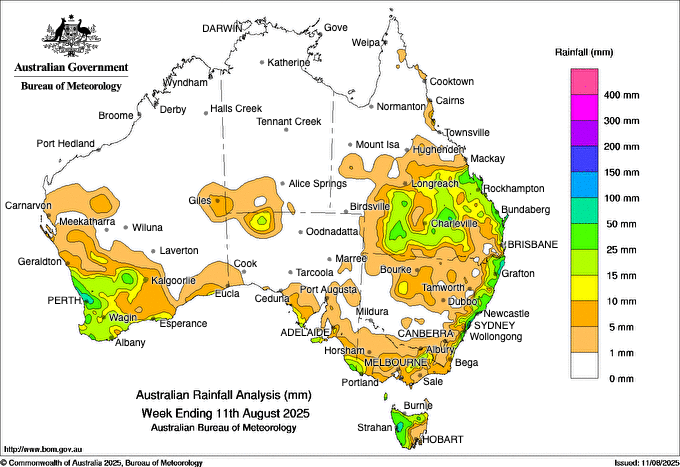

There has been improving sub-soil moisture profiles across Australia’s cropping zones. The levels have improved following the good July rains which is showing a lot of similarities to where were at this time last year. Queensland (QLD) and Northern NSW are very good. Conditions taper away in Southern NSW. Conditions are mixed in VIC as is SA with below average moisture but improving following the rain. Rainfall over the next week appears to mainly coastal after decent soaking rains were received in most cropping areas last week. VIC and SA will be the biggest beneficiary with 10mm to 20mm expected in cropping regions.

8 day forecast to 18 August 2025

http://www.bom.gov.au/

Weekly rainfall to 11 August 2025

http://www.bom.gov.au/

AUD/USD Currency Update:

Last week the Australian dollar (AUD) exhibited a modest yet steady appreciation against the US dollar (USD). The currency began the week trading in a relatively stable range between 0.6469 and 0.6477 USD, reflecting cautious market sentiment in the early sessions. However, as the week unfolded, several positive developments contributed to a gradual strengthening of the Aussie dollar. A primary catalyst was the release of stronger-than-expected trade balance data from Australia, which revealed that the nation continued to maintain a healthy trade surplus. This bolstered investor confidence in Australia’s broader economic outlook, reinforcing the AUD’s appeal to close out at .6524.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.