Basis Commodities – Australian Crop Update – Week 48

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

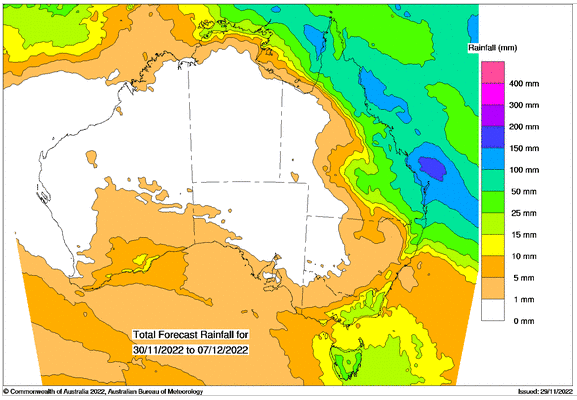

A week of dry weather across the country pulled the domestic cash markets sharply lower last week and that weakness has continued on the back of improved weather on the east coast as well as broader weakness in global markets. The question is how much of this will the owners of export elevators pass onto consumers given they are well sold through to the second quarter of 2023.

Queensland harvest is about 75% complete while NSW is still less than a fifth complete. Grain quality on the east coast was variable. Larger than expected supplies of AH2 have eased domestic miller concerns but expectations were low to start with. Growers will naturally focus on better paddocks first and quality is expected to decline through the NSW central west and southwest which has seen more rain than the north in recent weeks.

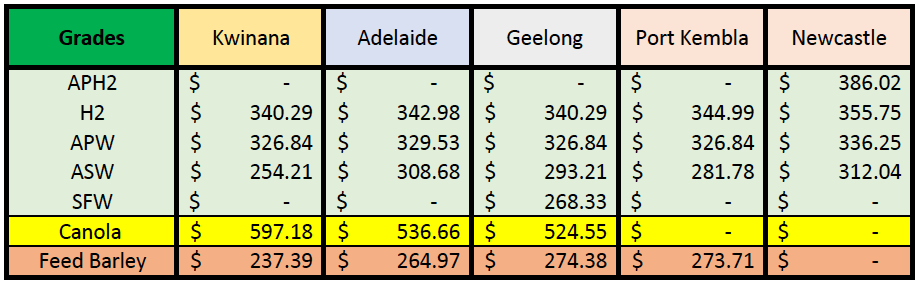

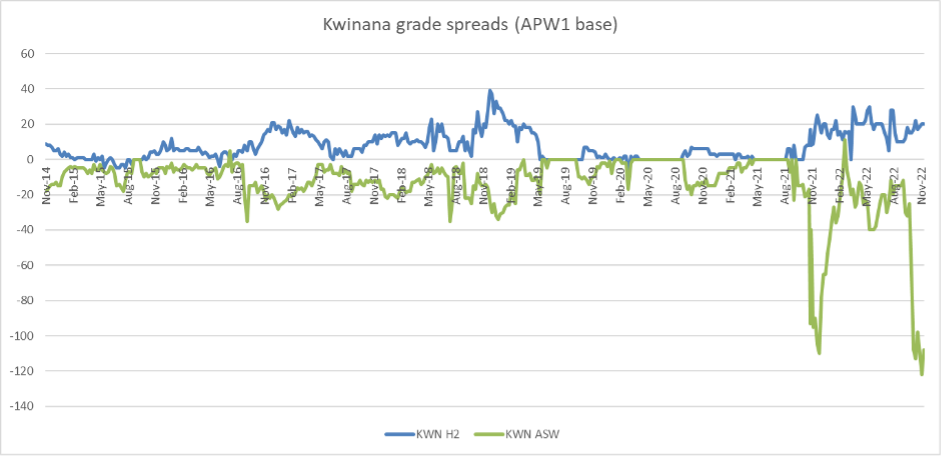

In Western Australia, the dry, warm weather also provided a huge harvest week. We understand that CBH received about 3MMT of grain deliveries in the past week which lifts the total harvest deliveries to 6.8MMT. Wheat protein levels have declined as the harvest picks up in the Kwinana zone. A significant proportion of wheat is reportedly ASW1 which is sub 9% protein and as a consequence, the ASW/APW spread has widened at the track level.

Looking forward – The Weather forecast across Australia is increasingly favourable for the next ten days or so. We expect that CBH could receive more than 3MMT of weekly grain deliveries with the warm, dry weather which would be about double the previous week. WA is still on track for a record 23MMT crop with several Geraldton sites already reporting record receivals.

Other states are also making good harvest progress. SA’s Eyre Peninsula will make big inroads into the harvest and activity is picking up in the Mallee. South Australia’s wheat quality has been good so far with a mix of H2, APW and ASW. Queensland and Northern New South Wales will also make solid progress.

The better wheat quality has significantly eased domestic quality concerns for milling wheat which should see the market’s focus return to export driven factors. Indeed, in terms of the cash markets, the protein spreads came under some pressure on the east coast and some FOB sellers of milling wheat have emerged, although the offers remain limited until the southern harvest cranks up and the logistics improve.

With respect to logistics, a slow start to harvest has seen some congestion build in WA, and Eastern Australia continues to face significant risk after the heavy rain and flooding. Freight corridors in some areas are in a state of disrepair, with an estimated 10,000 km of road impacted in NSW. Rail links are not much better with major lines connecting storage sites being impacted by flooding. In early November, a derailed freight train cut a key route from Adelaide to Melbourne for over a week until it could be repaired. This will compound the already slow start to harvest as growers struggle to get heavy machinery into paddocks without being bogged down.

In a precursor to what we may see on wheat when we get further into the New South Wales crop, the Australian Oilseed Federation (AOF) has established two segregations with a tolerance for mouldy seed for the canola Crop. The new segregation allows for 40 mouldy seeds per 1000 seeds compared to the normal 5 mouldy seeds per 1000. The new segregations have come about following consultation with domestic crushers, exporters, and bulk handlers to ascertain the extent of the quality impacts, and to assess options for dealing with weather-impacted canola.

Ocean Freight & Export Stem

There was 930KMT of wheat, barley and canola added to the stem in the past week. 70% of the weekly additions were in WA.

This week may prove interesting as some Indonesian coal cargoes appeared on the market. Immediately owners were trying to push the numbers a little however conflicting with this was news over the weekend of unrest in China and the possibility of falling commodity demand due to further lockdowns. As we write, it’s hard to call how this is going to play out. Owners are talking a good game but without much conviction. The market is volatile, and we are at a low point we have not seen for 2.5 years – in short, players are quite jittery either way

Looking forward, Oslo-based Xeneta. suggests that ocean cargo volumes could fall by up to 2.5% and ocean freight rates will drop “significantly” into 2023.

Currency

In FX markets, the clouded near-term outlook for China and the weaker yuan saw the AUD down 1.5%. The AUD is currently around 0.6652 after ending last week at around 0.6754. That puts the AUD back around levels before the move lower in the USD on Wednesday last week.

The post Basis Commodities – Australian Crop Update – Week 48 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.

Newsletter Signup

Quick Links

Basis Commodities Pty Ltd

PO Box 340, Northbridge

NSW 1560, Australia

Basis Commodities Consulting DMCC

PO Box 488112

Dubai, UAE

Copyright © 2024 Pty Ltd. All rights reserved.

site by mulcahymarketing.com.au