Basis Commodities – Australian Crop Update – Week 50, 2023

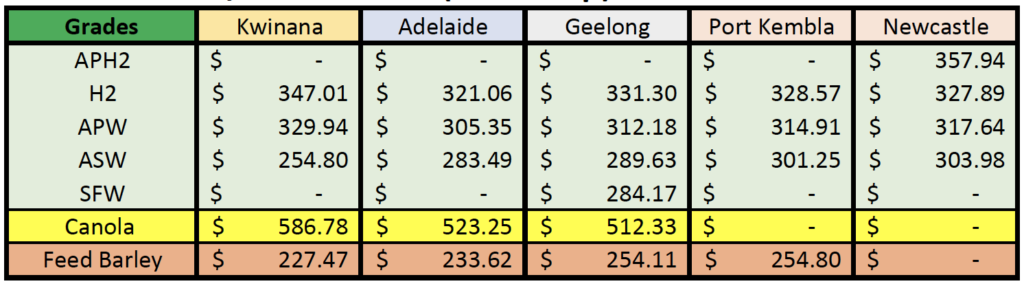

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS.

Australia’s winter grain harvest is now progressing quickly after the slow start. All the major storage companies are reporting strong weekly grain deliveries and the fine weather over the past week will ensure this trend continues. Queensland harvest is nearly complete. New South Wales is about 30% complete with wet subsoils slowing harvest progress. Victoria is just getting under way, while South and Western Australia are progressing quickly and are both over half done.

Yields remain good, but wheat proteins are lower than normal. In New South Wales, wheat quality is variable but there has been more protein than expected. This has allowed domestic millers to access protein wheat and so for time being, protein spreads are under pressure. We feel this is an opportunity international consumers should look closely at.

Farmer selling has slowed with the decline in local prices as domestic supply and quality concerns ease. There are no accurate measures on farmer selling, it is subjective by its nature, but it is fair to say growers were already behind the normal selling pace leading into harvest and falling values is slowing sales through the harvest window. Our take is that farmers will exit harvest with less of the crop sold in percentage terms than in other years.

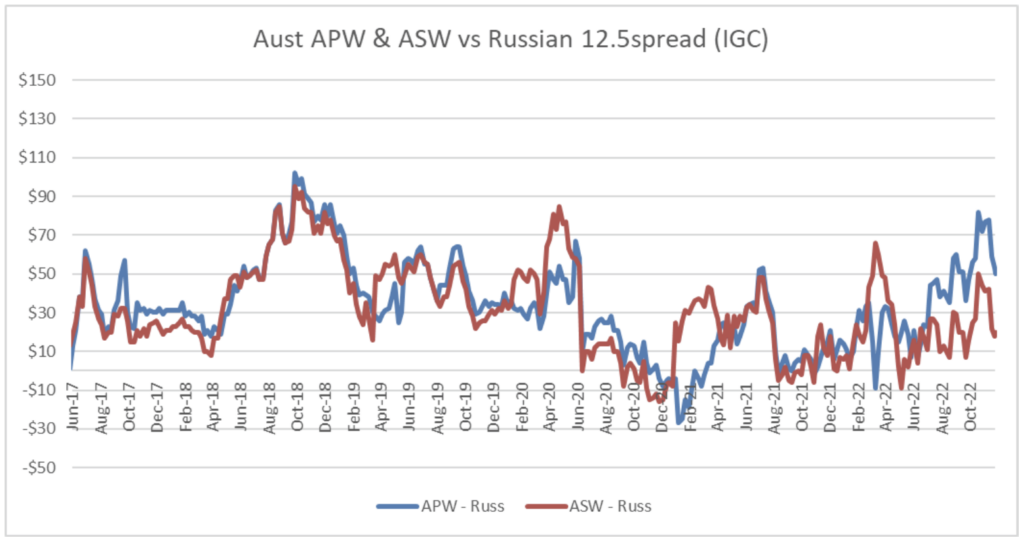

Track markets in most states were softer. The track market largely reflects where the exporter buying interest is. We get the impression that exporters are struggling to make further sales at the export margins they have been accustomed to in recent times. The combination of falling global wheat prices, slow farmer selling and importers who are keeping their demand spot and are seeing cheaper Russian wheat and lower ocean freight is likely to continue to pressure margins. This can be seen in the narrowing spread between Australian and Russian wheat quotes (see chart below). On the exporter side there is a reluctance to offer and therefore we are working hard with our customers to provide aggressive bids to start the conversation with sellers.

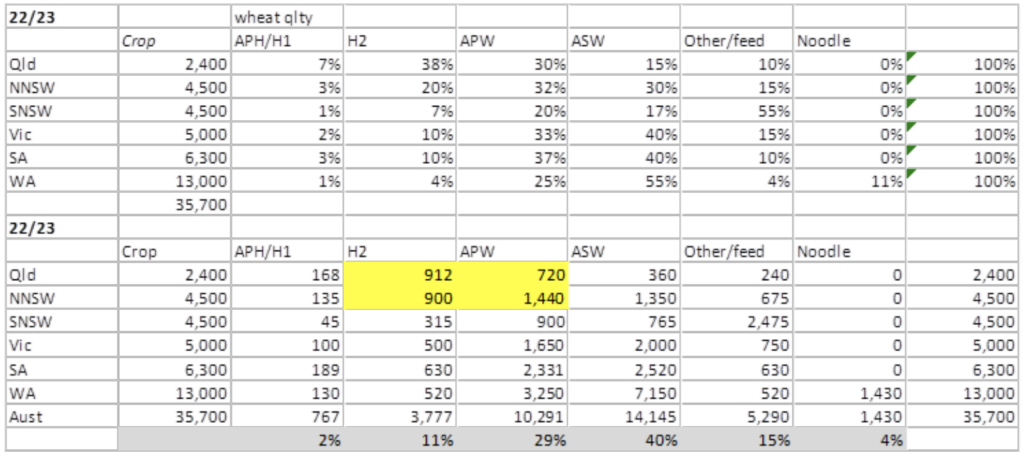

Crop Profile Update

Given the above, our analysts have made some small changes to the expected crop profile by increasing the AH2 and APW volumes expected in Queensland and Northern NSW. This would leave a quality exportable surplus from this region.

Pulses

As with grains and canola, the yields for lentils and beans have been very good so far. Lentils, like canola have been a grower favourite this year and we are told the quality has held up reasonably well in South Australia. The situation on Fava Beans is a little more unclear. The yields are good and there will be plenty around post-harvest, but quality continues to have growers and sellers worried given the rain and potential for disease, so the market remains at a standstill. There is a bean bulk cargo on the stem for January and this is likely to be seen as a litmus test for other exporters who, given the late harvest, have been moving the export slots back into March and beyond.

December WASDE Summary

US ag markets were mixed after the USDA’s December WASDE failed to offer any big surprises.

Wheat:

USDA kept its US wheat assumptions largely unchanged. They juggled the grade exports but kept the overall US wheat exports unchanged at 21.1MMT with 2202/23 ending stocks unchanged at 15.5MMT.

The global wheat situation was a function of lower supplies and shrinking consumption. Overall global production was cut by 2.1MMT to 780.6MMT. Argentine production was cut by 3.0MMT to 12.5MMT as they accounted for the impact of the drought on crop size. Canada was lowered by 1.2MMT to 33.8MMT following the StatsCan Nov report. This was partly offset by a 2.1MMT increase in the Australian crop to 36.6MMT in line with ABARES. Other major producers were unchanged. Global wheat consumption was cut by 1.6MMT to 789.5MMT, mainly on lower feed use in the EU and Ukraine. World trade was raised by 2.2MMT to 210.9MMT with higher exports from Australia, Ukraine, EU and Russia more than offsetting the smaller exports from Argentina. Australian wheat exports were raised by 1.5MMT to 27.5MMT (we don’t think this will be achieved given the smaller NSW crop which will restrict east coast exports while the big WA crop is limited by export capacity). USDA is expected larger feed wheat exports from Australia into Southeast Asia and South Korea. Ukraine’s exports were raised by 1.5MMT to 12.5MMT on the back of the healthy export pace. Argentine exports were cut by 2.5MMT to 7.5MMT which is the smallest since 2014/15. Russian wheat exports were raised by 1.0MMT to 43MMT, EU was lifted by 1.0MMT to 36MMT. Canada was unchanged at 26MMT.

Corn:

USDA cut US corn exports by 75 mill bu to 2.075 bill bu which is 16% down from last year with the lagging shipping pace. Ethanol and domestic feeding were unchanged. US ending stocks were raised by 75 mill bu to 1.257 bill bu. Further reductions in the US exports will need to happen if the export sales don’t improve. USDA lowered the US farmer corn price by 10 cts to $6.70. bu. USDA also cut the US sorghum exports by 20 mill bu on the decline in imports from China. The smaller exports were absorbed by larger feeding and FSI.

Global corn was interesting. World corn production was cut by 6.5MMT to 1162MMT on the back of a 4.5MMT reduction in Ukraine output to 27.0MMT with the reduction in area and yield. The EU crop was trimmed by a further 0.5MMT to 54.2MMT. South American production forecasts were unchanged with Brazil at 126MMT and Argentina at 55MMT. Global corn exports were cut by 1.1MMT to 181.6MMT. However, Ukraine’s exports were lifted by 2.0MMT to 17.5MMT on the back of the strong shipping pace, despite the smaller crop. Global corn imports were cut by 1.2MMT on the back of smaller imports into Southeast Asia and South Korea which is importing more feed wheat from Australia. World corn ending stocks were cut by 2.4MMT to 298.4MMT which is down 8.7MMT on last year (mainly in the US and China).

Barley:

World barley production was lifted by 0.5MMT to 149.5MMT. This was mainly due to the 0.7MMT increase in Australia to 13.4MMT in line with the ABARES increase. Argentine production was lowered by 0.3MMT to 4.2MMT. World barley exports were trimmed by 0.1MMT to 29.6MMT which is down 3.1MMT (9%) on last year. There were limited changes, although the EU imports were up 0.2MMT to 1.3MMT as they import more Black Sea feed barley because of the smaller corn crop. Thailand imports were cut by 0.1MMT to 0.4MMT. Australian barley exports were raised by 0.3MMT to 7.5MMT while Argi exports were cut by the same amount. China and Saudi imports were unchanged at 9.0MMT and 4.7MMT, respectively.

Soybean:

US soybean forecasts were unchanged from November. Production, crush, exports and ending stocks were unchanged. Based on a review of EPA’s recent proposed rule for renewable fuel obligation targets, soybean oil used for biofuel for 2022/23 is reduced 200 million pounds to 11.6 billion. Soybean oil exports are also reduced on historically low export sales through November. With reduced use of soybean oil for biofuel and exports, food use and ending stocks are raised.

South American soybean production was unchanged with Brazil at 152MMT (+25MMT last year), Argentina at 49.5MMT (+5.6MMT last year) and Paraguay at 10MMT (+5.8MMT on last year). Exports were raised slightly as higher shipments for Argentina are partly offset by lower exports for Canada and Paraguay. Global crush was close to unchanged. Ending stocks were up 0.5MMT to 102.7MMT (+7.1MMT last year).

Canola/rapeseed:

USDA cut Canadian canola production by 0.5MMT to 19.0MMT following the StatsCan report. This wasn’t the full extent of the StatsCan reduction. Canada’s crush was trimmed by 0.2MMT to 10MMT. FWC was up 150KMT to 450KMT. Exports were down 50KMT at 7.90MMT while ending stocks were lowered by 0.4MMT to 1.65MMT. Australian production was unchanged at 7.3MMT and exports unchanged at 5.2MMT. EU and China imports were unchanged. World stocks were cut by 0.36MMT with the smaller Canadian crop but are still 2.5MMT more than last year at 6.8MMT.

Australian Exports

ABS released its October export data late last week. Australia exported 2.042MMT of wheat in October up from 1.78MMT in September. WA shipped 983KMT and then NSW 450KMT followed by Vic with 391KMT. Indonesia was the largest destination with 453KMT closely followed by China with 426KMT. South Korea took 303KMT and Philippines 222KMT.

Barley exports fell to just 247KMT. Japan was the largest destination with 129KMT. Sorghum exports were at 276KMT down from 400KMT in September. China remains the major destination taking 268KMT.

2022/23 Shipping stem

There was 1.1MMT of wheat, barley and canola added to the shipping stem last week down from 1.3MMT in the previous week (largest in 8 months). Weekly additions of more than 1MMT are large given the max monthly export capacity is about 4MMT. There was 684KMT of wheat added to the stem in the past week following the 824KMT in the previous week. There was a further 236KMT of canola added to the stem and 190KMT of barley.

Ocean Freight

Charterers exploited an indifferent market in the last week even though spot tonnage was not so easy to find. This week has continued to be quiet, and we suspect this is the “end of term” feel that typically afflicts the market at this time of year. Freight went sideways in Asia for the second week in a row. Tellingly, there remains a sizeable quota of Chinese controlled tonnage being marketed for business – indicating China demand is itself subdued. As we mentioned last week, the groundswell of opinion suggesting a recovery in freight rates during February is increasingly popular however we are not so sure – the recessionary clouds keep gathering and ocean freight rates are often the canary in the cage with respect to global economic activity.

AUD Commentary

The FX markets remain choppy ahead of the final major reporting week of the year. It seems to us that the AUD is currently range bound between .685 on the upside and .65 on the downside and will take further direction into the new year.

The post Basis Commodities – Australian Crop Update – Week 50, 2023 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.

Newsletter Signup

Quick Links

Basis Commodities Pty Ltd

PO Box 340, Northbridge

NSW 1560, Australia

Basis Commodities Consulting DMCC

PO Box 488112

Dubai, UAE

Copyright © 2024 Pty Ltd. All rights reserved.

site by mulcahymarketing.com.au