Basis Commodities – Australian Crop Update – Week 15 2022

Market Update

Apologies for the delay between reports. With much of the grain markets focus elsewhere and international travels, unfortunately the weekly report had to be put on hold.

Last week was a steady week for Australian grain markets, with the grower remaining proud sellers. Those needing to are being forced to pay up and this looks set to continue as we head into the Easter holidays. Interestingly, barley also strengthened against feed wheat on the east coast with traders continuing to report that barley continues to be difficult to secure.

Milling quality wheat was generally up $10/MT for the week in most port zones which reflected the ongoing success of Australian milling wheat in the export markets where it feels most of the stem is well sold through to June and even most of July.

The Australian Bureau of Statistics (ABS) released its February export data last week and it confirmed what the domestic trade is acutely aware of – logistics are stretched to the max. Australia shipped 2.8MMT of wheat, 885KMT of barley and 608KMT of canola in Feb for a combined 4.3MMT.

In terms of sales pace, so far this marketing year (Oct 21/Sep22) Australia has shipped 10.62MMT of wheat which is 38% of the forecast Oct/Sep exports of 27.5MMT, 3.65MMT of barley which is 46% of the forecast Oct/Sep exports of 7.92MMT and 2.18MMT of canola in the Oct/Feb which is 52% of the forecast Oct/Sep exports of 4.23MMT. The shipping pace indicates Australia’s wheat ending stocks at the end of Sept will be below 5MMT despite a harvest of around 36.5MMT and this is testament to the amount of demand Australia has picked up, and is expected to continue to fill, due to the Russian invasion of Ukraine.

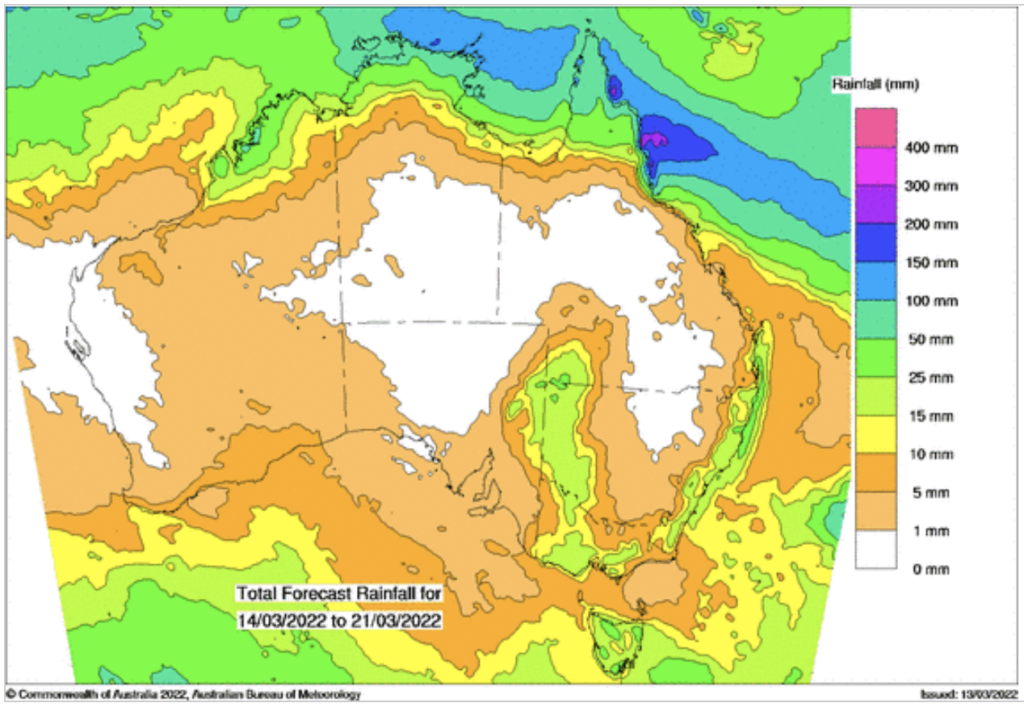

A quick update on logistics. Queensland and New South Wales shipping operations have been significantly slowed in March due to floods and associated supply chain disruptions and the BOM has forecast above average rain for April as well. In speaking with some east coast exporters, this disruption looks set to continue with damage to rail lines affecting the ability to accumulate grain along with an increasing list of vessels waiting to load.

On the positive side, much of the country is in great shape ahead of planting the 2022/23 crop. With 2021/22 exports maximised, this will leave smaller than expected carryover stocks than we had been forecasting prior to the outbreak of Russian hostilities in Ukraine.

Our analysts Agscientia expect canola plantings for 2022/23 will be held at similar levels to 2021/22 while their initial assumptions will be a wheat crop of 28.5MMT, barley 11.0MMT and canola at 4.6MMT. Pulses will increase on the margins. Higher yield assumptions will hinge on above average spring rains and a mild finish in Sept/Oct. Australia is off to a good start, but history tells us it’s too early to bank on that and there are some drier areas out there.

Weather

USDA April WASDE report summary

WHEAT:

USDA cut world wheat stocks by 3.1MMT to 278.4MMT. Most of this was in India where USDA raised domestic usage by 4.4MMT while production and exports were unchanged. Global wheat imports were lowered by 3.0MMT to 200MMT which is 2.5MMT less than 2020/21 as demand slows with the high prices and difficulty in accessing supplies with the war in Ukraine. Old crop wheat balance sheet issues are easing with the big Indian exports and slowing demand. The markets focus is now firmly on the 2022/23 crop where dry weather in the US central and southern plains, and the second worst winter crop conditions on record are helping to keep futures supported.

CORN:

USDA left the US 2021/22 corn balance sheet unchanged.

BARLEY:

There were limited changes in the USDA’s barley numbers. USDA cut 1.0MMT from global barley output to 145.1MMT. World barley trade was close to unchanged at 34.7MMT. Chinese and Saudi imports were unchanged at 10.5MMT and 5.9MMT respectively.

Ocean Freight

The freight market remains relatively soft as we enter the Ramadan and Easter periods. Sentiment remains neutral with both owners and charterers content to just let the market drift. Charterers point toward Ramadan and Easter, fewer coal stems from Indonesia, COVID issues in china and the potential for lower fuel prices as reasons the market should continue to ease. Owners talk up a still strong cargo picture and point to last year when the market pulled back only to soar away in Q2. If charterers are right, then we are experiencing a circuit breaker moment when we break out from the positivity of the past year, and if the owners are right then we are going to see an unseemly scramble for cover in early May. Despite the current market weakness (tonnage lists are still lengthening around the nearby positions), it is notable that period numbers remain a solid premium to spot – albeit that charterers are actively attempting to push those numbers down to be more in line with voyage levels. Handymax are fixing spot around the pacific at close to $30kpd dop, Supramax tonnage is heading toward mid $20k’s per day for the benchmark pacific round, while Panamax is hovering just over $20kpd for the same route.

Australian Dollar

Last week we saw the Aussie dollar surge through 0.76 US cents on the heels of a hawkish RBA policy update that saw interest rates on hold but a subtle shift in rhetoric fuelled expectations the board will raise rates in the coming months. However, by the end of the week a slightly weaker risk appetite from the market in general saw the Australian dollar fall below 75 U.S. cents.

The post Basis Commodities – Australian Crop Update – Week 15 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.

Newsletter Signup

Quick Links

Basis Commodities Pty Ltd

PO Box 340, Northbridge

NSW 1560, Australia

Basis Commodities Consulting DMCC

PO Box 488112

Dubai, UAE

Copyright © 2024 Pty Ltd. All rights reserved.

site by mulcahymarketing.com.au